| Information |  | |

Derechos | Equipo Nizkor

| ||

| Information | | |

Derechos | Equipo Nizkor

| ||

Aug13

IMF Country Report - Spain 2013 Article IV Consultation

IMF Country Report No. 13/244

Under Article IV of the IMF's Articles of Agreement, the IMF holds bilateral discussions with members, usually every year. In the context of the 2013 Article IV consultation with Spain, the following documents have been released and are included in this package:

- Staff Report for the 2013 Article IV consultation, prepared by a staff team of the IMF, following discussions that ended on June 19, 2013, with the officials of Spain on economic developments and policies. Based on information available at the time of these discussions, the staff report was completed on July 11, 2013. The views expressed in the staff report are those of the staff team and do not necessarily reflect the views of the Executive Board of the IMF.

- Informational Annex prepared by the IMF.

- Press Release on the Executive Board Discussion.

- Statement by the Executive Director for Spain.

STAFF REPORT FOR THE 2013 ARTICLE IV CONSULTATION

July 11, 2013

KEY ISSUES

Context. Strong reform progress is helping stabilize the economy and external and fiscal imbalances are correcting rapidly. But unemployment remains unacceptably high and the outlook difficult. This calls for urgent action to generate jobs and growth.

Policies. The reform effort needs to be raised to the level of the challenge.

- Despite reforms, labor market rigidities continue to force the adjustment onto employment. The reform needs to go further: increasing firms' internal flexibility, reducing duality, and enhancing employment opportunities for the unemployed. A social agreement could bring forward the employment gains from structural reforms.

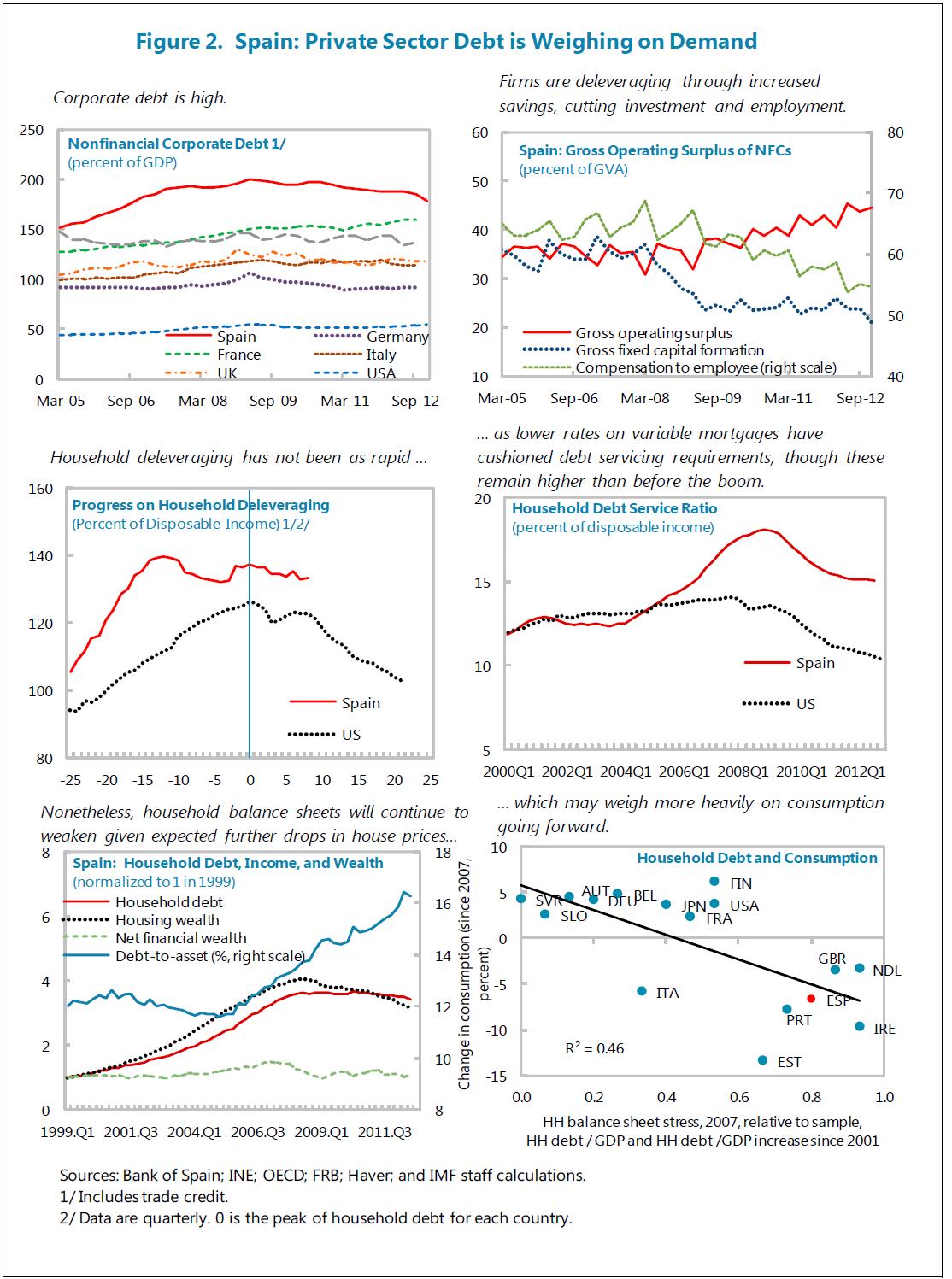

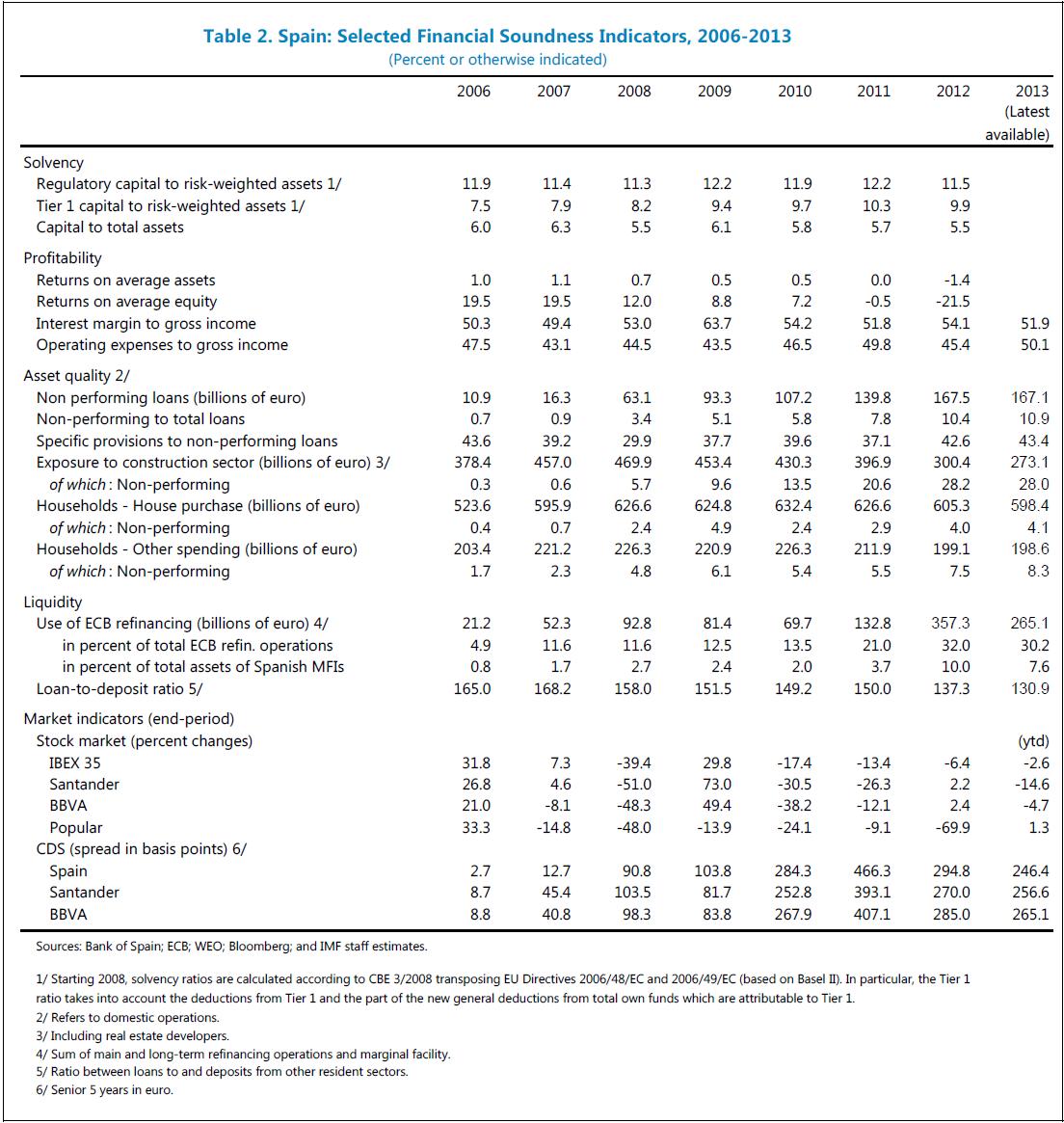

- Private sector deleveraging is weighing on growth. The insolvency regime should be further improved to provide incentives for accelerating debt workouts and cleaning up corporate balance sheets.

