| Information |  | |

Derechos | Equipo Nizkor

| ||

| Information | | |

Derechos | Equipo Nizkor

| ||

31Dec14

U.S. Crude Oil Export Policy: Background and Considerations

Contents

The Energy Policy and Conservation Act

The Export Administration Act and the International Emergency Economic Powers Act

Other Relevant Federal StatutesSection 201 of P.L. 104-58: Exports of Alaskan North Slope Oil

The Role of the Bureau of Industry and Security (BIS)

MLA Limitation on Export of Crude Oil Transported via Federal Right-of-Way

Limitation on Export of Oil from the Naval Petroleum Reserves

Limitation on Export of Crude Oil Produced from the Outer Continental ShelfTight Oil Production Has Increased

U.S. Refinery Configurations

Infrastructure Challenges

Crude Oil Producer PricesPrice Effects

Crude Oil Prices

Energy Security and Geopolitics

Product Prices

International Trade Policy

EnvironmentOil Transportation

Federal Revenue Collections

Oil Extraction

Climate ChangeRemove Existing Restrictions

Maintain Current Restrictions

Modify RestrictionsFigures

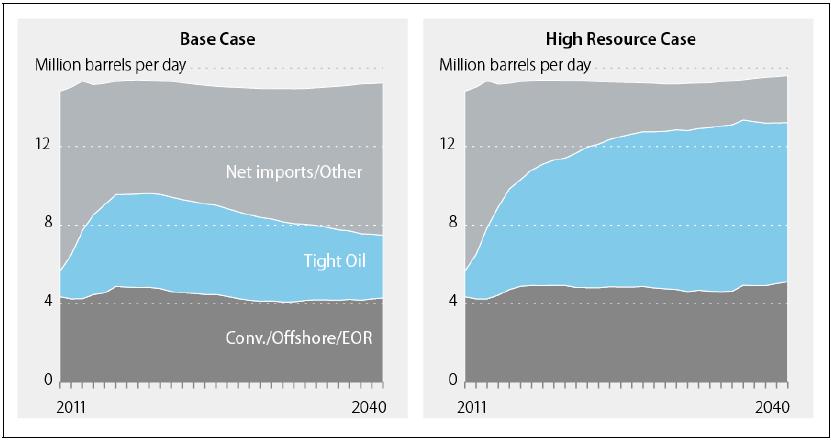

Figure 1. U.S. Crude Oil Supply Projections (Base and High Resource Cases)

Figure 2. U.S. Tight Oil Production, by Formation

Figure 3. Oil Refining Capacity and Coking Refinery Capacity by PADD

Figure 4. PADD 3 Light, Sweet Crude Oil Imports

Figure 5. Major U.S. and Canadian Crude Oil Pipelines

Figure A-1. Price History for Selected Crude Oil Types

Figure C-1. Simplified Diagram of Lease Condensate Stabilization and DistillationTables

Table B-1. Comparison of Crude Oil Export Policy Economic Impact Studies

Appendixes

Appendix A. Crude Oil Price History

Appendix B. Comparison of Economic Impact Studies

Appendix C. Processed Condensate Exports: A Change in Energy Policy?

Summary

During an era of oil price controls and following the 1973 Organization of Arab Petroleum Exporting Countries oil embargo, Congress passed the Energy Policy and Conservation Act of 1975 (EPCA), which directs the President "to promulgate a rule prohibiting the export of crude oil" produced in the United States. Crude oil export restrictions are codified in the Export Administration Regulations administered by the Bureau of Industry and Security (BIS)--a Commerce Department agency. Generally, U.S. crude oil exports are prohibited, although there are a number of exemptions and circumstances under which crude oil exports are allowed. The President has authority to allow certain crude oil exports if an exemption is determined to be in the national interest.

In 2009, a decades-long U.S. oil production decline was reversed due to the application of advanced drilling and extraction technologies to produce tight oil, generally light/sweet crude primarily located in Texas and North Dakota. Limited demand for tight oil and condensate being produced in the Texas/Gulf Coast region may result because certain refiners in that region are currently configured to process heavier crudes. As a result, oil producers and industry analysts are projecting an oversupply of light oil, which could lead to price discounts and lower production should export restrictions remain. However, the industry is dynamic, and refiners can modify operating configurations and add equipment in order to accommodate more light crude volumes. Price discounts may be needed to motivate such changes.

The effect on domestic gasoline prices is a major consideration, among several, associated with allowing crude oil exports. Commercial studies and federal government analysis suggests that gasoline prices are correlated to international crude oil prices--since gasoline and other petroleum products can be exported without restriction--and U.S. gasoline prices could possibly decrease if crude oil exports were allowed. However, the projected decreases--assuming ~$100 per barrel crude oil prices--are relatively small and range from $0.02 to $0.12 per gallon.

Congress may choose to consider crude oil export policy options that could range from maintaining existing restrictions to eliminating the prohibition on crude oil exports. During the 113th Con gress, four bills were introduced that would have eliminated crude oil export restrictions: H.R. 4286, H.R. 4349, S. 2170, and H.R. 5814. Some Members of Congress have expressed the desire to maintain crude oil restrictions. However, maintaining restrictions might not prevent more crude-oil-like material from being exported, because varying interpretations of existing regulations may allow for more exports. The crude oil definition in the export regulations is open to interpretation and has many undefined terms that the industry may explore with the objective of determining the minimum amount of crude oil processing necessary that would result in an exportable product. It is not clear how broadly or narrowly BIS might interpret existing laws and regulations.

Finally, Congress may choose to explore other options between eliminating and maintaining restrictions. Examples may include allowing exports of lease condensate--an ultralight hydrocarbon that is typically produced with natural gas--allowing unrestricted exports to Mexico since exports to Canada are not restricted, allowing a certain type of crude (i.e., light/sweet) from a certain location (i.e., Texas) to be exported--much like the California heavy crude oil export exemption--or allowing crude oil exports for a limited time period since U.S. oil production growth is uncertain and may, according to the Energy Information Administration, peak in 2020.

The President has the authority to make national interest determinations that would allow for more crude oil exports.

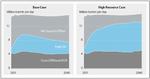

As a result of advanced oil drilling and extraction technologies (primarily horizontal drilling and hydraulic fracturing), crude oil production in the United States is growing and, according to Energy Information Administration (EIA) reference case projections, may reach 9.6 million barrels per day (bbl/d) by 2019 (see Figure 1)--up from 5 million bbl/d in 2008. |1| Production of light tight oil (LTO) is, and is expected to be, the primary contributor to U.S. crude oil production growth in the near to medium term. |2| As U.S. LTO production has increased, some have called for crude oil export restrictions to be either eased or lifted altogether. |3| However, according to the EIA, U.S. crude oil demand is forecasted to be approximately 15 million bbl/d through 2040. |4| EIA's reference case indicates that crude oil imports are projected to range between 6 million and 8 million bbl/d over the same period. |5| However, EIA's high resource case projections, if realized, could result in lower crude oil import requirements (2 to 4 million barrels per day from 2020 to 2040). |6| This apparent disconnect between expected import needs and the desire to export crude oil can be explained when considering crude oil prices can be influenced by the following: (1) the geographical location of LTO production, (2) the type/quality (i.e., light, sweet) of crude oil being produced, (3) the types of crude oil that some U.S. refineries are currently configured to optimally refine, (4) the petroleum products that are derived from different types of crude oil, and (5) transportation and infrastructure challenges associated with moving certain types of crude oil to demand centers. Each of these aspects is discussed in more detail throughout this report.

Figure 1. U.S. Crude Oil Supply Projections (Base and High Resource Cases)

2011-2040

Click to enlargeSource: Energy Information Administration, Annual Energy Outlook 2014.

Notes: EOR = Enhanced Oil RecoveryWhile U.S. crude oil exports are restricted under current law, petroleum products such as naphtha |7|, gasoline, diesel fuel, and natural gas liquids (NGLs) are not subject to export restrictions. As a result, production and export of these products have increased in recent years. In August 2014, approximately 4.1 million barrels per day (bbl/d) of petroleum products, NGLs, and other liquids were exported from the United States--up from an average of nearly 1.4 million bbl/d in 2007. |8|

Members of Congress have taken various positions regarding crude oil exports, including (1) calling for the Administration to lift export restrictions, |9| (2) maintaining existing restrictions, |10| (3) opposing attempts to lift restrictions through the World Trade Organization, |11| and (4) proposing bills to eliminate crude oil export restrictions (see section below titled "Legislative Action").

