| Information |  | |

Derechos | Equipo Nizkor

| ||

| Information | | |

Derechos | Equipo Nizkor

| ||

06Apr16

Text of the civil antitrust action filed to prevent Halliburton's acquisition of Baker Hughes

UNITED STATES DISTRICT COURT

FOR THE DISTRICT OF DELAWARE

UNITED STATES OF AMERICA, Plaintiff,

v.

HALLIBURTON CO.,

and

BAKER HUGHES INC.,Defendants.

Civil Action No.: COMPLAINT

The United States of America, acting under the direction of the Attorney General of the United States, brings this civil antitrust action to obtain equitable relief to prevent the acquisition of Defendant Baker Hughes Inc. by Defendant Halliburton Company. The United States alleges as follows:

I. INTRODUCTION

1. Halliburton's proposed acquisition of Baker Hughes would violate Section 7 of the Clayton Act, 15 U.S.C. § 18, because it would combine two of the three largest providers of oilfield services in the world, it would eliminate substantial head-to-head competition, and it would likely lead to higher prices and less innovation in this critically important industry.

2. Evaluating oil and gas reserves, drilling wells to reach those reserves, completing those wells, and extracting oil and gas from the ground are expensive, risky, time-consuming, and complex endeavors. They require many different products and services, including drill bits, drilling services, pumping, fluids, sand control, cementing, valves, plugs, and sensors. Halliburton and Baker Hughes, together with Schlumberger, are the "Big Three" -- the largest globally-integrated suppliers of these products and services. They compete to win the business of exploration and production (E&P) companies and to develop next generation technologies that will allow them to drill deeper and operate in ever-more challenging conditions. They possess unrivaled product portfolios, research and innovation capabilities, and the scope and scale necessary to address the most difficult technological challenges facing the oil and gas industry they serve.

3. The U.S. economy, American consumers, and those who engage in the production of energy consumed in the United States cannot be asked to accept the risk to competition posed by this transaction. Accordingly, the Court should enjoin it.

II. DEFENDANTS AND THEIR UNLAWFUL PROPOSED MERGER

4. Founded in 1919, Halliburton is the largest provider of services to the oil and gas industry in the United States. It has operations in approximately 80 countries and approximately 65,000 employees. In 2015, it earned revenues of $23.6 billion and invested $487 million in research and development. It has thousands of patents relating to oilfield technologies. Halliburton operates two divisions, one focused on drilling and evaluation and the other focused on completion and production. It also has a product service line called Consulting and Project Management, which spearheads its integrated services strategy and works across both divisions.

5. Baker Hughes was formed in 1987 with the merger of Baker International and Hughes Tool Company, both founded over 100 years ago. Like Halliburton, Baker Hughes has operations in more than 80 countries. It has approximately 43,000 employees and earned revenues of $15.7 billion in 2015. Baker Hughes considers itself to be an industry leader in research and innovation: it invested $483 million in research and development in 2015, it maintains hundreds of active research projects, and it has thousands of patents relating to oilfield technologies. In 2014 alone, Baker Hughes introduced 160 new products and generated over $1 billion from new products in their first 12 months of commercialization. Like Halliburton, Baker Hughes' oilfield services fall into two categories - drilling and evaluation, and completion and production - and it has an Integrated Operations group that provides comprehensive solutions to E&P companies.

6. Following a suggestion in early 2014 by a mutual stockholder of Halliburton and Baker Hughes, Halliburton approached Baker Hughes about a combination of the two companies in the fall of 2014. On November 16, 2014, after resisting the takeover attempt based in large part on antitrust concerns, Baker Hughes relented and agreed to be acquired by Halliburton in a transaction valued at $34.6 billion. This transaction is unprecedented in the breadth and scope of competitive overlaps and antitrust issues it presents. It would substantially lessen competition, not just in one or two isolated businesses, but across a broad spectrum of product and service lines that are critical to the oil and gas industry and that represent billions of dollars in annual E&P expenditures. It would leave E&P companies with one fewer major supplier driving down prices, improving services, innovating, developing new technologies, and otherwise competing for their business.

7. Defendants recognized the antitrust problems raised by their transaction when they negotiated their agreement. On November 4, 2014, Baker Hughes CEO Martin Craighead wrote to Halliburton CEO David Lesar, "we have both agreed that a combination of Halliburton and Baker Hughes will raise significant issues under the antitrust laws of the United States and other jurisdictions. . . . [I]t remains unclear whether there are workable solutions that appropriately address the antitrust risk and the completion risk." Halliburton prevailed upon Baker Hughes to take the legal risk of this transaction only by threatening a damaging hostile takeover bid and by offering a premium on the price of Baker Hughes' shares, a commitment to divest assets representing up to $7.5 billion in sales, and a reverse breakup fee of $3.5 billion if the merger could not be consummated.

8. Halliburton has proposed divesting a collection of assets selected from various Halliburton and Baker Hughes business lines in an attempt to remedy the many antitrust concerns that have been raised by the Antitrust Division of the Department of Justice and by antitrust authorities in other countries. Halliburton has had extensive discussions with a potential buyer of these assets but has not entered into a definitive agreement for a sale.

9. Although the terms of Halliburton's proposed remedy continue to change, it appears to be among the most complex and riskiest remedies ever contemplated in an antitrust case. It would separate business lines and divide facilities, intellectual property, research and development, workforces, contracts, software, data, and other assets across the world between the merged company and the buyer of the divested assets. Many customer contracts would not be transferred. For some of the services for which the transaction is likely to lessen competition substantially, the proposed remedy fails to divest many of the assets used to provide such services (such as tools, facilities, employees, and contracts). The proposed remedy would thus leave the buyer dependent on Halliburton for services that are crucial to the businesses being divested. And the proposed remedy would create a divestiture business that lacks assets in important segments of oilfield services that each of the Big Three possess today, such as fracking, onshore cementing, and onshore fluids.

10. For these reasons, among others, the assets that Halliburton proposes to divest would have lower sales volume and lower market share, be less efficient, have less research and development, provide fewer innovations and customized solutions, be less able to offer integrated solutions, and otherwise fail to replicate the competition provided by Defendants' businesses from which they would be extracted. The proposed remedy would also impose an unprecedented burden on the Court and the United States, as it would require oversight of the global separation and transfer of thousands of assets and employees, as well as the performance of numerous service agreements for years into the future. Therefore, if offered by Halliburton as a remedy in this case, the Court should reject this proposed remedy as wholly inadequate to resolve the risks to competition posed by this transaction.