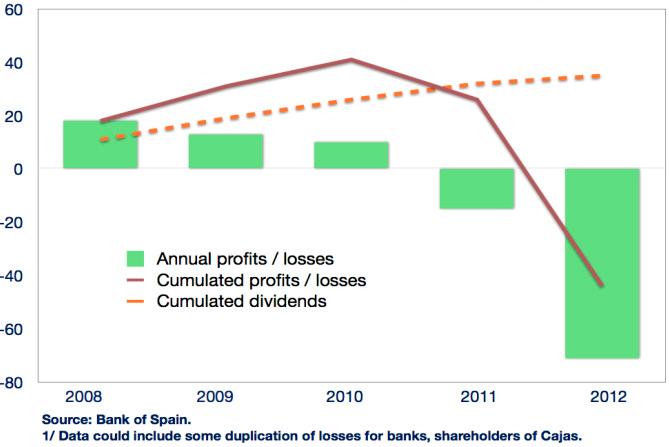

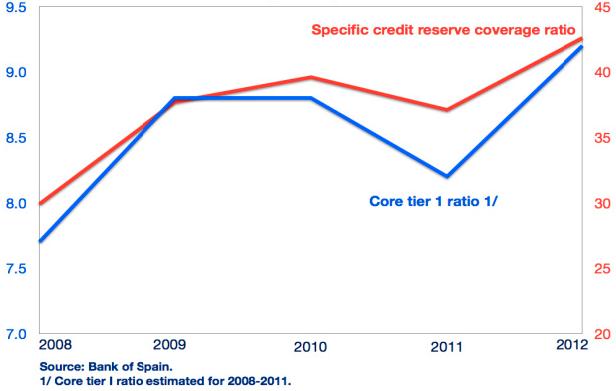

- The banking system is stronger, but risks remain elevated. This calls for continuing to reinforce capital, cleaning up loan books (encouraging banks to dispose of assets and to use the proceeds to lend), and removing credit supply constraints.

- The fiscal deficit is falling but remains too high. Consolidation should continue, but be as gradual and growth friendly as possible. Nominal, and if necessary, structural, targets should be flexible in the event growth disappoints.

- The inflation gap with the euro area has not narrowed significantly. Competition should be improved.

- European policies have helped, but--crucially--monetary policy is not feeding through. Europe should move faster to full banking union and the ECB implement further measures to reduce the much higher borrowing costs of Spain's private sector.

Approved by Ranjit Teja and Martin Mühleisen

A Staff team comprising J. Daniel (Head), K. Fletcher, P. Lopez Murphy, P. Medas, P. Sodsriwiboon (all EUR), A. Buffa di Perrero (MCM), M. Chivakul (SPR), R. Romeu (FAD), R. Espinoza (RES), K. Christopherson Puh (LEG) visited Madrid on June 6-19, 2013 to conduct the 2013 Article IV Consultation discussions. The mission also visited Barcelona, Sevilla, and Valencia. R. Teja (EUR) and A. Gaviria (COM) joined for the concluding meetings. Mr. Varela and Ms. Navarro from the Executive Director's office attended the discussions. S. Chinta and C. Cheptea supported the mission from Headquarters. The mission met with Economy and Competitiveness Minister De Guindos, Finance and Public Administration Minister Montoro, Bank of Spain Governor Linde, other senior officials, and financial, industry, academic, parliament, and union representatives.