The crude oil export policy debate has multiple dimensions and complexities. As U.S. LTO production has increased--along with additional oil supply from Canada--certain challenges have emerged that affect some oil producers and refiners. While the economic arguments both for and against U.S. crude oil exports are quite complex and dynamic, there are some fundamental concepts and issues that may be worth considering during debate about exporting U.S. crude oil. This report provides background and context about the crude oil legal and regulatory framework, discusses motivations that underlie the desire to export U.S. crude oil, and presents analysis of issues that Congress may choose to consider during debate about U.S. crude oil export policy.

Current crude oil export restrictions date back to the 1970s, during an era of U.S. oil price controls that motivated producers to export and sell crude oil at unregulated world prices. |12| In response, crude oil, petroleum products, and natural gas liquids were placed on the Commodity Control List established by the Export Administration Act of 1969. |13| In 1973, the Organization of Arab Petroleum Exporting Countries (OAPEC) imposed a total embargo of crude oil delivered to the United States. |14| The oil embargo motivated Congress to enact laws that would limit U.S. crude oil export opportunities. |15| The embargo resulted in rapid and steep crude oil price increases, thereby creating a perception of oil resource scarcity and prompting concerns about U.S. crude oil import reliance. |16| In response to these concerns Congress passed legislation--including the Energy Policy and Conservation Act (EPCA)--to restrict U.S. crude oil exports, with some exceptions as determined by the President. Using these exceptions, the United States has exported crude oil for decades, although in relatively low volumes. Crude oil exports reached a level of 287,000 bbl/d on average in 1980. |17| In 2002, crude oil exports averaged 9,000 bbl/d. Since then, crude oil exports have steadily increased and reached 401,000 bbl/d during the month of July 2014. |18| The majority of these exports were sent to Canada. |19|

In the context of exports, the Bureau of Industry and Security (BIS)--the Department of Commerce agency responsible for crude oil export licenses--defines "crude oil" as follows:

"Crude oil" is defined as a mixture of hydrocarbons that existed in liquid phase in underground reservoirs and remains liquid at atmospheric pressure after passing through surface separating facilities and which has not been processed through a crude oil distillation tower. Included are reconstituted crude petroleum, and lease condensate and liquid hydrocarbons produced from tar sands, gilsonite, and oil shale. Drip gases are also included, but topped crude oil, residual oil, and other finished and unfinished oils are excluded. |20|

From 1970 to 2008, U.S. crude oil production was on a steady decline. During this time, there were periods when easing crude oil export restrictions was a national-level policy topic and presidential determinations were made to exempt crude oil exports that met certain criteria. In 2009, production of light/sweet crude in tight oil formations throughout the country started to increase rapidly, and production levels are expected to continue rising out to 2019, or perhaps later.

The physical and chemical properties of LTO, when placed into context of the crude oil slate |21| desired by U.S. refineries, is one important factor that underlies the crude oil export debate. For more information about crude oil characteristics, see the text box below.

All Crude Oil Is Not Created Equal Hundreds of different types of crude oil are produced globally, each of which has unique qualities and characteristics. Two of the most common parameters used to compare different types of crude oil are (1) API gravity, and (2) sulfur content. API gravity, expressed in degrees, indicates the density of crude oil. The higher the API gravity, the lighter the crude oil. Sulfur content, expressed as a percentage, indicates the amount of sulfur contained in a particular crude stream. High sulfur content crudes are referred to as "sour" and low sulfur content crudes are referred to as "sweet." |22| Additionally, when processed by a refinery, different crude oils can yield varying amounts of petroleum products such as gasoline, diesel fuel, jet fuel, and fuel oil. The following table compares five different types of crude oil based on API, sulfur content, and initial product yield.

Initial Product Yield (Volume %)

Crude Oil (Yr) APIş Sulfur (%) Resid Gas oil Distillate Naphtha Other Maya ('07) 20.5 (H) 3.65 (Sr) 36 14 21 18 1 Arabian Heavy ('01) 27.5 (H) 2.78 (Sr) 30 25 24 18 3 Eagle Ford Cond. ('11) 55.6 (XL) 0.01 (Swt) 1 15 31 48 5 Eagle Ford 40 ('12) 40.1 (L) 0.09 (Swt) 11 28 33 26 2 West Texas Sour ('01) 32.4 (M) 1.72 (Sr) 14 29 29 27 1 Source: API and sulfur numbers from EIA; product yields from Chevron Assays.

Notes: Product yields represent typical initial yields off atmospheric and vacuum towers, which is generally the first step in the refining process. Additional processing steps (i.e., cracking, coking, combining, etc.) are used to produce finished products such as gasoline, diesel fuel, and others. Individual refineries are typically configured to handle a certain blend of crude oils that will produce an optimized volume of initial and finished products. H = Heavy; M = Medium; L = Light; XL = Extra Light; Sr = Sour; Swt = Sweet; Cond. = condensate.

Definitions: (1) Resid represents residual fuel oil, which is a general classification for heavier oils that can be used as feedstock for a coking refinery; (2) Gas oil refers to fuel oils that are lighter than resid but heavier than distillate and can include certain heating oils and fuels; (3) Distillate can be used as either a diesel fuel or a fuel oil; (4) Naphtha can be blended with other materials to produce motor gasoline or jet fuel. Naphtha can also be used as a solvent or as a petrochemical feedstock; (5) Other generally refers to light refinery gases such as butane and propane.Oil refiners, which process a blend of different crude oils, generally look to optimize the type/quality of crude streams to produce the desired product (i.e., gasoline and diesel fuel) output based on price (crude oil prices and product values) and other market conditions. The technical configuration, product markets, and economic conditions for each individual refinery will affect the desired crude oil selection.

Prior to the advent of advanced drilling and extraction technologies, many U.S. refiners in the Midwest and Gulf Coast invested in equipment to process heavy crudes from Canada and Latin America. Generally, these investments were encouraged by price discounts for heavy crudes. Tight oil production has changed the situation and the entire industry is adjusting. Investments are being made to process more light crude. Transportation bottlenecks are being relieved. However, as LTO volumes increase, oil producers are bracing for continuing price discounts that may result from a structural oversupply of light crudes in certain regions. Whether the industry will be economically motivated to continue adjusting to accommodate expected light crude production and supply is uncertain.

The export of domestically produced crude oil has been significantly restricted since the 1970s by an array of federal laws and regulations, in particular the Energy Policy and Conservation Act of 1975 (EPCA) |23| and the resultant Short Supply Control Regulations adopted and administered by the Bureau of Industry and Security (BIS). These laws and regulations are discussed below.

The Energy Policy and Conservation Act

EPCA directs the President to "promulgate a rule prohibiting the export of crude oil and natural gas produced in the United States, except that the President may ... exempt from such prohibition such crude oil or natural gas exports which he determines to be consistent with the national interest and the purposes of this chapter." |24| The act further provides that the exemptions to the prohibition should be "based on the purpose for export, class of seller or purchaser, country of destination, or any other reasonable classification or basis as the President determines to be appropriate and consistent with the national interest and the purposes of this chapter." |25|

This general prohibition on crude oil exports and the exemptions to that prohibition mandated by EPCA are found in the BIS regulations on Short Supply Controls at 15 C.F.R. §754.2. The regulations provide that a license must be obtained for all exports of crude oil, including those to Canada. |26| There are enumerated exceptions to the license requirement for foreign origin crude oil stored in the Strategic Petroleum Reserves, |27| small samples exported for analytic and testing purposes, |28| and exports of oil transported by pipeline over rights-of-way granted pursuant to Section 203 of the Trans-Alaska Pipeline Authorization Act. |29|

The regulations provide that BIS will issue licenses for certain crude oil exports that fall under one of the listed exemptions, including (1) exports from Alaska's Cook Inlet; (2) exports to Canada for consumption or use therein; (3) exports in connection with refining or exchange of Strategic Petroleum Reserve oil; (4) exports of heavy California crude oil up to an average volume not to exceed 25,000 barrels per day; (5) exports that are consistent with certain international agreements; (6) exports that are consistent with findings made by the President under certain statutes (see section below titled "Other Relevant Federal Statutes"); and (7) exports of foreign origin crude oil where, based on satisfactory written documentation, the exporter can demonstrate that the oil is not of U.S. origin and has not been commingled with oil of U.S. origin. |30|

The regulations also direct BIS to review applications to export crude oil that do not fall under one of these exemptions on a "case by case basis" and to approve such applications on a finding that the proposed export is "consistent with the national interest and the purposes of the Energy Policy and Conservation Act." |31| However, the regulations suggest that only certain specific exports will be authorized pursuant to this case-by-case review. The regulations provide that while BIS "will consider all applications for approval," generally BIS will only approve those applications that are either for temporary exports (e.g., a pipeline that crosses an international border before returning to the United States), or are for transactions (1) that result directly in importation of an equal or greater quantity and quality of crude oil; (2) that take place under contracts that can be terminated if petroleum supplies of the United States are threatened; and (3) for which the applicant can demonstrate that for compelling economic or technological reasons, the crude oil cannot reasonably be marketed in the United States |32| For additional information about these types of transactions, see the text box below.