III. MARKETS IN WHICH COMPETITION MAY BE SUBSTANTIALLY LESSENED

11. Defendants compete across a broad range of products and services. Over 90% of the revenue earned by Halliburton comes from products and services that are also offered by Baker Hughes. This complaint focuses on the 23 markets in which the effects of the proposed acquisition on competition would be particularly acute. Competition would likely be lessened with respect to other products and services as well, and would be diminished in the overall business of oilfield services, where there would be one fewer globally-integrated provider competing for the most substantial projects and driving innovation to new solutions.

12. Each of the products and services described below constitutes a line of commerce or an activity affecting commerce as those terms are used in Section 7 of the Clayton Act, 15 U.S.C. § 18, and each is a relevant product market in which competitive effects can be assessed. They are recognized in the industry as separate business lines, they have unique characteristics and uses, they have customers that rely specifically on these products and services, they are distinctly priced, and they have specialized vendors. In addition, they each satisfy the well-accepted "hypothetical monopolist" test, set forth in the U.S. Department of Justice and Federal Trade Commission Horizontal Merger Guidelines, which asks whether a hypothetical monopolist likely would impose at least a small but significant and non-transitory increase in price. Such a price increase would not be defeated by substitution to alternative products and services.

13. Adverse effects from the proposed transaction would likely differ from one customer to the next. Some customers are unwilling to take the risk of using oilfield services companies other than Halliburton, Baker Hughes and Schlumberger for certain types of work due to the complexity of the well, the advanced technology required, significant safety or environmental concerns, the cost of fixing the work if a less-sophisticated competitor fails to perform it adequately, or other reasons. Because prices are typically negotiated for each project or tender, Halliburton would be able to profitably raise prices to these customers after it acquired Baker Hughes.

14. Halliburton and Baker Hughes compete with each other for customers located throughout the United States. A hypothetical monopolist of each of the products and services described below likely would impose at least a small but significant increase in the price charged to customers in the United States. Such a price increase would not be defeated by substitution to another product or service, or by purchasing products or services outside the United States. Accordingly, the United States is a relevant geographic market for each of the relevant markets described below.

15. The more concentrated a market would be after a proposed merger, and the more the proposed merger would increase concentration, the more likely it is that the proposed merger would substantially lessen competition. Concentration can be measured in various ways, including by market shares and by the widely-used Herfindahl-Hirschman Index ("HHI") (see Appendix). Under the Horizontal Merger Guidelines, if the post-transaction HHI would be more than 2500, and the change in HHI would be more than 200, there is a presumption that the proposed acquisition is likely to enhance market power and substantially lessen competition. Given the high concentration levels and increases in concentration in the relevant product markets below, the proposed acquisition presumptively violates Section 7 of the Clayton Act. In many of these markets, customers would effectively face a duopoly after the transaction. In the following paragraphs the relevant product markets are described in the approximate order in which each product or service is used in the well drilling and completion process.

16. The revenue, share, and HHI data cited in the complaint are largely based on 2014 data, the most recent full year for which the United States has data from its investigation sufficient to estimate these figures. The oil and gas industry has experienced a significant downturn during the past year, including a downturn in exploration, drilling, and completion activities that drive demand for Defendants' products and services. Therefore, discovery may show substantial revenue reductions for 2015. The United States does not anticipate that updated data will change the conclusions drawn below about the likely anticompetitive effects of the proposed transaction.

A. Relevant Market #1: Offshore Directional Drilling Services

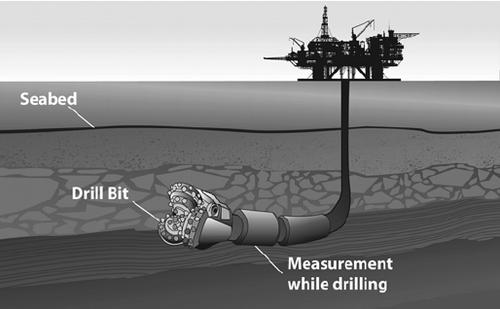

17. Directional drilling involves drilling a well at an angle, typically using either a steerable downhole motor or a rotary steerable system. A directional drilling service company provides the tools and expertise needed to steer the drill string and correctly position the wellbore within the formation. The service company provides both directional drilling tools, which allow the directional driller to understand and manipulate the orientation of the drill bit, and service personnel, who interpret data on the position of the drill bit and control the well's trajectory. Integral to this process is the service of Measurement While Drilling ("MWD"), which provides real-time information about the exact location and direction of a drill bit during the drilling process. Due to the unique requirements of offshore drilling, the offshore directional drilling services market is separate from the onshore directional drilling services market. Offshore Directional Drilling Services in the United States comprise a relevant antitrust market.

[Images throughout the Complaint are for illustrative purposes only and are not to scale.] 18. In 2014, this market had total revenue of over $500 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 43% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 94%. The post-transaction HHI is approximately 4400, with an increase of approximately 800 resulting from the acquisition. An internal analysis by Baker Hughes' drilling business confirms that the Big Three perform nearly all the offshore directional drilling in the Gulf of Mexico and there is "little to no competition" from smaller firms.

B. Relevant Market #2: Offshore Logging While Drilling Services

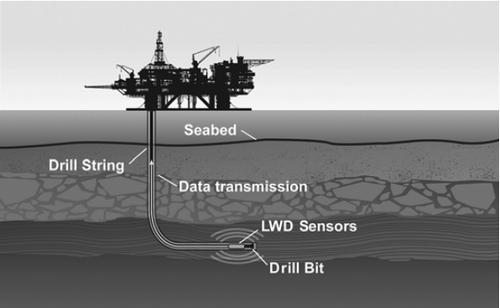

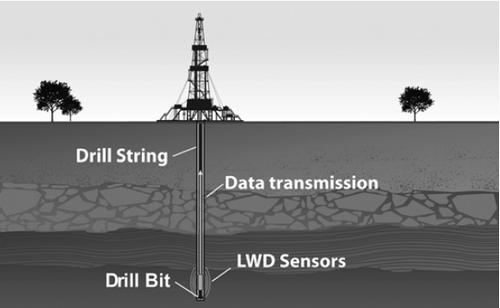

19. Logging While Drilling ("LWD") refers to the collection of data on a formation's properties during the drilling process. Data is collected from sensors mounted above the drill bit or motor. This data is used to optimize wellbore position in the reservoir, to efficiently plan next steps such as completions design, and to estimate the reservoir's hydrocarbon reserves. Due to the differences in well conditions, customer requirements, technology, logistics, and other factors, the offshore LWD services market is separate from the onshore market. Defendants have admitted in regulatory filings that "[t]here is no realistic substitute for LWD services in offshore drilling." Offshore LWD Services in the United States comprise a relevant antitrust market.