CONTENTS

CONTEXT: REBALANCING AFTER THE BOOM-BUST

OUTLOOK: A LONG AND DIFFICULT ADJUSTMENT

THE POLICY IMPERATIVE: JOBS AND GROWTH

A. Labor: Reinforcing the Reform to Generate Jobs

B. Helping the Private Sector Delever

C. Financial: Supporting Credit While Safeguarding Financial Stability

D. Fiscal Consolidation: Minimizing the Inevitable Drag

E. Structural: Building a World-Class Business Environment

F. Pan-European SupportBOX

FIGURES

1. Recent Economic Developments

2. Private Sector Debt is Weighing on Demand

3. Economic Activity

4. Competitiveness

5. Imbalances and Adjustment

6. Financial Market Indicators

7. Labor Markets

8. Credit Conditions

9. Households' Financial Positions

10. Nonfinancial Corporates' Financial Positions

11. Balance of PaymentsTABLES

1. Main Economic Indicators

2. Selected Financial Soundness Indicators, 2006-13

3. General Government Operations

4. General Government Balance Sheet

5. Balance of Payments

6. International Investment Position, 2006-12APPENDIXES

Appendix I. Debt Sustainability Analysis

CONTEXT: REBALANCING AFTER THE BOOM-BUST

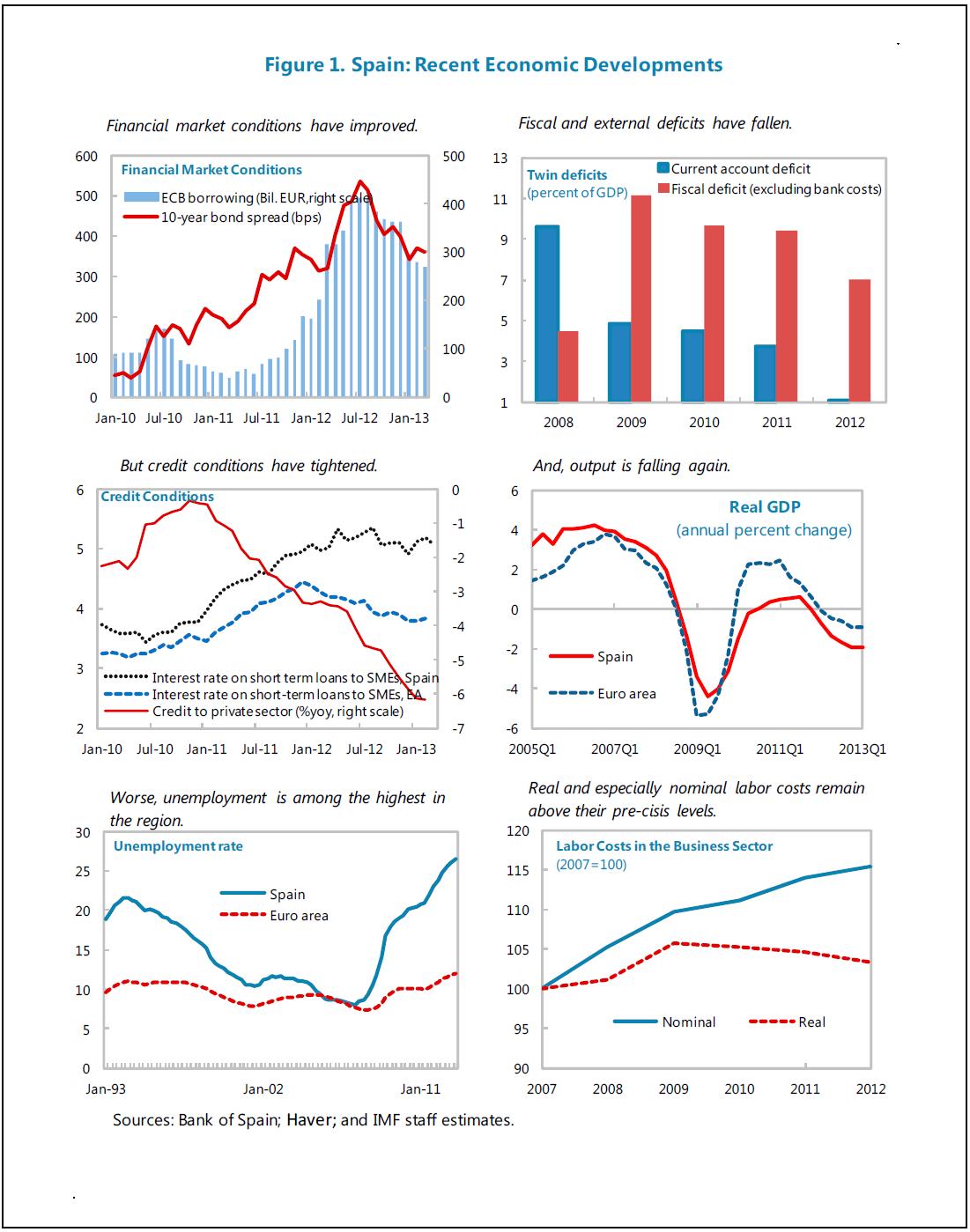

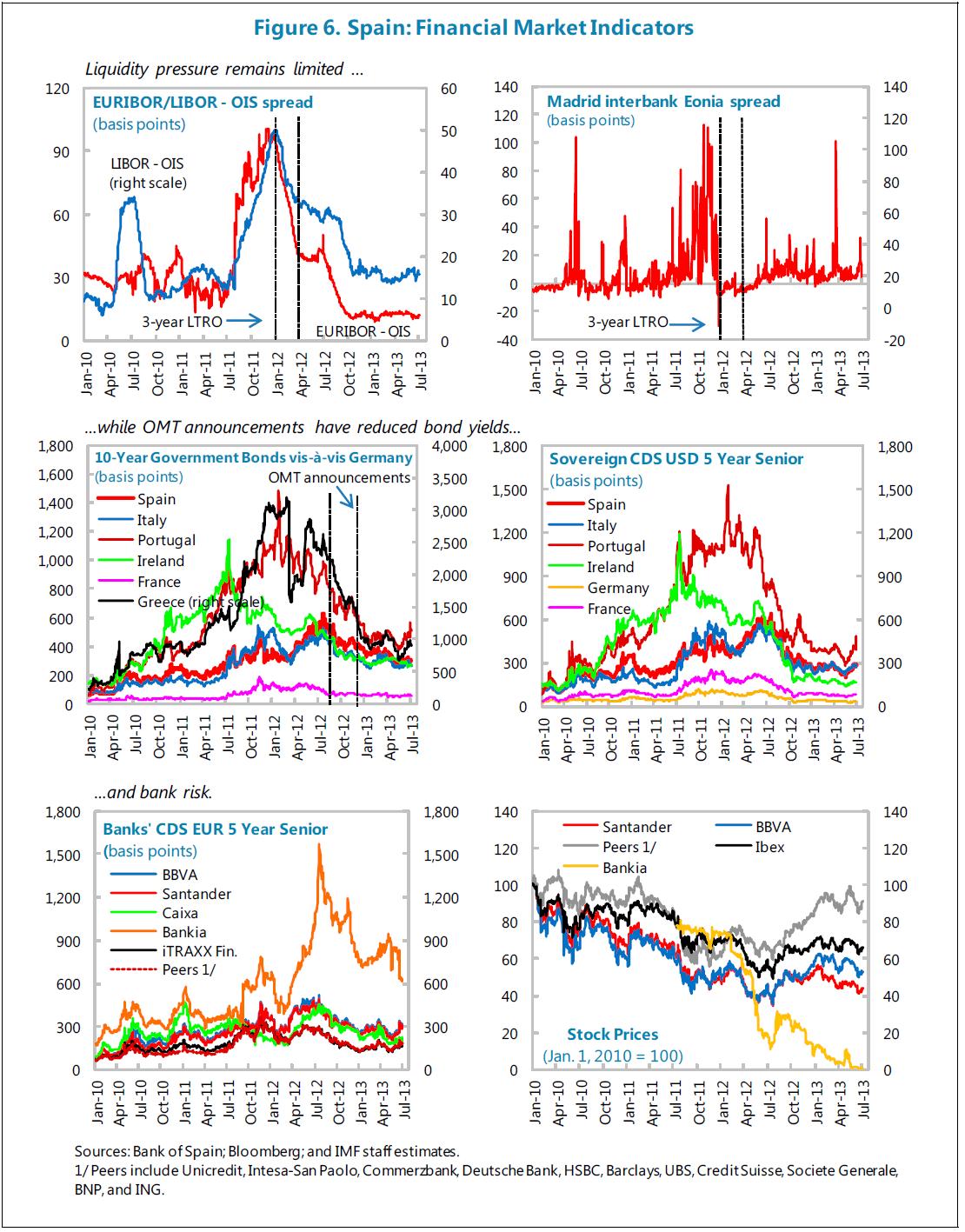

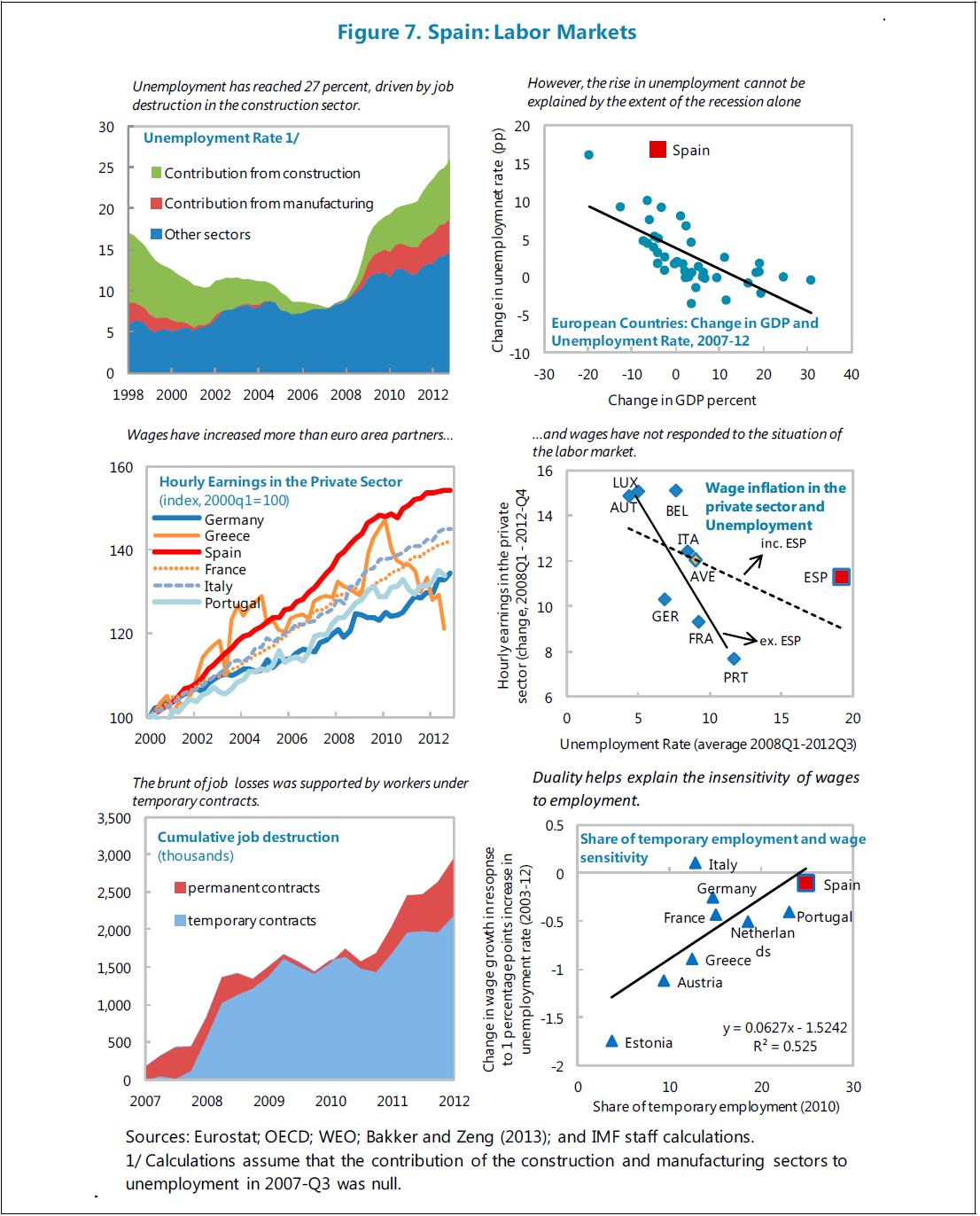

1. The Spanish economy accumulated large imbalances during the long boom that ended with the global financial crisis. After a brief stabilization in 2010, the economy fell back into recession in mid-2011 as the euro area crisis spread to Spain and Italy. Unemployment soared, more than tripling in five years to 27 percent. The fiscal position deteriorated sharply. Funding conditions tightened for both the public and private sectors, culminating in Spain's 10-year sovereign yields hitting 7V2 percent in summer 2012 and banks borrowing some 40 percent of GDP from the ECB.

2. More recently, however, there have been a number of positive developments. Most importantly:

Imbalances are correcting

- Sovereign yields have fallen sharply since the OMT announcements and the second Greek program in H2 2012 (although there is a risk that the increase in recent weeks could herald a return to higher yield environment). Financial conditions also eased for banks, allowing them to reduce their reliance on the ECB.