Crude Oil Exchanges and Swaps Are Distinctly Different The BIS crude oil export regulations allow for exchanges with other countries and swaps with an "adjacent foreign state," as long as certain criteria are met. It is important to recognize that exchanges and swaps are two distinctly different types of crude oil export transaction, and each has different criteria. Exchange transactions are allowed between the United States and other countries as long as the following criteria are met:

(1) For exported crude oil, it must be demonstrated that the exported crude oil cannot be reasonably marketed in the United States for "compelling economic and technological reasons."

(2) The transaction will result in either the import of crude oil of equal or greater quantity and equal or better quality, or the import of petroleum product volumes equal to or greater than petroleum product volumes that would have been produced by refining the exported crude oil.

(3) The transaction takes place under a contract that can be terminated if U.S. petroleum supplies are interrupted or threatened. |33|

Exactly how the Department of Commerce might evaluate exchange applications is unclear; however, adhering to some of the criteria requirements may be difficult for applicants. |34| Furthermore, a license is required for each exchange transaction, and the criteria must be met for each exchange application. According to the Department of Commerce, no exchange transactions have ever been approved. |35|

Swap transactions, which are allowed between the United States and an "adjacent foreign state," are distinctly different from exchanges in that the stringent criteria required for exchanges need not be met. Swaps could be approved based on "convenience and increased efficiency of transportation," terms which are not defined in the regulations. Additionally, crude oil exported as part of a swap transaction may not be re-exported to another country. Criteria for swaps are much less onerous than those for exchanges, and a swap transaction may be the preferred option for exporting more light/sweet U.S. crude oil in exchange for heavy/sour crude from Mexico. |36|

The Export Administration Act and the International Emergency Economic Powers Act

Although EPCA directs the President to promulgate regulations that restrict crude oil exports, it does not provide the regulatory framework for enforcement of that restriction and the issuance of licenses for eligible exports. As mentioned above, the BIS is tasked with that duty, which is handled under its "short supply control" regulations. The source of this authority is somewhat complicated. The Export Administration Act of 1979 (EAA) |37| confers upon the President the power to control exports for national security, foreign policy, or short-supply purposes, authorizes the President to establish export licensing mechanisms for certain items, and provides guidance and places certain limits on that authority. |38| These restrictions are enforced by BIS. Crude oil restrictions and licensing are found in the BIS short supply controls authorized by the EAA.

However, the EAA expired in August 2001. The provisions of the act, and the regulations issued pursuant to it, remain in effect by a presidential declaration of a national emergency and the invocation of the International Emergency Economic Powers Act (IEEPA). |39| That act authorizes the President to "deal with any unusual and extraordinary threat, which has its source in whole or substantial part outside the United States, to the national security, foreign policy, or economy of the United States, if the President declares a national emergency with respect to such threat." |40| When the EAA most recently expired in 2001, the President cited this emergency authority in the issuance of Executive Order 13222, which provided for the continued execution of the EAA and the regulations issued pursuant to it. |41| The continuation of emergency authority has been extended annually by the President since that time, most recently in August 2013. |42|

Other Relevant Federal Statutes

In addition to the statutes described above, several other federal statutes either bar certain types of crude oil exports or mandate that certain crude oil exports be exempt from the general prohibition in EPCA.

Section 201 of P.L. 104-58: Exports of Alaskan North Slope Oil

Section 201 of P.L. 104-58 amended the Mineral Leasing Act (MLA) |43| to authorize the export of oil transported by pipeline over the right-of-way granted pursuant to the Trans-Alaska Pipeline Authorization Act unless the President finds that export of this oil is not in the national interest. |44| The President's national interest determination must, at a minimum, consider (1) whether the export will diminish the quantity or quality of petroleum available in the United States; (2) the results of an environmental review; and (3) whether the export might cause sustained material oil supply shortages or significantly increase oil prices above world market levels. |45| The legislation required submission of this national interest determination within five months of November 28, 1995. |46|

In April 1996, President Clinton issued a determination that such exports were in the national interest. |47| BIS administers authorizations of Trans-Alaska Pipeline System oil exports pursuant to 15 C.F.R. §754.2(j), which carves out an exception to the general crude oil export licensing requirements provided that certain conditions regarding the physical transportation of the crude oil are satisfied.

MLA Limitation on Export of Crude Oil Transported via Federal Right-of-Way

Section 28(u) of the MLA clarifies that all domestically produced crude oil (except oil exchanged for similar quantities for purposes of convenience or efficiency) transported through federal lands via rights-of-way granted pursuant to the MLA "shall be subject to all of the limitations and licensing requirements of the Export Administration Act." |48| Section 28(u) also provides that before such exports may occur, the President must "make and publish an express finding that such exports will not diminish the total quantity or quality of petroleum available in the United States, and are in the national interest and are in accord with the provisions of the Export Administration Act." |49| The MLA further directs the President to submit reports to Congress containing these findings, and provides that Congress "shall have a period of sixty days, thirty days of which Congress must have been in session, to consider whether exports under the terms of this section are in the national interest. If Congress ... passes a concurrent resolution of disapproval stating disagreement with the President's finding concerning the national interest, further exports ... shall cease." |50| The MLA restriction on exports of crude oil that are transported through federal lands via a right-of-way is incorporated into the BIS regulations at 15 C.F.R. §754.2(c)(ii).

Limitation on Export of Oil from the Naval Petroleum Reserves

10 U.S.C. §7430(e) provides that petroleum produced at the naval petroleum reserves (except petroleum exchanged for similar quantities for purposes of convenience or efficiency) "shall be subject to all of the limitations and licensing requirements of the Export Administration Act." Section 7430(e) also provides that before such exports can take place, the President must "make and publish an express finding that such exports will not diminish the total quantity or quality of petroleum available in the United States, and are in the national interest and are in accord with the provisions of the Export Administration Act." |51| The Section 7430(e) restriction on exports of petroleum produced at the naval petroleum reserves is incorporated into the BIS regulations at 15 C.F.R. §754.2(c)(iv).

Limitation on Export of Crude Oil Produced from the Outer Continental Shelf

Section 28 of the Outer Continental Shelf Lands Act (OCSLA) |52| provides that any oil or gas produced from the Outer Continental Shelf (OCS) |53| "shall be subject to all of the limitations and licensing requirements of the Export Administration Act." As with the statutory export limitations discussed above, exports meeting this description are only authorized if the President makes "an express finding that such exports will not increase reliance on imported oil or gas, are in the national interest, and are in accord with the provisions of the Export Administration Act." |54| The OCSLA requires the President to submit reports containing such findings to Congress and provides that Congress "shall have a period of sixty calendar days, thirty days of which Congress must have been in session, to consider whether exports under the terms of this section are in the national interest. If the Congress ... passes a concurrent resolution of disapproval stating disagreement with the President's finding concerning the national interest, further exports ... shall cease." |55| The OCSLA restriction on exports of petroleum produced from the OCS is incorporated into the BIS regulations at 15 C.F.R. §754.2(c)(iii).

The Role of the Bureau of Industry and Security (BIS)

As noted above, exports of crude oil are licensed under the short supply controls of the Export Administration Act. The Export Administration Regulations (EAR) codify the requirements and provisions of the various statutes restricting crude oil exports, which are administered by the Bureau of Industry and Security. Except in certain instances, a license is required for the export of crude oil from the United States.

License applications are examined by the Office of National Security and Technology Transfer Controls at BIS. Only a U.S. exporter or entity may apply for a license. License applications are made electronically, thus one must register on the BIS Simplified Network Application Process Redesign (SNAP-R). |56| Once registered, the applicant must list the exporter, consignee, the volume of the export and its monetary value, a description of the product, its end-use, and a certification of origin for the product.

All BIS license applications are handled according to Executive Order 12981. Within nine days, BIS must contact the applicant if additional information is required; return without action if additional information is required or if a license is not needed; or refer the application to another agency. Once an application has been submitted, BIS has 30 days to make a decision. However, unlike dual-use technology licenses, crude oil licenses are not referred to other agencies. Thus, most crude oil licenses are handled within a 7-10 day period. A license is good for one year and is non-transferable, unless it is part of the assets of a company being bought or sold.