20. In 2014, this market had total revenue of over $200 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 48% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 94%. The post-transaction HHI is approximately 4400, with an increase of approximately 1000 resulting from the acquisition. In materials prepared by Halliburton in mid-2015 for the potential sale of its LWD business, Halliburton told buyers that the LWD market is "led by SLB, BHI and Sperry Drilling [Halliburton]" and there are "[significant barriers to entry (requires high degree of technological competence and effort)."

C. Relevant Market #3: Onshore Logging While Drilling Services

21. As described above, onshore LWD Services differ in significant respects from offshore LWD services. Onshore LWD Services in the United States comprise a relevant antitrust product market.

22. In 2014, this market had total revenue of $350 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 59% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 78%. The post-transaction HHI is approximately 4100, with an increase of approximately 900 resulting from the acquisition.

D. Relevant Market #4: Fixed Cutter Drill Bits

23. Drill bits used for drilling oil and gas wells are attached to the bottom of a drill string and are used to cut or crush rock. There are two main categories: fixed cutter and roller cone. Fixed cutter drill bits are solid metal-diamond bits with no moving parts. These drill bits are used in certain stages of well drilling, for certain wellbore sizes, in certain types of rock formations, or in other situations where roller cone drill bits are not appropriate. Fixed Cutter Drill Bits sold in the United States comprise a relevant antitrust market.

24. In 2013, this market had total revenue of approximately $1.4 billion in the United States and Canada. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 52% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 78%. The post-transaction HHI is approximately 3300, with an increase of approximately 1300 resulting from the acquisition. In materials prepared by Halliburton in mid-2015 for the potential sale of its drill bits business, Halliburton told buyers that "[Halliburton], Schlumberger and Baker Hughes are the leading competitors in the Fixed Cutter marketplace" and that "[s]maller competitors have found difficulty increasing share . . . ."

E. Relevant Market #5: Roller Cone Drill Bits

25. Roller cone bits have multiple cones, each rotating on its own axis during drilling. These drill bits are used in certain stages of well drilling, for certain wellbore sizes, in certain types of rock formations, or in other situations where fixed cutter drill bits are not appropriate. Roller Cone Drill Bits sold in the United States comprise a relevant antitrust market.

26. In 2013, this market had total revenue of over $300 million in the United States and Canada. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 35% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 72%. The post-transaction HHI is approximately 2600, with an increase of approximately 350 resulting from the acquisition. The Chief Integration Officer of Baker Hughes testified that Halliburton and Schlumberger represent the biggest competitive threats to Baker Hughes in drill bits.

F. Relevant Market #6: Offshore Drilling Fluids Services

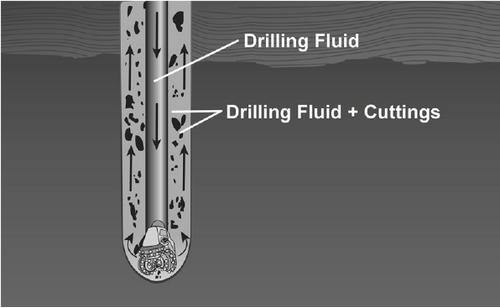

27. Drilling fluids are water-based, oil-based, or synthetic fluids used during the drilling process to keep the drill bit cool and clean, remove cuttings from the wellbore, control pressures in the wellbore, and prevent formation fluids from entering the wellbore. In addition to the fluids themselves, oilfield service companies provide associated services, such as formulation, mixing, monitoring, and testing. Due to the distinct and more complex requirements of offshore customers, resulting from environmental regulations and differences in geology, temperatures, pressure, and depth, among other factors, the offshore drilling fluids services market is separate from the onshore market. Offshore Drilling Fluids Services in the United States comprise a relevant antitrust product market.

28. In 2014, this market had total revenue of approximately $800 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 40% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 94%. The post-transaction HHI is approximately 4500, with an increase of approximately 650 resulting from the acquisition. The effect of the acquisition would be even more pronounced in the deepwater segment: as the head of Baker Hughes' Drilling and Completion Fluids business acknowledged, "[t]he deepwater market is dominated by BHI, HAL & SLB" and has "high barriers to entry."

G. Relevant Market #7: Offshore Surface Data Logging Services

29. Surface data logging, also called mud logging, involves the analysis of rock cuttings and gases brought to the surface in the drilling fluids during the drilling of a well. It helps provide information about potentially productive hydrocarbon-bearing formations. A specialized crew, including geologists, creates a detailed record (mud log) of the properties of the rock cuttings and formation gases, and other aspects of the drilling process. The surface data logging provider often performs other related services, such as safety support services, which are also included in the relevant market. Due to the more complex well conditions, customer requirements, technology, and other factors, the offshore surface data logging services market is separate from the onshore market. Offshore Surface Data Logging Services in the United States comprise a relevant antitrust product market.

30. In 2014, this market had total revenue of approximately $150 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 36% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 78%. The post-transaction HHI is approximately 3100, with an increase of approximately 550 resulting from the acquisition.

H. Relevant Market #8: Offshore Open Hole Wireline Services

31. Wireline services are a collection of instrumental readings, sampling, testing, or mechanical services in a wellbore. The tools and instruments are conveyed into the wellbore by means of a cable that can send and receive electrical signals, and the resulting data is recorded in a log. Open hole wireline services are performed after drilling has commenced but before the well is lined with casing (large-diameter metal pipe) and cement. They are used to evaluate the formation and help determine whether the well should be completed and whether other wells should be drilled in the area. Due to the unique requirements of offshore wireline services, the offshore open hole wireline market is separate from the onshore market. Offshore Open Hole Wireline Services in the United States comprise a relevant antitrust market.