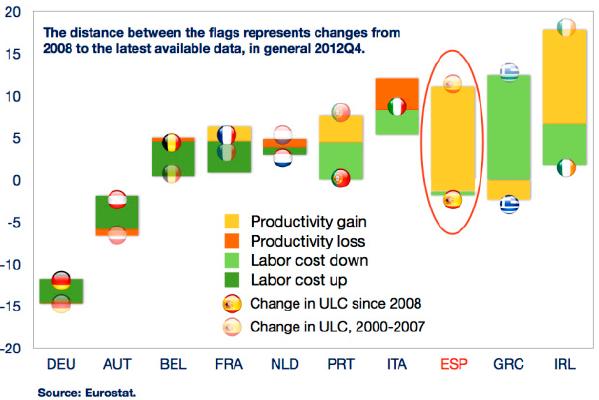

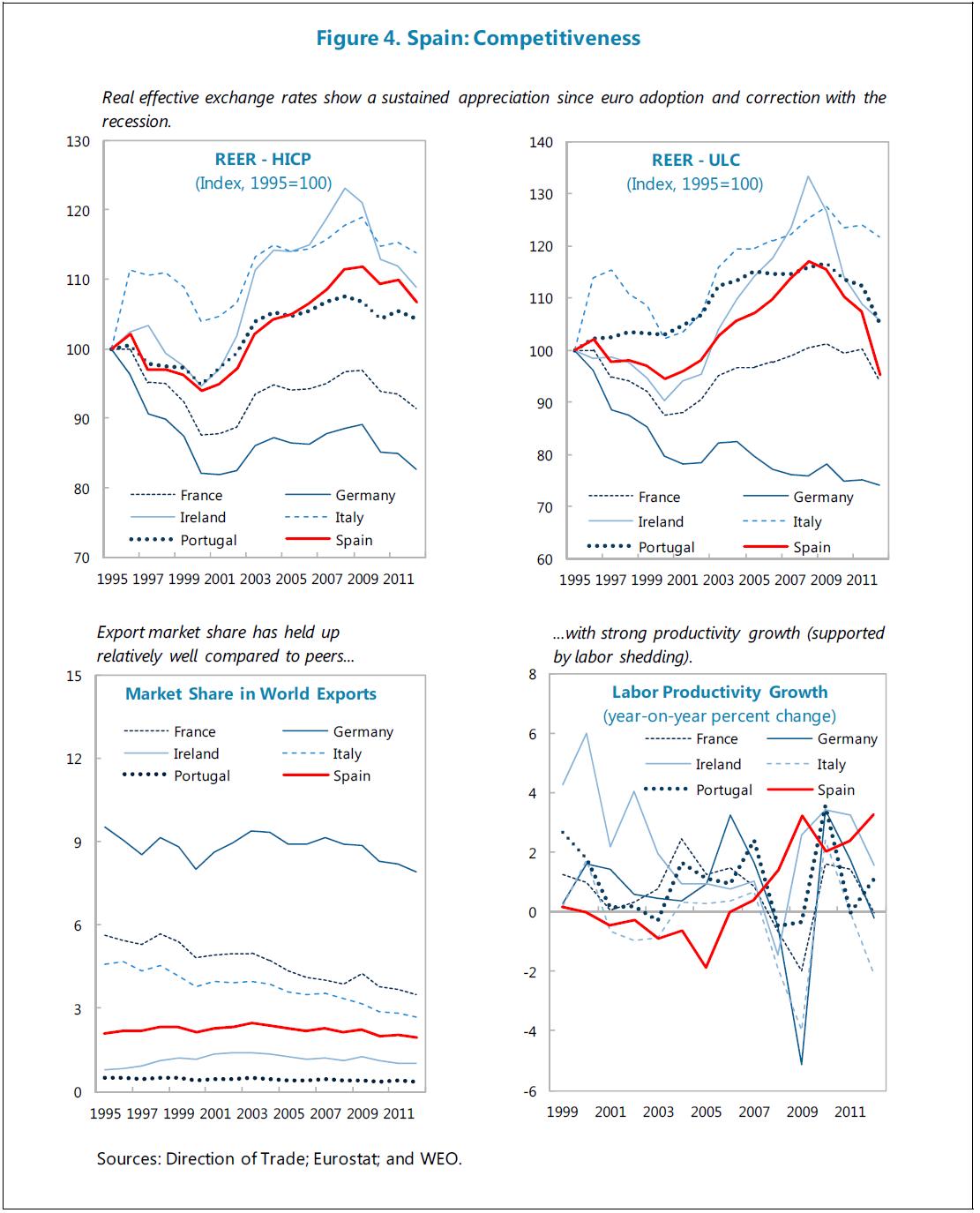

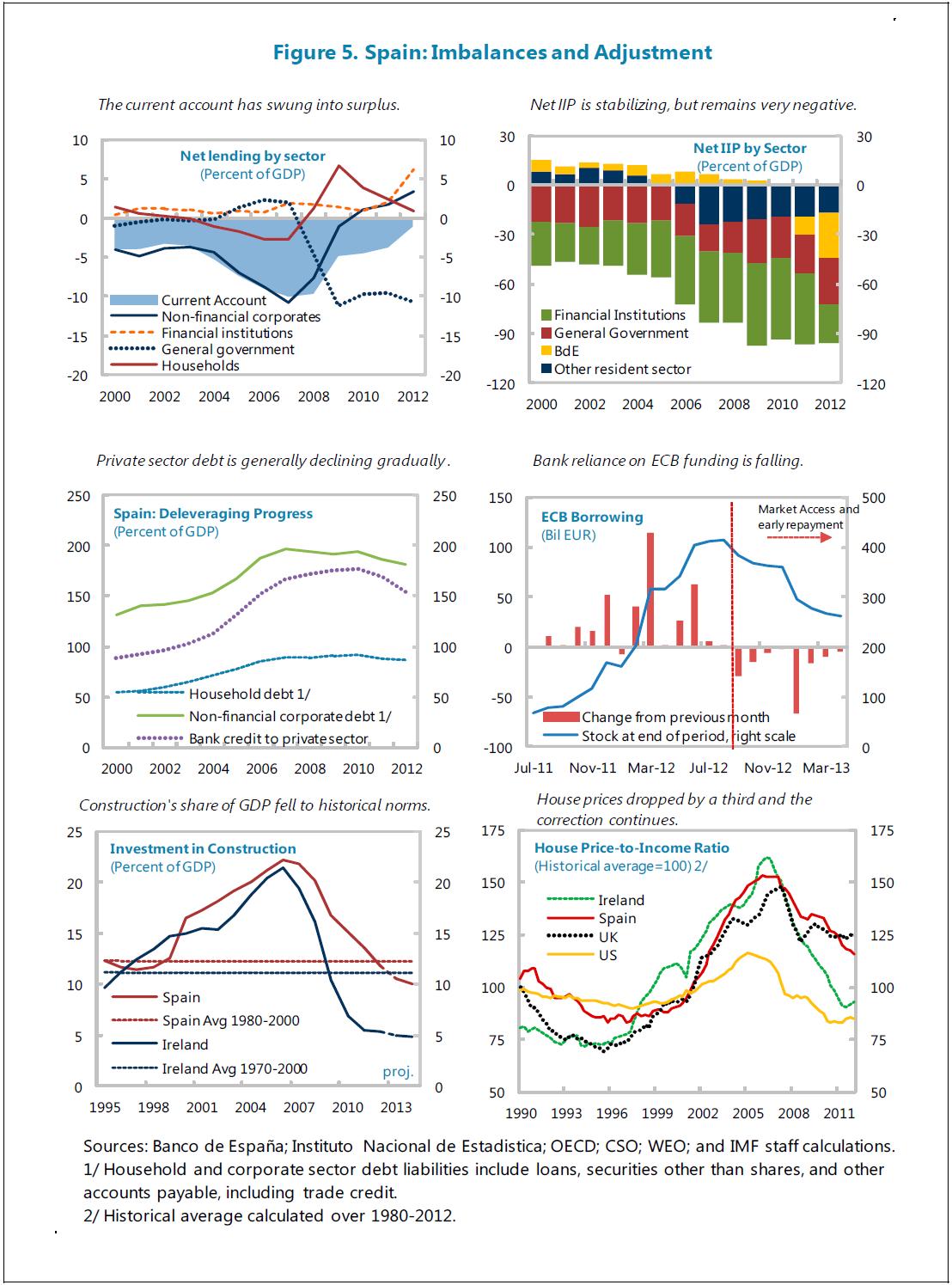

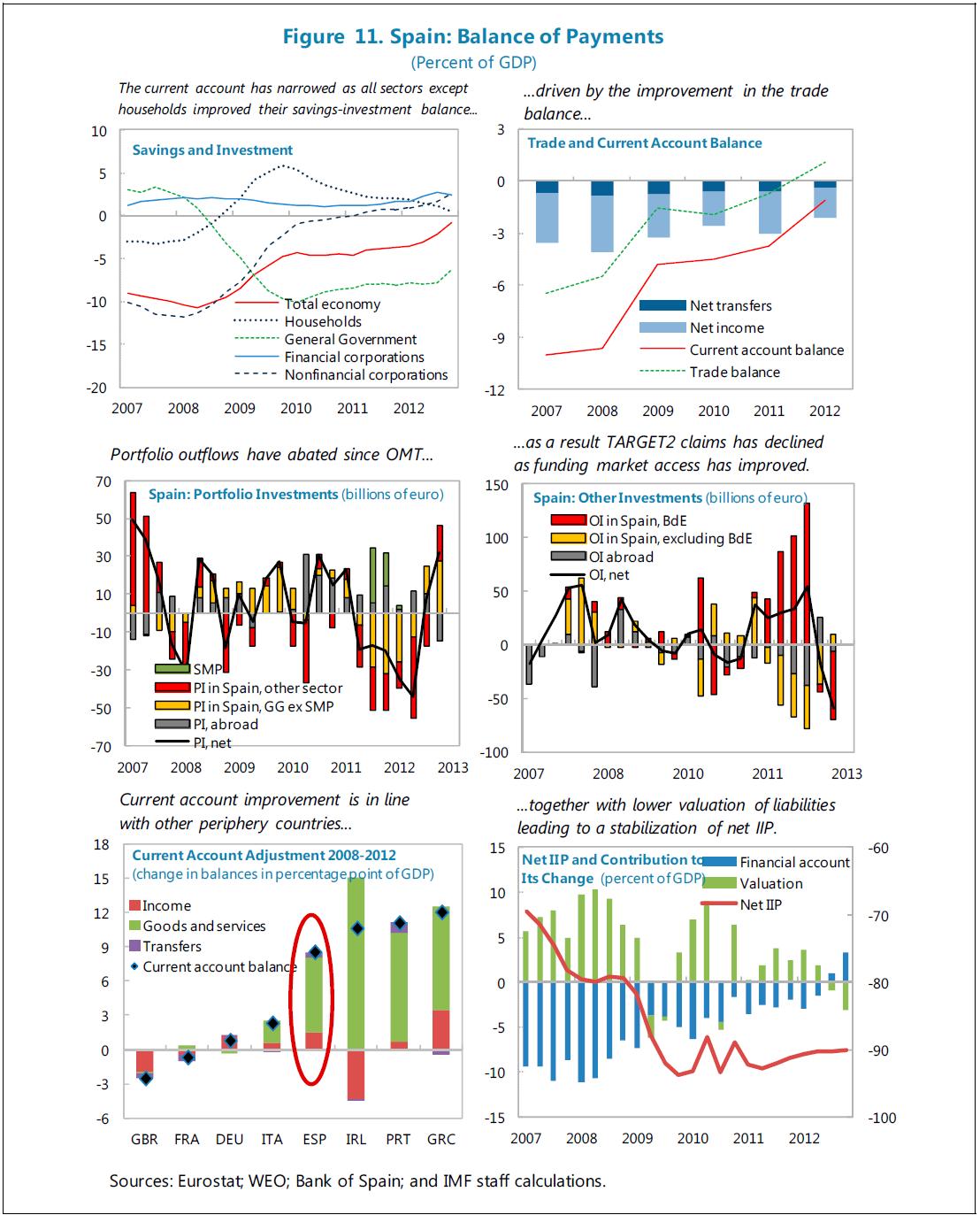

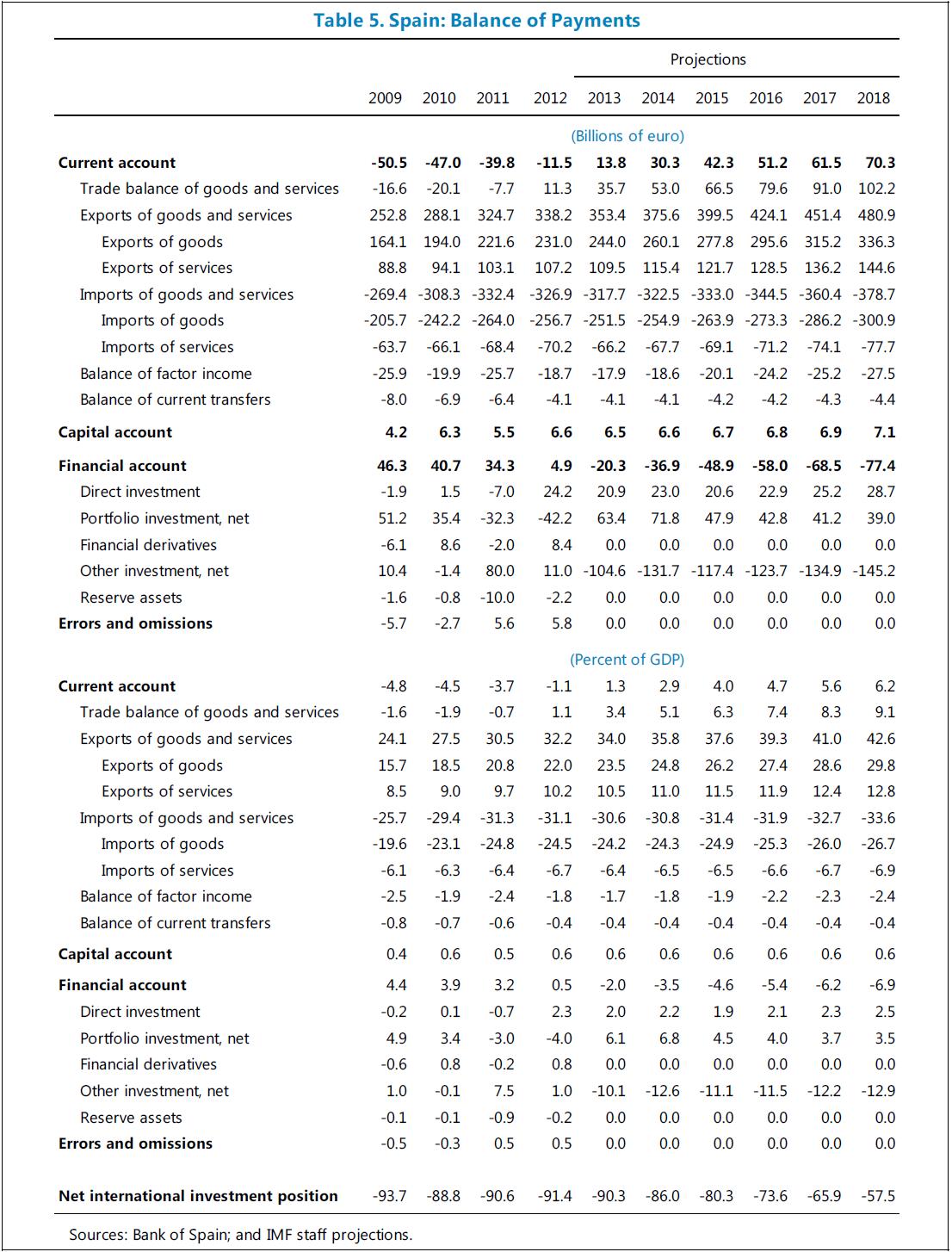

- The current account swung rapidly into surplus as exports recovered strongly (among the fastest in the euro area) and weak domestic demand restrained imports, stabilizing the IIP. Price competitiveness indicators are improving, especially unit labor costs (see background note).

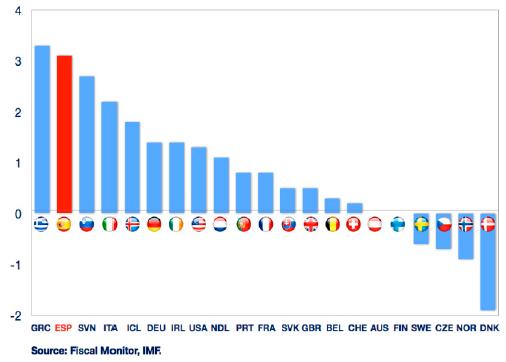

Chart 1. Change in Cyclically Adjusted Primary Balance, 2012

(percent of GDP)

- House prices are falling fast and are down a third from their peak (but are still likely some 15 percent overvalued). Construction employment is half of its peak. Private sector debt is declining.

- The fiscal deficit (excluding financial sector costs) fell sharply from 9 percent of GDP in 2011 to 7 percent in 2012, despite the interest bill increasing and the recession. The cyclically-adjusted primary balance improved by 3 percent of GDP. And in contrast to 2011, the deficit of regional governments fell sharply in 2012, with all regions reducing their deficits, some very substantially.

- Underlying inflation and wage pressures eased. Inflation at constant taxes fell 0.3 percent in May (though headline inflation remained around 1V percent). Wages in the business sector fell 0.3 percent in Q1.

Figure 1. Spain: Recent Economic Developments

The reform process has accelerated and deepened

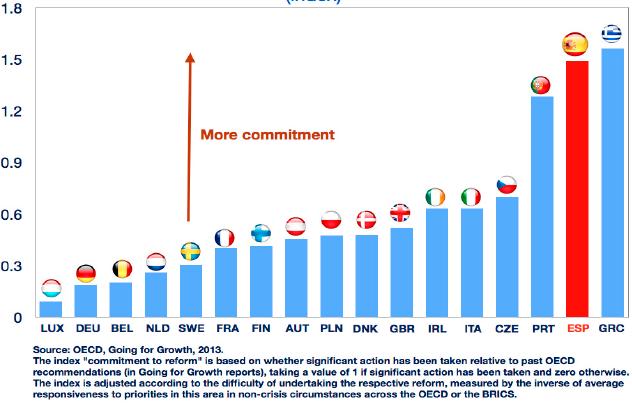

Chart 2. Commitment to Reform, Adjusted for Difficulty

(index)

- The authorities have made substantial progress in structural reforms in recent years, in line with staff advice, especially to strengthen the financial sector, improve the functioning of the labor market, and upgrade the fiscal framework. Ongoing efforts, especially to establish a fiscal council, ensure the sustainability of the pension system, and enhance competition in domestic markets, are also in line with past staff advice.