Certain crude oil exports can be shipped with a license exception. A license exception is an authorization to export or re-export, under certain conditions, items subject to the EAR that normally would require a license. Basically, under a license exception, the exporter certifies that a lawful transaction is taking place while maintaining proper documentation. The three license exceptions available for crude oil exports are (1) shipments of foreign-origin crude stored in the Strategic Petroleum Reserve; (2) shipments of samples for analytic or testing purposes; and (3) Trans-Alaska pipeline shipments. In order to use the TAPS license exception, certain tanker routing and environmental restrictions must be observed. Additionally, vessels used to export TAPS crude oil must be U.S.-owned and crewed. In addition, the licenses allow no re-exports, thus, prohibiting, for example, trans-shipments to foreign destinations through Canada.

The number of crude oil license applications has steadily increased over the last few years, from 31 applications in FY2008 to 189 in FY2014. In the last several years, no licenses have been rejected, although some have been returned without action. This high approval rate is likely due to the specificity and exporters' knowledge of the regulations. The vast majority of licenses are for exports to Canada. For countries other than Canada, the exports can be attributed to re-exports of foreign crude oil (mostly Canadian crude) that has not been commingled with domestic crude. |57|

As tight oil production has rapidly increased, technical and economic factors are motivating some stakeholders to pursue lifting crude oil export restrictions. Some oil producers would like to receive higher prices for oil produced. However, some refiners are concerned that regional crude oil acquisition price discounts may narrow if exports are expanded. Narrow price discounts may affect refinery operating margins and may result in some refineries ceasing operations. Additionally, some refiners may need to consider capital investments necessary to absorb increasing volumes of LTO--along with the value of products yielded from refining LTO. As mentioned above, the geographic location of tight oil production, refinery configurations, infrastructure limitations, and prices received by some oil producers have been cited as justification for lifting export restrictions. However, it is important to realize that these factors are not static in nature. Rather, the industry is dynamic and is constantly changing. Refineries can adjust their operations. Transportation infrastructure can adjust based on market conditions. Therefore, oil values received by oil producers would likely adjust as well. In 2013, the Energy Information Administration stated:

Some recent commentary has suggested that it was likely or even inevitable that the growth in U.S. oil production from tight resources would be significantly curtailed unless there was a relaxation of current U.S. policies toward crude oil exports. However, this is likely an overstatement of the actual situation, because there are several other midstream and downstream adjustments that could help to accommodate changing production patterns. |58|

The dynamic nature of the oil industry makes the debate about oil export policy inherently complex. Each of the three primary industry segments--production, transportation, and refining--will adjust based on changes to any one of the other segments. As a result, it can be difficult to assess the potential impacts of policy decisions on any one segment without considering how the other two might adjust to changing market conditions. With that caveat, additional detail about some of the motivations for crude oil exports is provided in the following sections.

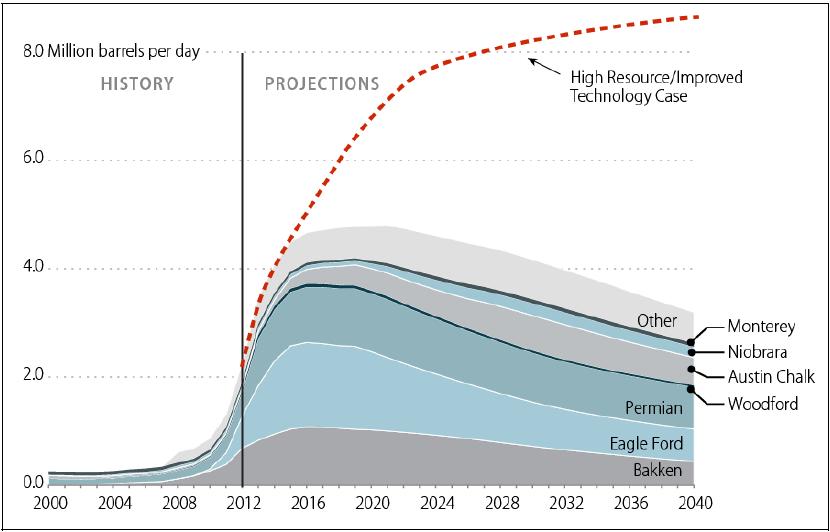

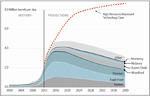

Tight Oil Production Has Increased

In 2000, approximately 250,000 bbl/d of tight oil was produced in the United States. |59| In 2013, U.S. tight oil production was approximately 3.5 million bbl/day, a nearly 14-fold increase. |60| The Energy Information Administration (EIA) 2014 reference case projects that U.S. tight oil production will continue to increase in the near to medium term and projects that LTO production may peak at 4.8 million bbl/day in 2021. |61| Most of this production is expected to come from three tight oil formations: (1) Eagle Ford in Texas, (2) Permian Basin in Texas, and (3) Bakken in North Dakota (see Figure 2). It is important to note that EIA projections for LTO production are subject to assumptions that are based on currently available information and current policies (e.g., export restrictions). These projections would likely change over time as new information becomes available and if policies are modified. For example, EIA's high resource case projects that tight oil may peak at 8.5 million barrels per day in 2035. |62| Some degree of uncertainty exists in terms of how much LTO might be produced. Future projections, and actual production, may be either higher or lower than those included in EIA's 2014 Annual Energy Outlook.

Timing for a potential oversupply, and resulting price discounts, of U.S. LTO is also uncertain and depends on several factors. Some analysts estimate that price discounts related to the combination of LTO production volumes and export restrictions may occur as early as 2015/2016 or sometime after 2020. |63| Some of the factors that will likely impact the timing and magnitude of price discounts include (1) actual LTO production levels, (2) potential for U.S. exports to Canada, (3) LTO access to West Coast markets, (4) potential to displace light sour and medium grade crudes in refineries, and (5) the amount of additional LTO processing capacity at refineries. |64|

Figure 2. U.S. Tight Oil Production, by Formation

(2000-2040 Reference Case est.)

Click to enlargeSource: Energy Information Administration, Annual Energy Outlook 2014.

Notes: The area chart shows EIA's reference case projections for tight oil production by formation. The red dashed line shows EIA's high resource/improved technology case for total tight oil production out to 2040. The disparity between these two projections illustrates some of the uncertainty associated with long-term tight oil production in the United States. Locations for tight oil formations are as follows: Bakken, North Dakota; Eagle Ford, Texas; Permian, Texas and New Mexico; Woodford, Oklahoma; Austin Chalk, Texas, Louisiana, and Mississippi; Niobrara, Colorado and Wyoming; Monterey, California.Based on EIA reference case projections in Figure 2, LTO production is projected to rapidly increase and peak around 2019. The implication of the reference case production profile is that the window of opportunity for crude oil exports--depending on export volumes--may be temporary. The potential temporary nature of the export opportunity may reflect the continuous and rapid drilling that may be needed to maintain and increase LTO volumes. Although, EIA's high resource case indicates that LTO may continue growing out to 2035. As noted above, actual and projected production can, and does, change over time. The high resource case reflects how industry knowledge could expand and technologies could improve, thereby resulting in increased U.S. LTO production in the future. LTO production at scale is a relatively new industry development and, thus, it is likely too early to accurately predict the magnitude of future production levels.

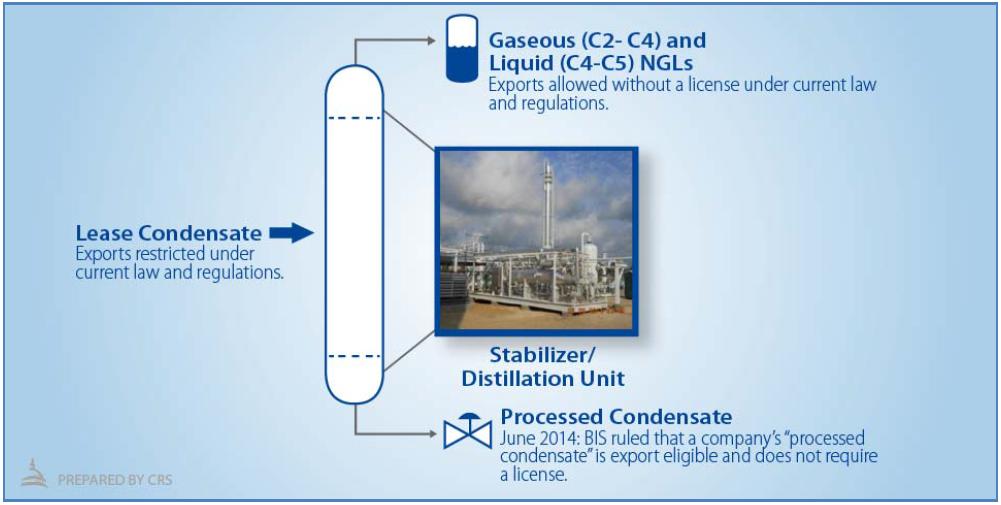

One element of LTO production is the increase in extremely light hydrocarbons that might be classified as lease condensate, which is subject to export restrictions. While there is no quality characteristic (i.e., API gravity) that defines lease condensate, increasing production volumes of condensate and condensate-like material is one aspect of the crude oil export debate. For additional information, see the text box below.