32. In 2014, this market had total revenue of over $200 million. This market would be highly concentrated after the proposed acquisition because the number of competitors would be reduced from three to two. Historically, Baker Hughes and Schlumberger were the two principal providers in this market -- in 2014, Baker Hughes had a share of approximately 13% and Schlumberger had a share of approximately 86% -- as Halliburton lacked the most advanced technologies needed in the high pressure environments found in the Gulf of Mexico, particularly in deepwater. However, Halliburton is active in deepwater markets in other countries and has engaged in a multi-year effort to build up its expertise and technology to better compete with Baker Hughes and Schlumberger in the United States. Halliburton has started to win contracts from E&P companies in the U.S. Halliburton's presence as a wireline provider in the Gulf of Mexico has already resulted in tens of millions of dollars in potential savings for at least one E&P company.

33. Because Halliburton's emergence in deepwater is so recent, and most of the awards are for future projects that may not commence operations until 2016 or later, historical data does not capture Halliburton's competitive significance. Halliburton is the biggest threat to Baker Hughes and Schlumberger going forward. No firm other than Halliburton, Baker Hughes, and Schlumberger has a significant share or is likely to become an important competitor in the future.

I. Relevant Market #9: Offshore Liner Hanger Systems and Services

34. A liner is a string of casing that, instead of being run all the way up to the wellhead, is "hung" from the inside and bottom of the casing string above it. A liner hanger is the device used to attach a liner to the casing string above it. The service of hanging liners is typically provided by the company that provides the liner hangers and is included within the market definition. Liner hangers used offshore are distinct from those used onshore because offshore customers face unique challenges and require more robust pressure and temperature ratings, larger sizes, and greater reliability, among other things. Offshore Liner Hanger Systems and Services in the United States comprise a relevant antitrust market.

35. In 2014, this market had total revenue of approximately $150 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately an 84% share of the market. (Schlumberger has approximately a 1% share.) The post-transaction HHI is approximately 7200, with an increase of approximately 2600 resulting from the acquisition.

J. Relevant Market #10: Onshore Liner Hanger Systems and Services

36. Due to distinctions in customer requirements and other factors described above, the market for onshore liner hangers is separate from the offshore market. Onshore Liner Hanger Systems and Services in the United States comprise a relevant antitrust market.

37. In 2014, this market had total revenue of over $400 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 72% share of the market. (Schlumberger has approximately a 4% share.) The post-transaction HHI is approximately 5300, with an increase of approximately 2100 resulting from the acquisition.

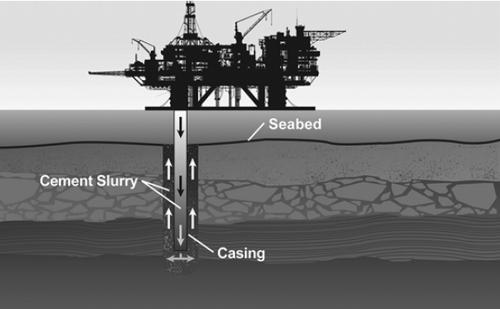

K. Relevant Market #11: Offshore Cementing Services

38. Oilfield cementing is the process of pumping cement down a wellbore to secure the well casing to the rock formation, isolate oil and gas producing zones from non-producing zones, repair leaks or failed cement jobs, set a kick-off plug to assist in maneuvering the drill bit, or seal an abandoned well to prevent fluid migration, among other purposes. Cementing services involve mixing dry cement and additives at a facility, transporting the cement mix to the well site, preparing a slurry, and pumping the slurry into the wellbore. Due to the unique challenges of performing offshore cementing, including enhanced technical, logistical, and regulatory requirements, the offshore cementing services market is separate from the onshore cementing services market. Offshore Cementing Services in the United States comprise a relevant antitrust market.

39. In 2014, this market had total revenue of approximately $400 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 56% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 99%. The post-transaction HHI is approximately 5000, with an increase of approximately 1500 resulting from the acquisition. In a strategic planning session, Halliburton's cementing executives recognized that this market is already a "pure oligopoly" among the Big Three.

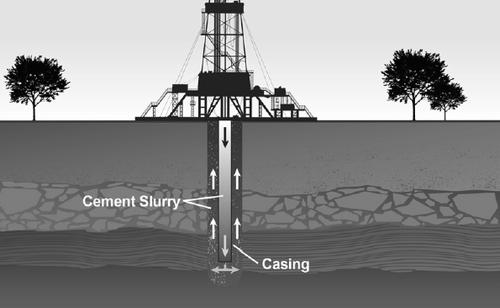

L. Relevant Market #12: Onshore Cementing Services

40. Onshore cementing is performed using different equipment and differs in other respects from offshore cementing, as described above. Onshore Cementing Services in the United States comprise a relevant antitrust market.

41. In 2014, this market had total revenue of over $4 billion. Combined, Halliburton and Baker Hughes have approximately a 45% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 62%. The post-transaction HHI is approximately 2400, with an increase of approximately 800 resulting from the acquisition. Defendants are close competitors in this market: the Chief Integration Officer of Baker Hughes testified that Halliburton poses the most significant competitive threat to Baker Hughes in cementing.

42. While competition would be substantially lessened in the U.S. Onshore Cementing Market as a whole, the effects of the proposed acquisition would be particularly significant in cementing complex wells and in certain geographic areas where customers have fewer choices, including parts of Texas, Louisiana, California, and Oklahoma.

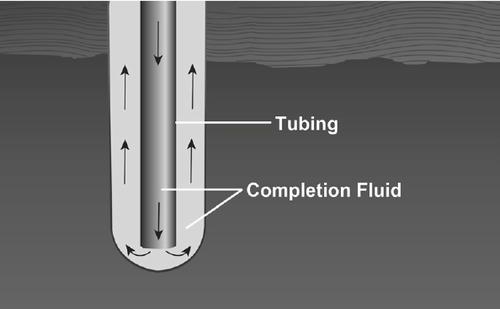

M. Relevant Market #13: Offshore Completion Fluids Services

43. Completion fluids are solids-free liquids that are typically used after the drilling process is complete to prevent damage to the formation or completion components. Other uses include controlling well pressure during completion, obtaining maximum flow, increasing the well's capacity, and making it easier to repair the well if necessary. In addition to the fluids themselves, oilfield service companies provide related services such as technical expertise and support. Due to the unique requirements of offshore completion fluids applications, including extreme pressure and temperature conditions and the need for higher density fluids made of different chemical compounds, the offshore completion fluids market is separate from the onshore market. Offshore Completion Fluids Services in the United States comprise a relevant antitrust market.