- Decisive action has been taken to help clean up banks in the context of a €100 billion (10 percent of GDP) financial sector program from the ESM, and for which the Fund is providing technical assistance. Provisions and capital were greatly increased following an independent stress test and asset quality review in summer 2012, using €41 billion of the ESM facility. Weak banks are being restructured and much of their real estate assets have been transferred to an asset management company (SAREB). Regulation and supervision was also enhanced.

- A major labor market reform was instituted in February 2012 to improve firms' ability to adjust working conditions (including wages), reduce duality, and promote job matching and training. Unemployment insurance was reduced by 17 percent after 6 months of benefits, and hiring subsidies were reformed. In February 2013, the government announced more flexible hiring arrangements and tax incentives to support youth employment and entrepreneurship.

- Product and service market reforms are underway. The government liberalized the establishment of small retail stores and retail business hours. Further reforms have been announced, in particular, to remove regulations that fragment the domestic market, to liberalize professional services, and to foster entrepreneurship.

Chart 3. Structure of Two Recessions

(cumulative percentage change)

- Fiscal frameworks and transparency have been substantially upgraded. An independent council is being introduced and a commission of experts has issued a proposal to ensure pension system sustainability. Early and partial retirement rules were further tightened. Monthly reports are now available for all major levels of government. A commission is reviewing public administration functions to eliminate overlaps/increase efficiency.