Lease Condensate: What Is It? Is It Crude Oil? Production of lease condensate, especially in the Texas Eagle Ford formation, has emerged as a topic of debate in the context of U.S. crude oil exports due to its ultra-light properties, limited marketability, and apparent price discounts to the WTI crude oil price benchmark. As the name implies, condensate is generally a gas underground. When produced along with oil and gas, it "condenses" into a liquid at atmospheric temperature and pressure. According to one source, the majority of Eagle Ford condensate is being produced from natural gas wells, not crude oil wells. |65| While "lease condensate" is included in the BIS crude oil definition, there is a potential contradiction within the definition. BIS defines crude oil as hydrocarbons that existed in liquid phase underground. However, condensate is generally in a gas phase underground and condenses to a liquid at atmospheric conditions. This apparent contradiction, along with other considerations, raises questions about the applicability of export restrictions to condensate.

As a point of comparison, the Energy Information Administration defines condensate as follows:

Condensate (lease condensate): Light liquid hydrocarbons recovered from lease separators or field facilities at associated and non-associated natural gas wells. Mostly pentanes [hydrocarbons with five carbon atoms] and heavier hydrocarbons. Normally enters the crude oil stream after production. |66|

There is no industry- or government-wide lease condensate definition nor are there standard quality characteristics-- such as API gravity--used to classify what is and is not lease condensate. Additionally, there is limited information available that quantifies actual and expected volumes of lease condensate produced on an annual basis, because lease condensate is typically classified as crude oil for reporting purposes. EIA does request condensate production data in its EIA Form-23 survey. However, each state has a unique lease condensate definition, and the self-reported results may not accurately reflect total production volumes. As a result, it can be difficult to accurately assess condensate production volumes when considering policy options that might allow this material to be exported. According to one estimate, lease condensate production in 2013 was approximately 1 million bbl/d and may reach 1.6 million bbl/d by 2018. |67| EIA is in the process of expanding existing surveys and creating new surveys that would collect condensate production data. Results from these efforts were not available as of the date of this report.

Furthermore, the EIA definition of condensate is very similar to the definition of "natural gasoline," which is defined as being "equivalent to pentanes plus." |68| Natural gasoline is a product of gas processing facilities. Some market analysts have indicated that depending on the season--winter or summer--identical hydrocarbons can be classified as either natural gasoline, which can be exported without restriction, or condensate, which is subject to export restrictions. |69|

Finally, the BIS crude oil definition states that crude oil hydrocarbons that have not passed through a distillation tower are subject to export restrictions. In order to comply with the regulation, investments are being made to install standalone condensate splitters--essentially a basic distillation tower--that separate the components (e.g., naphtha) of condensate. The resulting condensate components are eligible for export to international markets. In June 2014, the Bureau of Industry and Security ruled that processed condensate through a stabilizer/distillation unit can be exported without requiring a license. This decision sparked much debate about whether this represents a change in policy or an administrative ruling within the existing regulatory framework. It is important to note that the BIS crude oil definition is open to interpretation, and it is likely that the industry will pursue avenues within existing regulations to maximize the amount of minimally processed crude oil and condensate that can be exported. For additional information about the BIS processed condensate commodity classifications, see Appendix C. As a result of the above considerations, some industry stakeholders have called for condensate to be removed from the BIS definition. Some producers have begun self-classifying processed condensate and will be exporting more of this material in the absence of a commodity classification or a license from BIS. This is allowed under the current regulations. However, BIS released regulation guidance to applicants regarding processed condensate, including some factors that are considered when evaluating processed condensate commodity classification requests. |70|

Actual and projected LTO production levels are affecting the refining and infrastructure segments in a variety of ways, and vice versa. How these segments might adjust to changing market conditions (i.e., increased LTO production) will depend on multiple economic variables and investment considerations.

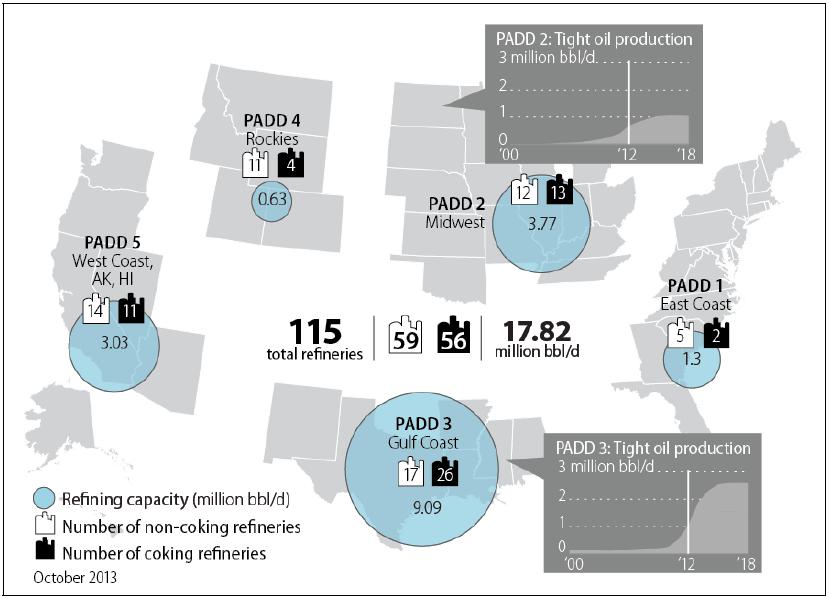

U.S. Refinery Configurations |71|

As of October 2013, there were 115 oil refineries in the United States with a total operable capacity of 17.8 million barrels per day of crude oil throughput. |72| Each refinery has its own unique configuration that is generally designed to economically optimize the use of a certain crude oil blend and the production of oil products that will maximize profit margins. In the context of exporting crude oil, refineries located in the Petroleum Administration for Defense District (PADD) 3 provide an illustration of some of the emerging complexities and economic decisions that are being considered as LTO production increases in the Gulf Coast area, and as Canadian and Midwest crudes are delivered to the region. |73|

There are 43 refineries located in PADD 3, with a total operable refining capacity of approximately 9.1 million barrels per day, the largest concentration of refining capacity in the country. |74| Nearly half of the refineries in PADD 3 are equipped with coking units (Figure 3), a refinery process that upgrades heavy residual material from a refinery's distillation unit and converts this material into higher-value products such as naphtha and distillate. |75| Adding a coking unit to a refinery is an expensive endeavor, with estimated costs in the $1 billion+ range. Generally, the decision to add coking capacity to a refinery is based on an expectation that the refinery will be able to purchase heavier crude oils that generally sell at a discount, and can yield certain oil products that are highly valued in domestic and international markets. Approximately 60% of PADD 3 refiners are considered coking refineries (Figure 3). Investments in coking capacity were made based on an expectation that price-discounted heavy crudes from Canada and Latin America would be increasingly available.

Figure 3. Oil Refining Capacity and Coking Refinery Capacity by PADD

Click to enlargeSource: Energy Information Administration, CRS.