44. In 2014, this market had total revenue of approximately $300 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 49% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 74%. The post-transaction HHI is approximately 3600, with an increase of approximately 1100 resulting from the acquisition.

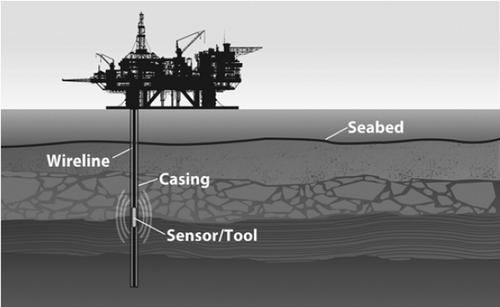

N. Relevant Market #14: Cased Hole Wireline Services for Rigs in Deepwater

45. Cased hole wireline services are used to assess the condition and integrity of a well, evaluate the properties of a reservoir by taking measurements through the well casing and cement, and log hydrocarbon production. They are also used to perform mechanical and perforation services (punching holes in the casing to allow hydrocarbons to flow into the wellbore). Cased hole wireline services for rigs located in deepwater require more sophisticated tools and technology than in other locations. Cased Hole Wireline Services for rigs in deepwater in the United States comprise a relevant antitrust market.

46. In 2014, this market had total revenue of over $50 million. This market would be highly concentrated after the proposed acquisition. While smaller suppliers can provide some specialty services, E&P customers also issue tenders to determine a single primary supplier of cased hole wireline services for rigs operating in deepwater. Halliburton, Baker Hughes and Schlumberger are generally the only competitors for such tenders. The vast majority of revenue in this market is earned by Halliburton, Baker Hughes, and Schlumberger. Smaller providers that work in other parts of the United States do not have the technology and other resources necessary to provide the cased hole services used on deepwater rigs for the drilling and completion of wells.

O. Relevant Market #15: Onshore Frac Plugs

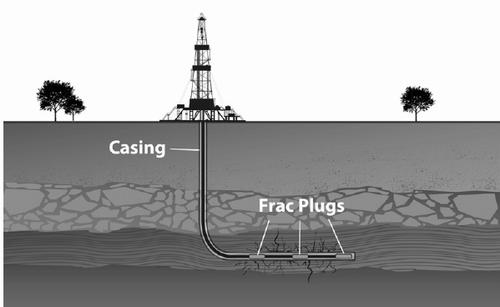

47. Frac plugs are used in a method of multistage fracturing known as "plug and perf" to isolate zones within a wellbore. Plug and perf is one of the predominant methods of fracking in the United States, and is mainly employed onshore. This method involves the following sequence of steps: (a) a frac plug is set inside the casing via wireline, (b) a designated area of the casing and formation is perforated, and (c) fluids are pumped under high pressure into the perforated formation to stimulate the production of hydrocarbons through the holes made by the perforation. This process is then repeated until all desired zones of the well have been treated. At the conclusion of the process, plugs are typically either milled out using coiled tubing or dissolve on their own, allowing production to commence. Onshore Frac Plugs sold in the United States comprise a relevant antitrust market.

48. In 2014, this market had total revenue of approximately $950 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 62% share of the market. (Schlumberger has approximately an 8% share.) The post-transaction HHI is approximately 4100, with an increase of approximately 1800 resulting from the acquisition.

P. Relevant Market #16: Offshore Sand Control Tools

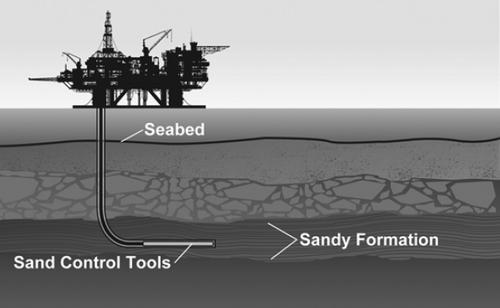

49. Sand control tools include various types of packers and associated devices, as well as service tools used in the installation of sand control screens to block migration of sand into the wellbore. Sand control tools are used predominantly offshore. Offshore Sand Control Tools sold in the United States comprise a relevant antitrust market.

50. In 2014, this market had total revenue of over $200 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have a share of approximately 63%. (Schlumberger has approximately a 5% share.) The post-transaction HHI is approximately 5000, with an increase of approximately 1600 resulting from the acquisition.

Q. Relevant Market #17: Offshore Stimulation Vessel Services

51. Offshore stimulation vessel services involve pumping water and proppants (materials used to hold fissures open) under high pressure into a formation to create a pathway for hydrocarbons. These services are provided by specially-equipped vessels, which have pumps and other specialized equipment. Stimulation vessel services are necessary for most wells in the Gulf of Mexico. Offshore Stimulation Vessel Services in the United States comprise a relevant antitrust market.

52. In 2014, this market had total revenue of over $150 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately an 86% share of the market. The post-transaction HHI is approximately 7700, with an increase of approximately 3700 resulting from the acquisition. In the ultra-deepwater segment of the market, Defendants are the only current competitors.

R. Relevant Market #18: Offshore Production Packers and Services

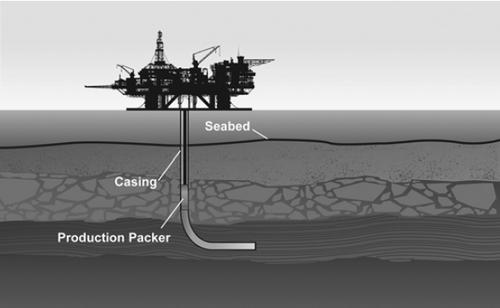

53. Production packers are tools installed when a well is being prepared for production that seal or "pack off" the wellbore in order to control or redirect the flow path of fluids in the well - typically routing fluids into the production tubing through which oil and gas is produced. A production packer consists of pipe through which well fluids can flow, gripping elements called "slips" that anchor the packer to the wall of the casing, and a sealing element. Production packers used in offshore applications are distinct from onshore packers because they have more robust pressure and temperature ratings, are substantially more expensive, are often customized for a specific project, and are not typically used interchangeably with packers designed for onshore use. Along with the packers, oilfield service companies offer the service of running and setting the packers in the well. Offshore Production Packers and Services sold in the United States comprise a relevant antitrust market.