But the adjustment process is proving slow and difficult

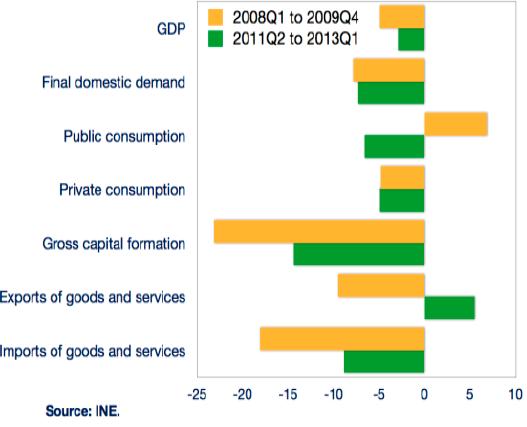

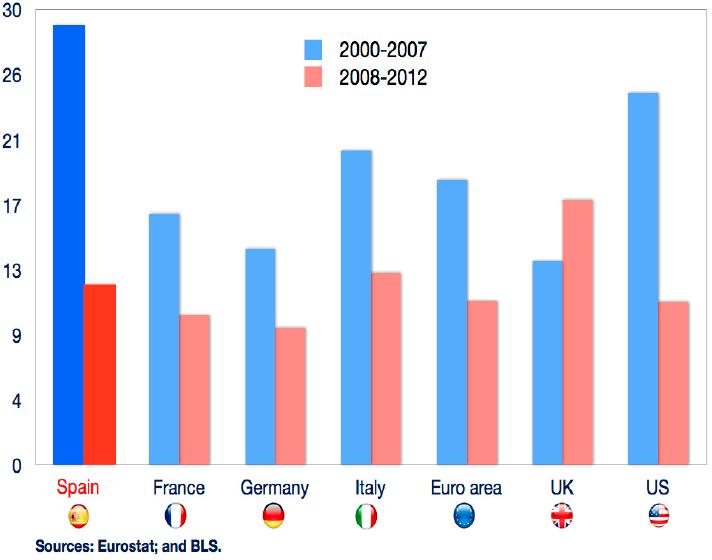

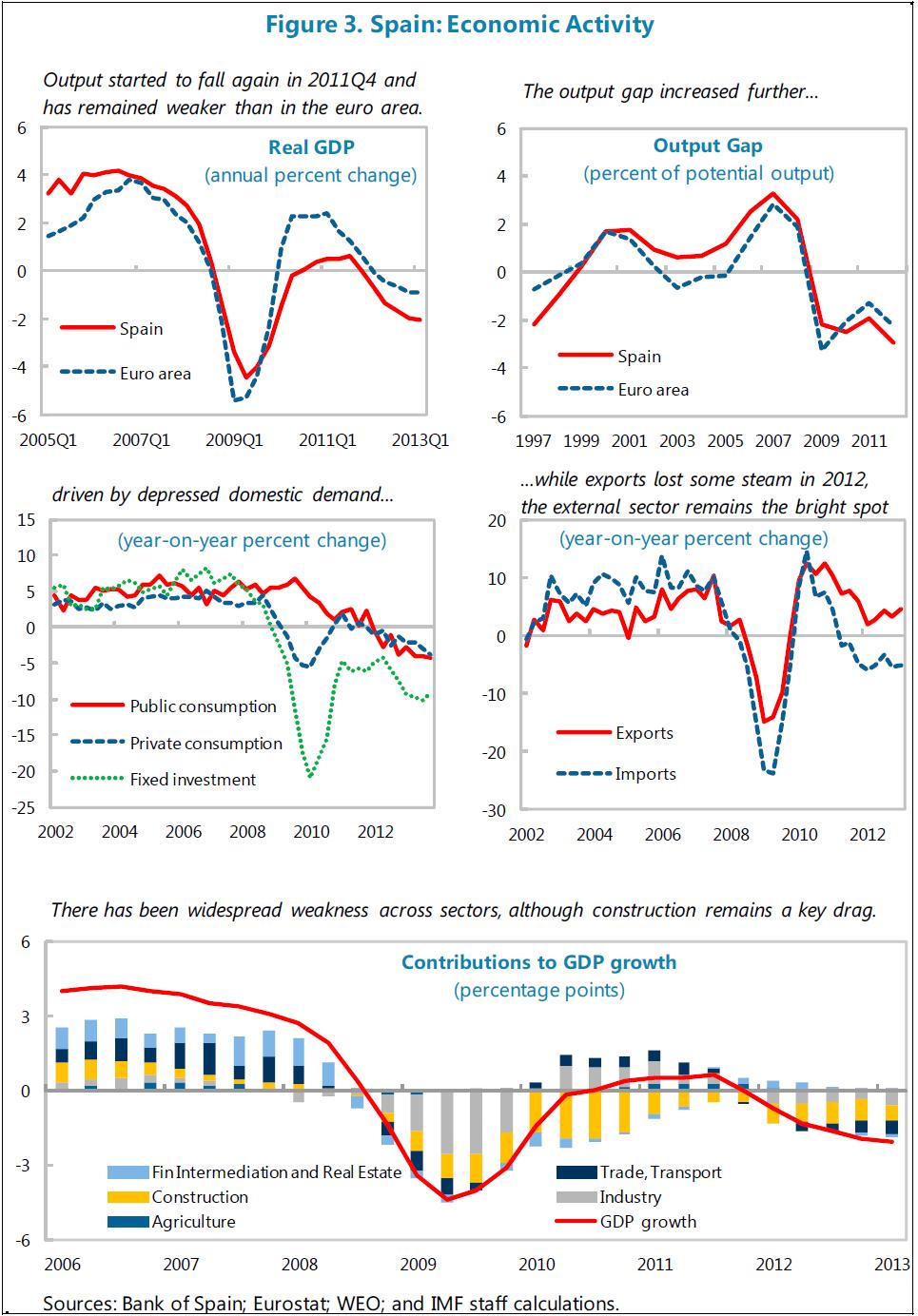

- Growth has been negative in the last seven quarters, and output is down 7 percent from its peak. Unlike the first dip of the recession, the second is proving shallower, but longer. It is also marked by fiscal consolidation rather than stimulus, but has benefited from stronger net trade and less sharp investment contraction.

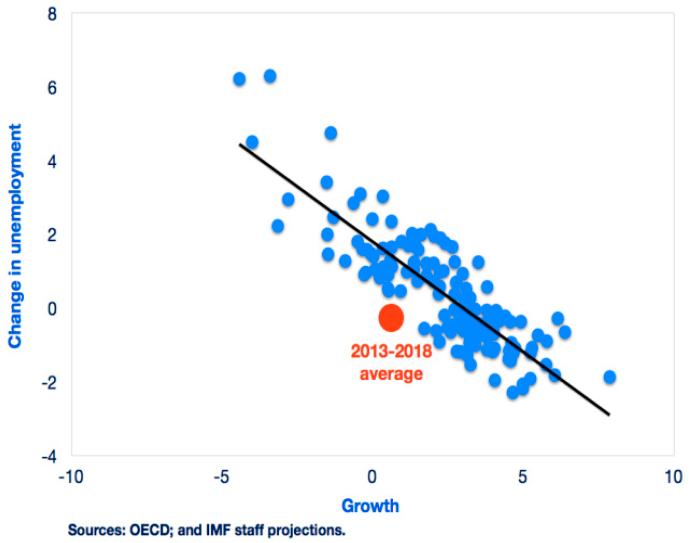

- Unemployment increased further to 27% percent in Q1. The increase since 2007 (19 points in 6 years) is unprecedented in Spain's history and the sensitivity of unemployment to growth in 2012 was one of the highest in the world. Unemployment is disproportionately affecting workers with temporary contracts and the young (57 percent unemployed in Q1 2013), reflecting Spain's highly dual labor market.

- Immigration has reversed, as both foreigners and nationals leave due to poor job prospects.