Notes: Numbers may not sum due to rounding. PADD 2 tight oil production is for Bakken only. PADD 3 tight oil production reflects actual and expected crude oil production in both the Eagle Ford and Permian Basin formations. Tight oil production numbers are from EIA's 2014 Annual Energy Outlook reference case scenario.Increased production--both actual and forecasted--of LTO in PADD 3, primarily from the Eagle Ford and Permian Basin tight oil formations, may cause some refiners in this region to assess their optimal economic operating parameters. Each individual refiner will likely evaluate economic conditions--crude oil prices and product values--to determine if processing additional volumes of LTO is economically justified. While it may be challenging for PADD 3 refiners to process increasing volumes of LTO based on a refinery's current configuration, investments can be made to handle additional volumes of LTO. However, LTO price discounts, product values and volume commitments, investment requirements, and economic optimization for each individual refinery will dictate the additional volume of LTO that is ultimately absorbed. Whether such investments might actually be made is beyond the scope of this report. |76|

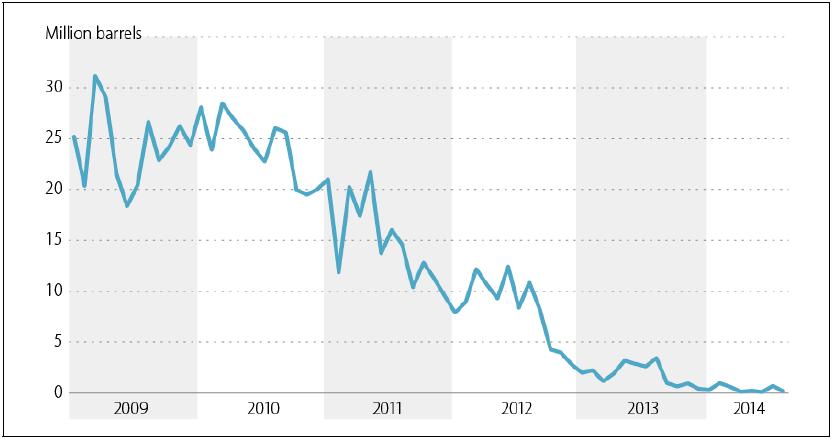

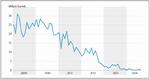

In addition to making investments in refining equipment, reducing import volumes of light sweet crude into PADD 3 is one possible avenue for absorbing more domestically produced LTO, but some refiners may have already exhausted this option. Indications are that light sweet crude imports are approaching extremely low levels and there may be limited opportunities to further reduce light sweet imports--based on current refinery configurations--if U.S. LTO production continues to increase as projected. As an example, PADD 3 light sweet imports were near zero through August 2014 (Figure 4).

Figure 4. PADD 3 Light, Sweet Crude Oil Imports

2009-August 2014

Click to enlargeSource: CRS using data from the Energy Information Administration's U.S. Crude Oil Import Tracking Tool, accessed November 21, 2014.

Additionally, some estimates project that total North American light crude oil imports may go to zero by the end of 2014. |77| Once total light crude imports are reduced to zero, refiners may begin evaluating options to reduce medium- and heavy-quality crude imports. However, foreign oil suppliers--notably Saudi Arabia and Venezuela--have ownership positions in some U.S. refinery assets. These countries could choose to continue providing oil, in some cases at discounts compared to available U.S. crudes, to their U.S. refineries in order to maintain presence in the U.S. oil market. Should countries elect this option, there may be limits to reducing crude oil imports. The ability of refiners to utilize more LTO is one consideration. However, transporting crude oil from production fields to refiners is another issue that can impact LTO price discounts and refining economics.

One consideration for U.S. oil producers is the availability and cost of transportation infrastructure to deliver crude oil to refineries. Delivery infrastructure, and the cost associated with various transportation modes, can affect the value of oil that is produced in certain locations. LTO production growth in certain parts of the country is resulting in some constraints associated with moving crude oil to refiners. |78|

Crude oil is transported via pipeline, rail, marine vessel, and truck. Pipelines are the primary means of crude oil transportation in the United States. Generally, the U.S. crude oil pipeline network was originally designed to move crude oil and petroleum products northward from the Gulf Coast to Cushing, Oklahoma, and other destinations (See Figure 5). The geographic distribution of LTO production--currently concentrated in North Dakota and Texas--is constraining the existing U.S. pipeline delivery system, thereby creating market access challenges for some oil producers.

Figure 5. Major U.S. and Canadian Crude Oil Pipelines

Click to enlargeSource: CRS using data from Platts Quarter 4, 2013 dataset. Map created on February 6, 2014.

Notes: The figure above is a simplified illustration of the U.S. crude oil pipeline network. Many small and short distance pipelines are not included.To address these challenges, the crude oil transportation network is evolving: (1) some pipelines are reversing oil flow direction, |79| (2) new pipelines are being developed, |80| (3) rail shipments are increasing to deliver LTO from North Dakota to the east and west coasts, as well as the Gulf Coast, |81| and (4) LTO waterborne shipments are also increasing. Waterborne shipments must comply with Jones Act requirements. |82| Transportation costs and constraints contribute to different oil values at various delivery points throughout the country. While infrastructure adjustments are occurring, it is unclear how much LTO volume these adjustments will ultimately accommodate. Depending on their location and the cost of transportation modes available, some oil producers may argue that allowing crude oil to be exported would serve to equalize prices by alleviating some of the infrastructure-related price discounts in the market. Infrastructure limitations and resulting price discounts will impact the volumes of oil produced as well as refiner decisions to utilize incremental LTO production.

Ultimately, the objective of U.S. oil producers is to maximize the value, or selling price, of each barrel of oil produced. U.S. oil producers throughout the country receive different prices, which can be affected by oversupply in a certain region due to production levels, refinery demand, and/or infrastructure limitations. Figure A-1 in Appendix A provides price history information for selected crude oil types. Allowing crude oil to be freely exported may have the result, all other things being equal, of reducing producer price discounts in some parts of the country, thereby equalizing the value of LTO to match global crude prices, adjusted for quality and yield characteristics and the cost of transportation. However, allowing crude oil prices to normalize may negatively impact certain refiners that are currently profitable due, in part, to regional crude oil price discounts.

For example, spot prices for Bakken LTO have experienced price discounts compared to the U.S. West Texas Intermediate (WTI) benchmark. EIA reports that Bakken discounts have been as high as $28 per barrel, but have since adjusted--a result of changes to the oil transportation network (see "Infrastructure Challenges" section above)--to lower levels as logistic constraints have been alleviated in the region. |83| Eagle Ford LTO in Texas has not experienced significant price discounts like those observed in the Bakken, likely due to its relatively closer proximity to refining customers and fewer transportation challenges. Eagle Ford condensate prices are more difficult to assess (see "Condensate" text box above). While typical U.S. price information does not include a condensate category, some refiners do post prices for various crude types, including condensate. Price postings available to CRS indicate that condensate prices, and therefore discounts to crude oil benchmarks, can vary. December 2014 condensate price postings from two different refiners indicate discounts that range between $0.75 and $12 per barrel. |84| This wide discount range suggests that specific refiners value condensate differently. As a result, certain, but not all, condensate producers may be financially impacted by condensate price discounts.

As LTO production increases, transportation bottlenecks and limited refinery demand for LTO and condensate feedstock may put downward pressure on LTO producer prices. While refining and transportation adjustments will likely occur, lower prices may result in less oil production, depending on the severity of the price discount and the economics of specific oil production projects. Furthermore, the relationship between producer prices and refinery acquisition costs is dynamic. As transportation networks and refinery configurations adjust to a changing crude oil slate, prices should reflect bottlenecks and limitations that exist. Under constraint conditions, the price discounts needed to motivate system modifications, in combination with price levels needed to incentivize incremental oil production, are uncertain and can be difficult to estimate due to the integrated and dynamic nature of production, transportation, and refining. Such estimates are beyond the scope of this report.

Debate about U.S. crude oil exports is complex, dynamic, multidimensional, and includes many different stakeholder views. As a result, there are several issues that Congress may consider during future debate about crude oil exports. The following sections discuss some of these considerations. Also, in 2014 several organizations published analytical studies that assessed the economic and price impacts of potentially removing U.S. crude oil export restrictions. Appendix B includes a table that summarizes results from four studies based on parameters that might be of interest to Congress.

According to the economic theory of international trade, opening markets to world trade tends to push the domestic price of the traded good toward the world price. Additionally, if the volume of products entering the world market is sufficiently large, the world price may also adjust to account for the new world supplies. Although the U.S. oil market has been open to world trade for many years, it has generally been in one direction. While large volumes of imported crude oil have helped to provide for the consumption of petroleum products, exports of crude oil have essentially been prohibited. The price of oil is determined on the world market, and any changes in demand and/or supply which might be expected to affect the price of oil must be set against world levels of market activity. As the United States considers whether to allow the export of domestic crude oil to the world market, price changes are likely to occur consistent with those suggested by international trade theory.

The price effects of allowing the export of crude oil from the United States to the world market are likely to be threefold. First, the domestic price of LTO, or other grades of exported oil, is likely to converge toward the world price. Second, the price of the U.S. reference crude grade-- West Texas Intermediate (WTI)--is likely to adjust relative to world reference grade crude oils, notably Brent. |85| Third, the world price of oil is likely to adjust to reflect added U.S. supplies to the world total, all else being equal. See Figure A-1 in Appendix A for price history information for selected crude oil types.