54. In 2014, this market had total revenue of approximately $100 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 75% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 95%. The post-transaction HHI is approximately 6100, with an increase of approximately 2500 resulting from the acquisition.

S. Relevant Market #19: Onshore Production Packers and Services

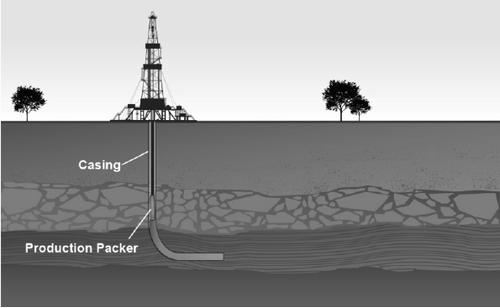

55. Due to distinctions in customer requirements, prices, and other factors described above, the market for onshore production packers is separate from the offshore market. Onshore Production Packers and Services sold in the United States comprise a relevant antitrust market.

56. In 2014, this market had total revenue of over $300 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 57% share of the market. (Schlumberger has approximately a 2% share.) The post-transaction HHI is approximately 3500, with an increase of approximately 1200 resulting from the acquisition.

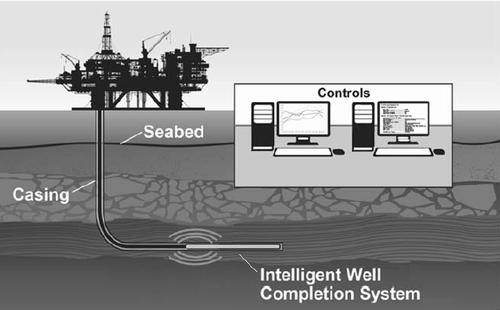

T. Relevant Market #20: Offshore Intelligent Well Completion Systems and Services

57. Intelligent well completion systems are a suite of products installed in the wellbore that permit the remote monitoring and control of production from one or more zones of the well. Components of these systems include permanent downhole monitors and gauges, technology to transmit data collected by the monitors and gauges to the surface, and controls at the surface from which commands can be sent downhole to adjust flow by opening and closing sleeves or valves. Intelligent well completion systems are predominantly used offshore. Offshore Intelligent Well Completion Systems and Services in the United States comprise a relevant antitrust market.

58. In 2014, this market had total revenue of over $100 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 58% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 99%. The post-transaction HHI is approximately 5000, with an increase of approximately 1000 resulting from the acquisition.

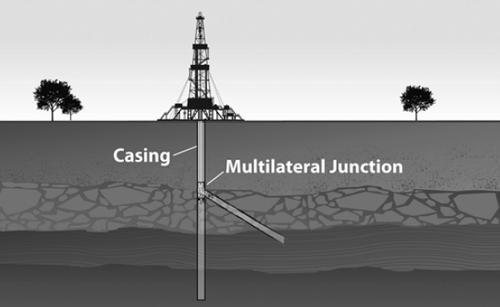

U. Relevant Market #21: Multilateral Completion Systems and Services for TAML Levels Two and Above

59. Multilateral completion systems are used to construct multiple branches which radiate from the main wellbore. They allow the drilling and completion of multiple wells within a single wellbore. The industry has adopted standard classifications, called Technology Advancement of Multilaterals or "TAML" levels, based on the complexity of the junction (ranging from levels one through six). The completion process for TAML levels two and above involves the placement of specialized junction hardware where the divergent wells intersect to reinforce and maintain the junctions. In contrast, TAML level one involves an open hole and no specialized hardware. Due to their complexity, and the extensive design, engineering, drilling, and completion expertise required to create and install them, multilateral junctions with TAML levels of two and above constitute a separate relevant market. Such multilateral completion systems require significant design and installation services, and these services are included within the relevant market. Multilateral Completion Systems and Services for TAML Levels Two and Above in the United States comprise a relevant antitrust market.

60. This is an emerging market in the United States and reliable sales and market share data are not available. However, the parties have acknowledged that globally only four companies account for more than 99% of sales of multilateral completion systems and services for TAML levels two and above. Because the same companies that compete globally have the ability to provide such multilaterals in the U.S., the closest available proxy for calculating concentration levels is global market shares. Halliburton and Baker Hughes have a combined global market share of approximately 70%, and the acquisition would increase HHI levels by over 1100 points, resulting in a highly concentrated market with HHIs of over 5600. Combined, Defendants and Schlumberger together hold approximately 90% of the global market.

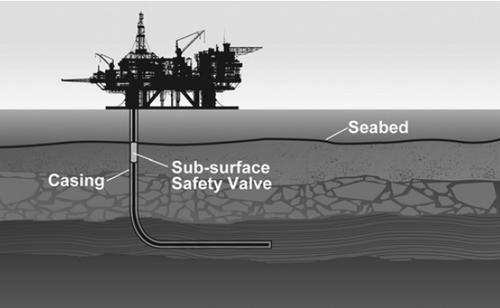

V. Relevant Market #22: Offshore Sub-Surface Safety Valves

61. Sub-surface safety valves ("SSSVs") are fail-safe valves installed in the upper wellbore to provide automatic emergency closure of the well's producing conduits in the event of an emergency. Their use offshore is mandatory under federal government safety regulations. Due to the unique requirements offshore, including well pressures and temperatures, the offshore SSSV market is separate from the onshore market. Offshore SSSVs and associated services sold in the United States comprise a relevant antitrust market.

62. In 2014, this market had total revenue of approximately $75 million. This market would be highly concentrated after the proposed acquisition. Combined, Halliburton and Baker Hughes have approximately a 46% share of the market, and Defendants and Schlumberger together hold a combined share of approximately 97%. The post-transaction HHI is approximately 4700, with an increase of approximately 350 resulting from the acquisition. Halliburton's SSSV product managers recognize that Baker Hughes is the "leader" and "our main competitor" in SSSVs.