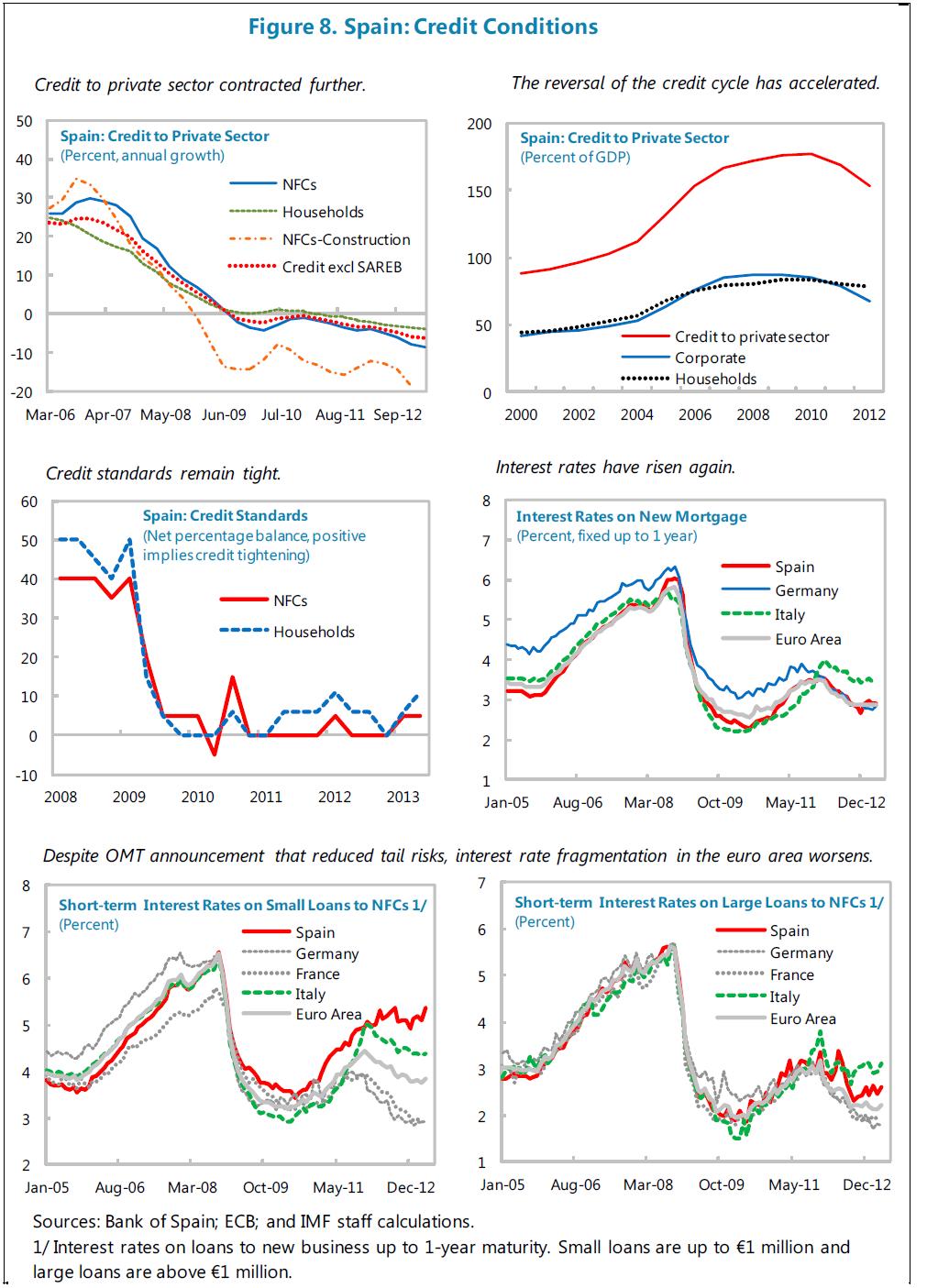

- Despite the fall in sovereign spreads, financing conditions remain tight, especially for smaller firms. Credit is falling at about 7 percent annually (9 percent for firms), lending rates on small loans are much higher than in core euro area countries and many banks have either no wholesale market access or only at high cost. NPLs continue to rise, reaching 10˝ percent in March.

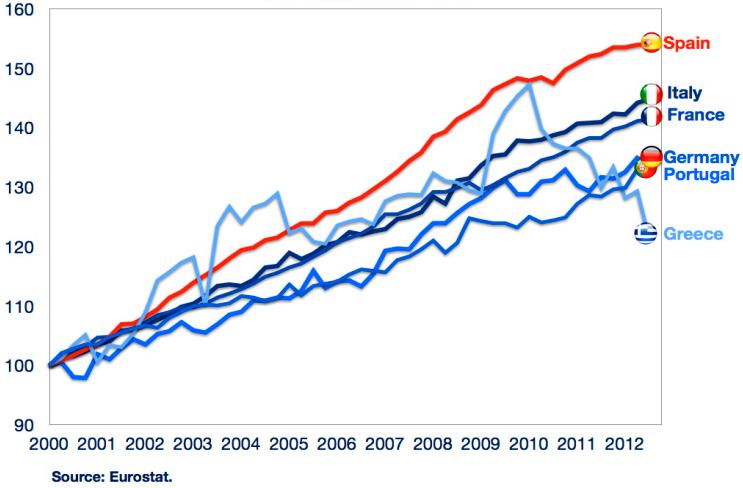

Chart 4. ULC Total Economy Growth

Relative to EA 17, since 2008

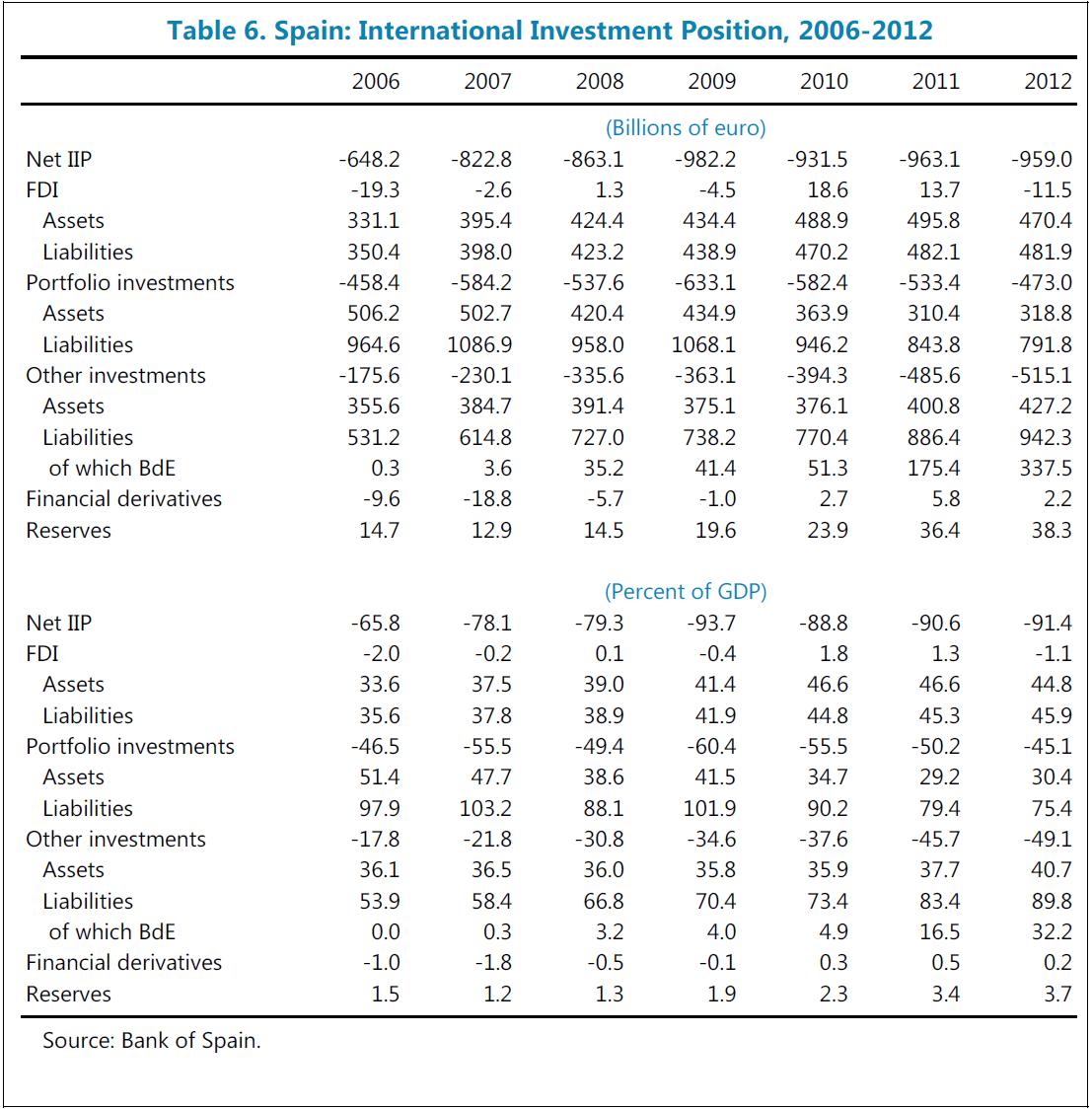

- Gains in unit labor costs reflect labor shedding (the marginal worker is typically less productive), but wage moderation too is starting to play a greater role. Although the net IIP has stabilized, the level (minus 93 percent of GDP) remains among the weakest in the euro area. Reducing unemployment while avoiding external imbalances reopening would require a significantly weaker real exchange rate. While estimates of current account norms do not suggest a significant current account gap, model-based REER analysis, as well as the overriding need to sharply improve the net IIP position, suggest an overvaluation of 8-12 percent (see background note).