The actual magnitude of these price effects will be determined by the volume of crude exports from the United States that actually materialize. For example, should U.S. exports of LTO settle at about 500,000 barrels per day, |86| this would represent nearly one half of the total output from the Bakken field in 2013, 2.5% of total U.S. consumption, and 0.5% of world demand for oil. |87| As a result, the observed price effects on Bakken, and other price-discounted domestic crude oils might be expected to be relatively large, while the effects on U.S. reference prices and the world price of oil might well be smaller.

Shale based LTO, since its entry to the U.S. market, has sold at a discounted price relative to other domestic crude oils of similar quality. As described in this report, the location of the oil, the lack of infrastructure to move the oil to refineries, and the technological characteristics of U.S. refineries all contributed to the need of suppliers to discount the price to induce refiners to purchase available supplies. The EIA reported that since 2012 the price of Bakken crude oil has been discounted by as much as $28 per barrel compared to WTI. |88| While price discounts were less during most of the years 2012-2013, discounts were necessary to help cover the added cost of rail shipment of Bakken crude oil, which averages $10 to $15 per barrel nationwide. Rail shipment costs are as much as three times the cost of shipping oil by pipeline. |89|

Allowing the export of LTO would likely create additional demand for these crude oils that could cause the price to rise from discounted levels in the U.S. market to approach those earned by other light, sweet crudes in the world market. This would have the effect of reducing or eliminating the discount experienced in the U.S. market. Transportation infrastructure limitations would likely limit the quantities of exportable oil and add to its cost, but the potentially higher price earned by producers could help expand the industry. Investment in the fields might increase and with it oil production and related job creation.

Introduction of LTO exports might also affect the price spread between WTI and Brent crudes. This could happen as the result of two price effects. First, as domestic LTO becomes relatively less available on the domestic market, reflecting the quantities entering the world market, the price of WTI is likely to rise as the domestic market tightens. Second, the price of Brent has been especially high since the Libyan revolution, which led to reduced supplies of light, sweet crude oil to Europe. While the direction of change in both prices may be estimated based on market theory, the actual magnitude of the price change would likely depend on the quantity of U.S. crude oil exported. A reduction in the WTI-Brent price spread as a result of these factors would be favorable for oil production and producers in the United States, with somewhat higher product prices for some U.S. consumers. A reduction in the price of Brent would primarily benefit European consumers, although the benefits of lower prices could extend to the world market.

An increase in supply of LTO to the world market of, for example, 500,000 barrels per day, or 0.5% of world demand, would not be expected to have a large effect on world oil prices. A qualification to this observation is that the elasticities of both demand and supply in the world market are very low. As a result, changes in the quantities demanded or supplied on the market can have exaggerated effects on price. Among the effects of U.S. exports might be a reduced call on Organization of the Petroleum Exporting Countries (OPEC) crude oil and an increase in effective spare oil production capacity in the world market.

OPEC provides crude oil to fill the gap between world demand and the total production from all other, non-OPEC, oil producers. Nations tend to use domestic crude oil and the supplies available from close exporters before calling on OPEC producers for supply. If the call on OPEC producers is reduced, this amounts to an increase in spare capacity in the sense that supplies, if withdrawn from the market, could re-enter the market in the event of an unanticipated demand increase or a supply emergency. An increase in spare capacity might be expected to reduce the potential for price volatility in the oil market. The escalating prices of the summer of 2008 were associated with a period of high demand that strained available supply, which caused excess capacity to fall to low levels.

Changes in the prices of petroleum products directly affect consumer costs and behavior at the pump. According to EIA, 68% of the consumer's cost of gasoline and 57% of the consumer's cost of diesel fuel is directly attributable to the refiner's cost of crude oil. Therefore, changes in the price of crude oil are likely to result in proportional changes in the prices of petroleum products. This implies that the crude oil price effects analyzed in the previous section of this report will directly affect U.S. consumers.

The observed price discounts on Bakken crude largely, but not entirely, accrued to refiners supplying the Midwest and Rocky Mountain regions. A result of the availability of discounted crude oil may be that gasoline and other petroleum product prices were lower in those regions, compared to the national average. For example, during the period January 2012 through January 2014 Midwest gasoline prices were lower than national average gasoline prices during 21 of 24 months. As the price of local crude oil supplies rises to reflect convergence with the world price of oil, the benefit of these lower prices to regional consumers is likely to be reduced.

If world oil prices decline as a result of U.S. exports, this could result in somewhat lower petroleum product prices for U.S. consumers as refiners use a mixture of domestic and imported crude oils that are tied to the world price of oil. This could occur if the quantity weighted reduction in world prices more than offset the quantity weighted increase in regional domestic prices. Although a fall in world oil prices might be predicted, its magnitude may be small should the amount of U.S. crude oil exports be small relative to the world market.

By contributing to an increase in world spare capacity, U.S. exports could contribute to less volatile prices in the world oil market. Price stability, coming from less reaction to the numerous supply problems that plague the supply side of the market, could reduce market uncertainty, possibly bringing benefits to national and international energy planners.

Energy Security and Geopolitics

Although there has been some debate over U.S. crude oil exports, the effects of rising U.S. oil production have already been felt in international markets and on geopolitics. While increased oil production has allowed the United States to alter its geopolitical posture, the U.S. government has not used its oil production as leverage over other countries, and has been critical of countries that do. |90| Furthermore, the U.S. government does not directly control either oil production or the companies that produce oil.

The rise in U.S. production has decreased the need for imports, improving the U.S. trade balance, and leaving more oil and spare production capacity on the world market. It has also contributed to an increase in refined petroleum product exports, an activity not prohibited by U.S. law. The change in perspective of the United States being a major oil importer to possibly an exporter has altered the United States' place in world energy. Countries that may have viewed the United States as a declining economic power may now view it as having competitive advantages in new sectors related to petroleum. Some oil producing countries that viewed the United States as a market destination may now view it as a competitor.

If the United States changes its import/export position and potentially its rules regarding crude exports, the effects on geopolitics will differ depending upon how and when the changes occur in addition to the expected volume of exports. In the short term, as has already been raised, the United States may consider allowing more exports of crude oil to correct a possible market inefficiency due to refining capacity/configurations and crude oil specifications. In the medium term, whether U.S. laws will be changed to allow greater export of crude oil remains a key question. In the long term, if U.S. laws and regulations were changed to promote crude oil exports, how big of an exporter would the United States become remains the central question to the impact on geopolitics.

The U.S. posture toward sanctions against Iran, including by some Members of Congress, has become more stringent, in part because of the rise in U.S. oil production. |91| Additionally, the decline in U.S. imports has made the United States less reliant on certain OPEC countries, particularly countries that provide light sweet crude oil (see Figure 4), such as Nigeria. |92| OPEC, at least publicly, has "welcomed" the rise in U.S. oil production as stabilizing to the market. |93| Saudi Arabia, the world's largest crude oil exporter, has also indicated support for increased U.S. oil production as well as exports. |94| However, some analysts argue that the United States is shifting its interest (i.e., military presence) from key oil-producing regions, like the Middle East, because of its newfound resources. |95| Additionally, other industry analysts speculate that Saudi Arabia may discount its crude oil and refined product exports to the United States in order to stay in the U.S. market for strategic reasons.

U.S. consumption of petroleum products was 18.49 million barrels per day in 2012 compared to the peak rate of 20.80 million barrels per day in 2005. In 2012, the United States produced 6.49 million barrels per day of crude oil and imported 8.53 million barrels per day with the difference between consumption and production plus imports being made up of non-crude oil inputs (i.e., natural gas liquids, biofuels, refinery gain) to the refining system. In 2005, the United States produced 5.18 million bbl/d and imported 10.13 million bbl/d. Over two-thirds of imports came from Canada, Saudi Arabia, Mexico, and Venezuela in 2012 and almost 60% in 2005. |96|

Canada and Mexico are considered to be reliable suppliers. Saudi Arabia and Venezuela, both OPEC members, own extensive refining assets in the United States (Motiva and Citgo refineries respectively) and as a result might be expected to desire to maintain a presence in U.S. oil markets. Beyond these 4 countries, over 30 other countries supply the United States with crude oil, none at levels expected to be difficult to replace if emergency conditions might develop.