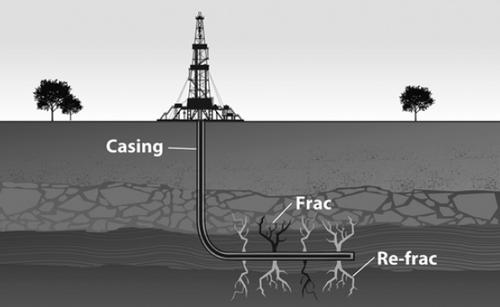

W. Relevant Market #23: Integrated Refracturing Solutions

63. When a well is hydraulically fractured, only a small percentage of the available hydrocarbons is typically recovered. Integrated refracturing solutions are a suite of services that function together to restimulate such wells. These services include candidate selection through reservoir data analysis, real-time surface and downhole pressure monitoring, use of chemical diverters to isolate the production zone, and customized refracturing design and execution. Integrated refracturing solutions are distinct from other forms of refracturing, sometimes referred to as "pump and pray," due to the level of technology, integration, and reservoir modeling data utilized. Defendants view integrated refracturing solutions as potentially a multi-billion-dollar per year business that, as a top Halliburton executive told the company's Board of Directors, "is poised to take off." Both Halliburton and Baker Hughes have been investing substantial resources to develop and market these products. Integrated Refracturing Solutions in the United States comprise a relevant antitrust market.

64. Integrated Refracturing Solutions is an emerging market in which the products have only recently been introduced, and reliable sales and market share data are not yet available. However, Defendants' internal documents reflect the fact that only the Big Three are serious participants in this market because of the breadth of their product lines, their ability to integrate products and services, the quality of their reservoir data, and their capacity to conduct the necessary R&D. As the Baker Hughes refracturing team stated in a strategy document provided to the Vice President of Corporate Development, "only the big '3' service providers are expected to have the 'complete' solutions package." Therefore, this market, although nascent, is highly concentrated and the proposed acquisition would cause a significant increase in the concentration level by reducing the number of competitors from three to two.

IV. ANTICOMPETITIVE EFFECTS FROM ELIMINATING ONE OF THE BIG THREE ARE GREATER THAN INDICATED BY CONCENTRATION FIGURES ALONE

65. The concentration measures described above, while giving rise to a presumption that the proposed acquisition would substantially lessen competition, likely understate the extent to which the transaction would result in anticompetitive effects such as higher prices, lower service levels, and less innovation in the relevant markets.

66. As two of the three largest global integrated oilfield services providers, Halliburton and Baker Hughes compete particularly aggressively with each other. They bid head to head for business in the relevant markets as well as many other markets, and offer similar types of integrated solutions, bundled services, and other multiple-product and service combinations. They have the ability to deal with global customers in countries around the world. They play leading roles in driving technological innovation, integration efficiencies, and service quality for the industry. They closely track, and respond to, each other's prices, products and technologies, and financial metrics. They compete for similar types of projects, particularly higher-end and more demanding work required by E&P companies.

67. Defendants recognize that the competitive choices for E&P companies needing complex services are limited. For example, executives in Halliburton's drilling services business have observed that "[c]ompetition reduces to the big three as the complexity of the wells increases." Likewise, Halliburton's President stated at an industry conference that the deepwater Gulf of Mexico is "[v]ery technologically demanding" and that there is a "significant barrier of entry as a business." Therefore, "only three service companies (HAL, SLB, BHI) can handle the full breadth of this work."

68. In some instances, the Big Three oilfield services providers are the only qualified suppliers bidding for complex projects. For example, a major E&P company procuring an integrated suite of completion equipment for wells in the ultra-deepwater Gulf of Mexico turned to the Big Three because those were the only firms with the technical capability to meet the extreme temperature, pressure, and other conditions in these wells. Some of the products necessary to build these wells did not yet exist, and the company decided to pit Halliburton and Baker Hughes against each other in a "design challenge" to create the best solution. Both Halliburton and Baker Hughes invested substantial resources in research and development to win this challenge. Reducing the number of bidders from three to two for these types of projects would represent a very significant reduction in competition, with the effects being especially acute for those projects where a customer needs to award contracts to two qualified suppliers.

69. Halliburton and Baker Hughes continue to push one another to develop the most advanced technologies for E&P companies. Each company has engaged in competing research efforts to bring what they refer to as "game changing" or "disruptive" new technologies to market first, or to surpass each other's existing technology, in such areas as dissolvable frac plugs, drilling automation, and integrated refracturing, among others. Defendants have stated that they plan to eliminate expenditures on overlapping research projects after the proposed acquisition. The acquisition would end competition between the Halliburton and the Baker Hughes versions of key emerging technologies.

70. Thus, the elimination of competition between Halliburton and Baker Hughes would have more profound anticompetitive effects than market shares and HHI measures alone would indicate. These anticompetitive effects would likely include unilateral effects in the form of higher prices, lower service levels and less innovation, as well as greater coordination among the remaining competitors.

V. ABSENCE OF COUNTERVAILING FACTORS

71. Entry is unlikely to prevent or remedy the merger's likely anticompetitive effects. Barriers to entry include the resources necessary to create products and build service capabilities; the need for scale; the need for an established record of safety, reliability, and efficiency to qualify for many projects; the need for substantial resources dedicated to product development; and the importance of having a wide portfolio of services to allow for integrated offerings.

72. Although Defendants assert that the proposed acquisition may produce efficiencies, they cannot demonstrate acquisition-specific and cognizable efficiencies that would offset the proposed acquisition's anticompetitive effects in the relevant markets.

73. As described in paragraphs 8-10 above, Halliburton has proposed divesting certain assets in an attempt to remedy the anticompetitive effects of the transaction, and Defendants may raise these proposed divestitures as a remedy in this case. The proposed package would include a mix of assets extracted from Halliburton's Sperry Drilling business, from Halliburton's drill bits business, from Baker Hughes' fluids business, from Baker Hughes' completions business, and from Baker Hughes' cementing business. Although Halliburton has had lengthy discussions with a prospective buyer, the scope of the asset package has been a moving target and the parties have not entered into an asset purchase agreement.

74. The proposed divestiture package, as it has been described to the United States, has numerous problems that make it unlikely to replicate the competition that would be lost as a result of the proposed merger. The proposed divestiture would fail to transfer intact businesses to the buyer. For example, although Sperry Drilling competes by offering a number of services relating to drilling, at least some of these, such as optimized pressure drilling, are being held back from the divestiture. With respect to cementing, drilling fluids and completion fluids, the proposal contemplates dividing offshore assets from onshore assets, keeping most of the onshore assets with the merged company and transferring offshore assets to the divestiture buyer, even though this will necessitate dividing facilities, R&D, intellectual property and personnel. No divestiture of either Defendant's wireline business is contemplated -- just the non-exclusive licensing of certain IP rights and the transfer of some personnel. Similarly, the proposal does not contemplate the divestiture of assets that would allow the buyer to replicate the level of development and implementation of integrated refracturing solutions that is currently being pursued by Halliburton and Baker Hughes.