Should the United States remove barriers to crude oil exports, the amount of exports may not matter as much as the psychological impact. The view that the United States is committed to the global energy market may have the greatest effect. Even in the long run, most industry analysts do not project that the United States will produce more crude oil than it consumes (see Figure 1). Nevertheless, any additional barrels that the United States produces will dilute OPEC's market share, assuming demand stays the same, and this may be viewed positively by most oil-consuming countries. |97| Some countries have directly expressed interest in the United States removing crude oil and condensate export restrictions. For a brief overview of South Korea's interest, see the text box below titled "Global Interest in U.S. Crude Oil and Condensate."

U.S. oil production is rising and is projected to rise, at least, through the beginning of the next decade. If the EIA reference case projections turn out correctly, the United States would likely eventually resume its role as a growing importer of oil, assuming no other market changes. Changing geopolitical relationships because of the current situation may prove short lived if oil production does not continue to increase. Despite having a cartel supplier trying to manipulate prices, the oil market remains robust and competitive. |98| Being a part of this market has helped many countries, both producers and consumers. As an example, when the United States needed petroleum products after Hurricanes Katrina and Rita in 2005, European countries were able to supply them from their strategic reserves. Similarly, when Japan shuttered its nuclear reactors after the Fukushima tragedy in 2011, the energy market reacted by sending more natural gas, coal, and oil resources to the country in order to satisfy energy demands. Unlike earlier periods, the United States is now a participant in energy agreements through the International Energy Agency to share the burden of supply disruptions on the world market. As part of its IEA membership, the United States maintains a Strategic Petroleum Reserve that can offset disruptions in imported supplies.

Global Interest in U.S. Crude Oil and Condensate: South Korea Increased U.S. crude oil and condensate supply--especially price discounts for crude and condensate in some U.S. regions--has motivated several countries to call for ending U.S. crude oil export restrictions. South Korea has been vocal about its interest in purchasing U.S. crude oil and condensate. In August 2014, South Korean President Park Geun-hye expressed to U.S. lawmakers that getting access to U.S. condensate is a priority. |99| In particular, South Korean refiners and petrochemical companies could potentially benefit financially from access to U.S. condensate.

South Korean companies have increased condensate processing capacity, and the country is approaching nearly 350,000 barrels/day of dedicated condensate splitter capacity. Historically, condensate splitter economics were profitable due to demand for heavy naphtha and ultimately petrochemical products in combination with condensate prices, which typically sold at a discount to the Dubai crude oil benchmark price. However, market conditions changed, and during the summer and fall of 2014 condensate sold at a premium to Dubai, thereby eroding the economics of condensate splitters. South Korean companies are dependent on very few suppliers--primarily Qatar-- which have significant bargaining and pricing power.

Compared to some reported U.S. prices, South Korean refiners have paid approximately $20 per barrel of condensate more than U.S. refiners in some regions. |100| This large price spread represents a potential opportunity for South Korean buyers (i.e., lower price paid) and U.S. oil producers (i.e., higher value received), even when factoring in transportation costs. Additionally, by sourcing condensate from an alternative and potentially lower cost supplier, South Korea could use this as leverage to encourage Qatar to lower its condensate price. Ultimately, these outcomes would improve the economics and profitability of South Korean refiners and petrochemical companies.

Market conditions in December 2014 changed again with Qatar condensate selling at a discount to Dubai. As a result, South Korean refiners and petrochemical companies may not benefit much from accessing U.S. condensate in this price environment. However, over the long term access to U.S. condensate may be beneficial as an alternative source of supply should condensate markets and prices revert back to a premium over Dubai.

The potential exportation of U.S. crude oil may have implications for U.S. trade policy. The United States has undertaken certain obligations as a member of the World Trade Organization (WTO) and is a signatory to several regional and bilateral free trade agreements (FTAs).

As noted above, the United States licenses the export of crude oil under certain restrictive circumstances. The WTO generally discourages limitations on international trade such as import or export restraints. Underlying the WTO agreements are two basic principles: most-favored-nation (MFN) treatment and national treatment. MFN obligates a WTO member not to discriminate among the products of other member states. National treatment obligates a member not to treat another member's products as different from one's own. The General Agreement on Tariffs and Trade (GATT) Article XI, General Prohibition Against Quantitative Restraints, states:

No prohibition or restrictions other than duties, taxes or other charges made effective through quotas, import or export licenses or other measures, shall be instituted or maintained by any contracting party on the importation of any product of the territory of any other contracting party or on the exportation or sale for export of any product destined for the territory of any other contracting party.

However, some exceptions are available. Article XX provides a generalized exception that allows governments to restrict trade based on the conservation of exhaustible natural resources or the necessity to protect human health. However, these exceptions are subject to the provision that the objectives are not used as a disguised restriction on international trade or to arbitrarily discriminate between countries where the same conditions prevail. In this case, for example, restricting the export of crude oil may be dependent on a member's restriction of its own production.

The crude oil restriction may also be subject to the WTO's Agreement on Subsidies and Countervailing Measures (ASCM) if it, by limiting demand, drives down the price, thereby conferring a subsidy for domestic industry. This was one facet of a successful U.S. challenge to Chinese raw materials and rare earth export restrictions.

The United States is in negotiations on two multi-nation free trade agreements (FTAs): the TransPacific Partnership (TPP) and the Transatlantic Trade and Investment Partnership (T-TIP). TPP includes Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, and Vietnam. T-TIP is a proposed agreement between the United States and the European Union (EU). Countries in both of these negotiations may be interested in obtaining access to U.S. energy supplies. Both these agreements are directly relevant to exports of U.S. liquefied natural gas; according to statute it is in the national interest to approve LNG exports to FTA countries.

There is no such exception for exports of crude oil; however, the EU has sought to put access to U.S. energy--including crude oil--on the T-TIP negotiating agenda. The EU has sought a comprehensive energy chapter in the T-TIP that would guarantee access to U.S. energy supplies, which, according to a EU "non-paper," would include, "a legally binding commitment in the T-TIP guaranteeing the free export of crude oil and gas resources by transforming any mandatory and non-automatic export licensing procedure into a process by which licenses for exports to the EU are granted automatically and expeditiously." |101| The United States reportedly has resisted EU attempts to include energy as a separate chapter, but to consider energy in terms of other goods trade in the agreement. |102| On September 29, 2014, Senators Boxer and Markey wrote to U.S. Trade Representative Michael Froman contending that "automatic and unrestricted approval of U.S. oil and gas exports to the EU has the potential to harm consumers, our national security, and our environment" and urged him to oppose such provisions in T-TIP. |103| EU attempts to lock in energy guarantees through T-TIP may take on increased urgency as a result of renewed tensions with Russia, a major oil and gas supplier to Europe.

Potential environmental issues that could arise from the removal of crude oil export restrictions are dependent on the specific consequences that might ensue from removing such restrictions. However, these consequences, particularly the long-term effects, are uncertain.

A primary question for policy makers is the net effect on domestic oil production from removing the export restriction. As illustrated in Figure 2, EIA projects domestic production of LTO to increase dramatically in the near future. However, some observers have argued that the export restriction, coupled with current refinery configurations (discussed above), will effectively create a production ceiling for specific resources. |104| Assuming this is the case, the next question concerns magnitude: How much additional domestic production would occur if the crude oil export restriction is removed? Estimates for expected U.S. crude oil export volumes are uncertain and actual volumes will depend on multiple variables. As noted above in the "Price Effects" section, some estimate a potential excess of 500,000 bbl/d of light sweet crude oil by the 2015 to 2016 time frame.

Assuming that lifting or modifying export restrictions would result in a substantial increase in domestic crude oil production--above what would otherwise occur--several environmental issues would likely receive some attention. These issues, discussed below, may include oil transportation, impacts related to oil extraction, and climate change.

A further increase in domestic crude oil production could amplify existing oil transportation concerns, which have received considerable attention. In particular, the current expansion of North American oil production has led to significant challenges in transporting crudes efficiently and safely using the nation's legacy pipeline infrastructure. In the face of continued uncertainty about the prospects for additional pipeline capacity, and as a quicker, more flexible alternative to new pipeline projects, crude oil producers are increasingly turning to rail as a means of transporting crude supplies to U.S. markets. According to EIA data, the volume of crude oil carried by rail increased 20-fold between 2008 and 2013. |105|

While oil by rail has demonstrated benefits with respect to the efficient movement of oil from producing regions to market hubs, it has also raised significant concerns about transportation safety and potential impacts to the environment. The most recent data available indicate that railroads consistently spill less crude oil per ton-mile transported than other modes of land transportation. |106| Nonetheless, safety and environmental concerns have been underscored by a series of major accidents across North America involving crude oil transportation by rail. |107|