75. Another serious problem with the proposal as it has been described to the United States is that it contemplates the division of hundreds of facilities across the world currently used by the divestiture assets, with the merged company retaining the majority of these facilities. This is likely to be highly disruptive to the businesses at issue. Based on materials presented by Defendants to the United States, it appears that fewer than half of the more than 400 facilities worldwide that have been used by the divestiture assets (for example, for production, service, R&D, sales, etc.) would be divested.

76. Yet another serious problem arises because many of the contracts that relate to the divestiture assets, including customer contracts and technology in-licenses, cannot be assigned to the divestiture buyer without the consent of the counterparties. There are hundreds of such contracts. Also, many permits and licenses from around the world that are required to engage in the businesses at issue cannot be assigned at all; the divestiture buyer would have to go through a new permitting and licensing process.

77. The fact that Defendants are not transferring any complete businesses to the divestiture buyer means that Halliburton and the buyer would need to enter into numerous support agreements that would leave the buyer dependent on one of its biggest competitors to operate successfully. These services would include, among other things, sharing and supporting essential software, supplying products, assisting with R&D, offering shared space in facilities, providing testing services and repair services, and even assisting with supplying services on customer contracts for which Halliburton competes.

78. Another concern with the proposed remedy is that Halliburton would generally retain the more valuable assets from either Defendant while divesting the less significant assets. This makes the buyer even less likely to replace the competition lost from the merger.

79. The examples described above illustrate just some of the many issues that would arise if the Court were to accept Halliburton's proposed divestitures as a remedy. In addition, both the Court and the United States would have to regulate over many years what amounts to a major reorganization of the global oilfield services industry involving the division, sharing, and transfer of hundreds of facilities, thousands of employees, thousands of patents, hundreds of contracts, and numerous other assets across dozens of countries. A remedy involving this level of complexity and risk to competition in a merger case and over the objection of the United States would be unprecedented and should be rejected by the Court.

VI. VIOLATION ALLEGED

80. The United States alleges and incorporates paragraphs 1 through 79 as if set forth fully herein.

81. The United States brings this action, and this Court has subj ect-matter jurisdiction over this action, under Section 15 of the Clayton Act, as amended, 15 U.S.C. § 25, to prevent and restrain Defendants from violating Section 7 of the Clayton Act, as amended, 15 U.S.C. § 18.

82. Defendants are engaged in, and their activities substantially affect, interstate commerce. Halliburton and Baker Hughes provide products and services to numerous customers located throughout the United States.

83. This Court has personal jurisdiction over each Defendant. Both Halliburton and Baker Hughes are incorporated in the State of Delaware and are inhabitants of this District. Halliburton's acquisition of Baker Hughes would have effects throughout the United States, including in this District.

84. Venue is proper under Section 12 of the Clayton Act, 15 U.S.C. § 22, and under 28 U.S.C. §§ 1391(b) and (c).

85. The effect of the proposed transaction, if approved, likely would be to lessen competition substantially, and to tend to create monopoly, in interstate trade and commerce in the relevant markets, in violation of Section 7 of the Clayton Act, 15 U.S.C. § 18.

86. Among other things, the transaction would likely have the following effects:

(a) Eliminating significant present and future head-to-head competition between Halliburton and Baker Hughes in the relevant markets;

(b) Causing prices to rise for customers in the relevant markets;

(c) Causing a reduction in service quality in the relevant markets; and

(d) Reducing competition over innovation and new product development.

VII. REQUEST FOR RELIEF

87. The United States requests:

(a) That the acquisition of Baker Hughes by Halliburton be adjudged to violate Section 7 of the Clayton Act, 15 U.S.C. § 18;

(b) That Defendants be permanently enjoined and restrained from carrying out the planned acquisition of Baker Hughes by Halliburton or any other transaction that would combine the two companies;

(c) That the United States be awarded its costs of this action; and

(d) That the United States be awarded such other relief as the Court may deem just and proper.

Respectfully submitted, FOR PLAINTIFF UNITED STATES

OF AMERICA

[Signature]

WILLIAM J. BAER

Assistant Attorney General

Antitrust Division[Signature]

JOHN R. READ

ANGELA L. HUGHES

BLAKE W. RUSHFORTH[Signature]

DAVID I. GELFANI

Deputy Assistant Attorney GeneralTrial Attorneys

Antitrust Division

United States Department of Justice

450 Fifth Street, NW

Washington, DC 20530

Telephone: (202) 307-0468

Facsimile: (202) 307-2784

Email: john.read@usdoj.gov[Signature]

PATRICIA A. BRINK

Director of Civil Enforcement[Signature]

KATHLEEN S. O'NEILL

Chief, Transportation, Energy,

and Agriculture SectionCHARLES M. OBERLY, III

United States Attorney[Signature]

JENNIFER HALL (#5122)

Assistant United States Attorney

United States Attorney's Office

1007 Orange Street, Suite 700

Wilmington, DE 19801

(302) 573-6277

jennifer.hall@usdoj.govDated: April 6, 2016

APPENDIX

Herfindahl-Hirschman Index

The Herfindahl-Hirschman Index ("HHI") is a commonly accepted measure of market concentration. The HHI is calculated by squaring the market share of each firm competing in the relevant market and then summing the resulting numbers. For example, for a market consisting of four firms with shares of 30, 30, 20, and 20 percent, the HHI is 2,600 (302 + 302 + 202 + 202 = 2,600). The HHI takes into account the relative size distribution of the firms in a market. It approaches zero when a market is occupied by a large number of firms of relatively equal size, and reaches its maximum of 10,000 points when a market is controlled by a single firm. The HHI increases both as the number of firms in the market decreases and as the disparity in size between those firms increases.

Economic, Social and Cultural Rights

| This document has been published on 11Jul16 by the Equipo Nizkor and Derechos Human Rights. In accordance with Title 17 U.S.C. Section 107, this material is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. |