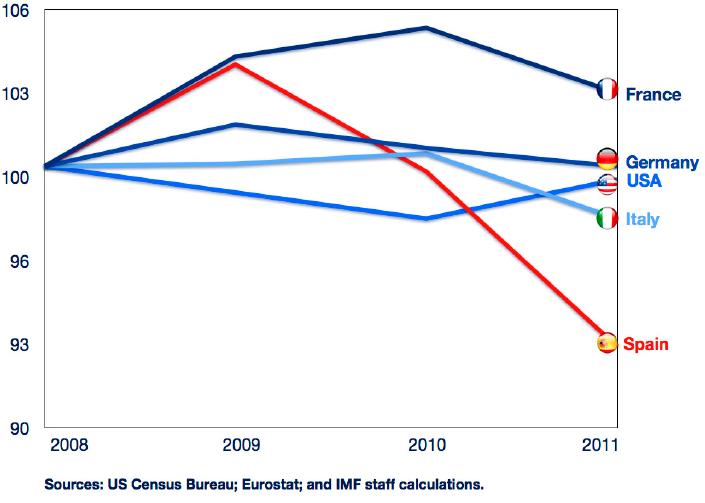

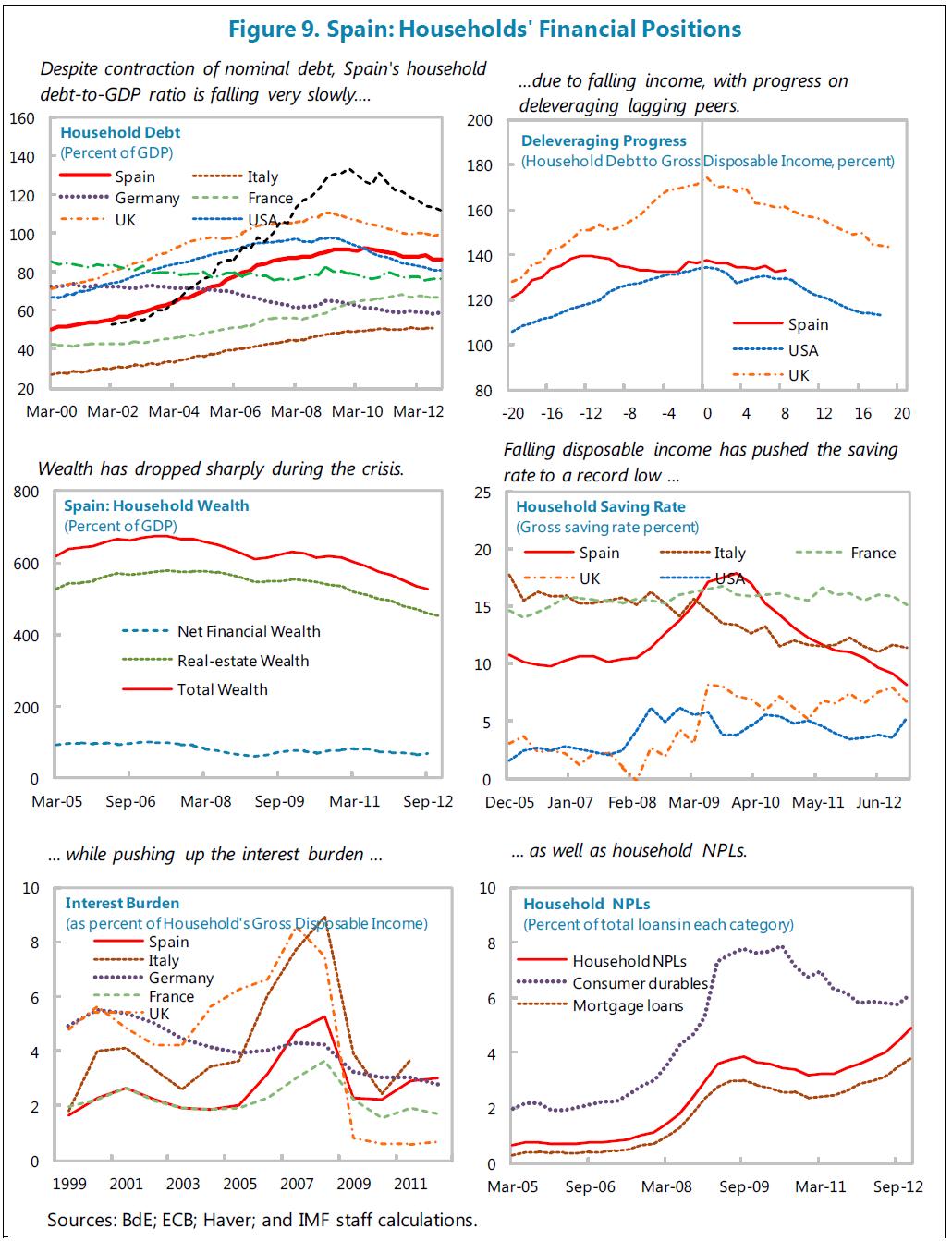

- Falling household incomes are preventing progress on reducing high (above US) household leverage. Median household real income has fallen 10 percent since 2009, forcing households to cut their savings rate to historical lows to support consumption.

Chart 5. Real Median Household Disposable Income

(index, 2008=100)

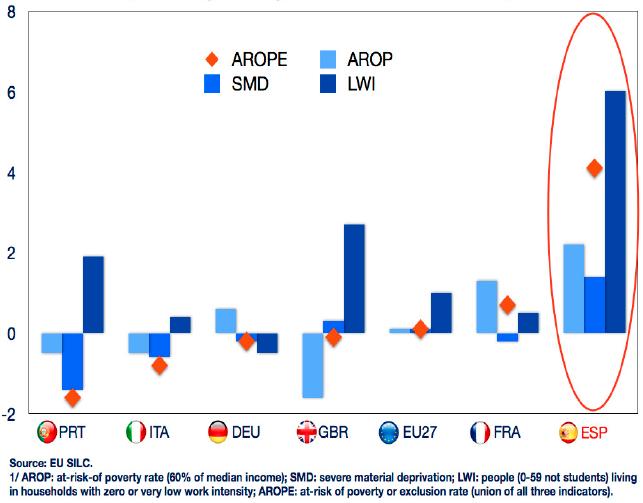

Chart 6. Risk of Poverty and Social Exclusion and its Components

(percentage change between 2008 and 2011)

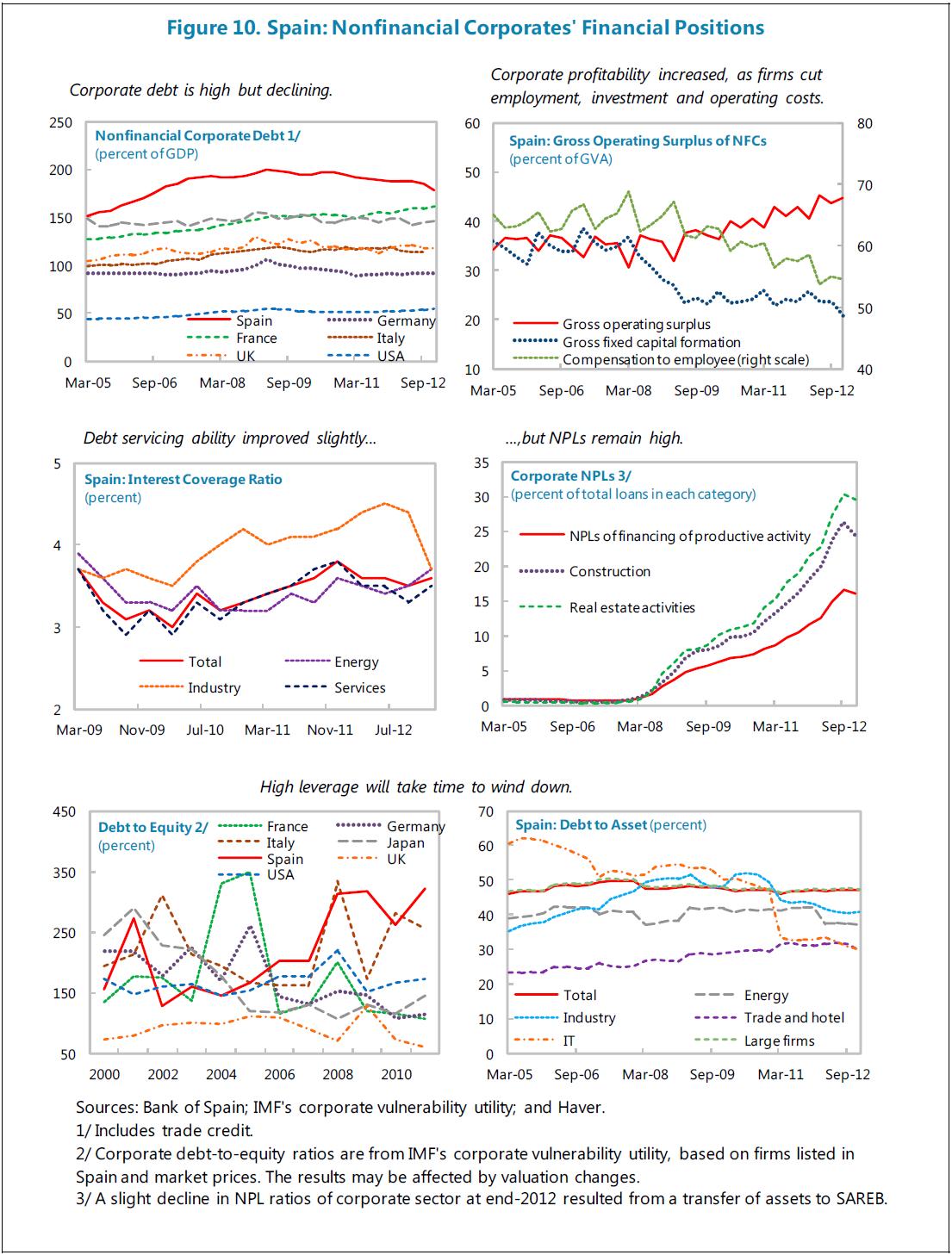

- Firms are deleveraging by cutting employment and investment in the face of costly financing and weak demand prospects and are increasingly net lenders to the rest of the economy. Their debt/GDP ratios, however, remain among the highest in the euro area and twice their 1990-99 levels. While the insolvency law is relatively modern, it is little used to facilitate early rescue of viable firms and swift liquidation of unviable ones (for example, most insolvency proceedings eventually end in liquidation rather than restructuring). There is no personal insolvency regime providing for a fresh start for responsible debtors, unlike most other EU jurisdictions.

- Government debt rose to 84 percent of GDP in 2012 and the 7 percent of GDP deficit remains among the highest in the EU.

Chart 7. Spain: Risks

OUTLOOK: A LONG AND DIFFICULT ADJUSTMENT

3. The outlook is difficult and risks are high.

Recovery from a financial crisis, for both output and unemployment, is typically weaker than a normal recovery. This is compounded by the imperative for fiscal consolidation and private sector deleveraging. Key external risks include a new bout of financial market stress, delayed banking union (both of which would raise borrowing costs for Spain), and a slowdown in Emerging Markets (which would significantly undermine exports as non-euro area countries accounted for most of the recent growth--see the Risk Assessment Matrix). Staff sees three main scenarios:

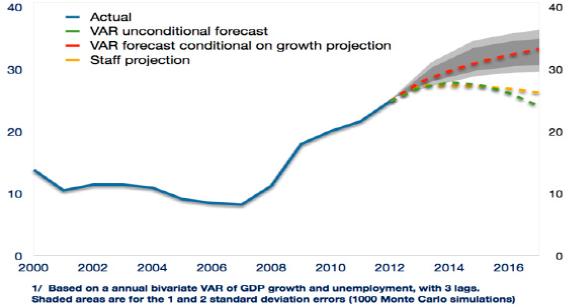

Chart 8. Unemployment Rate Projections

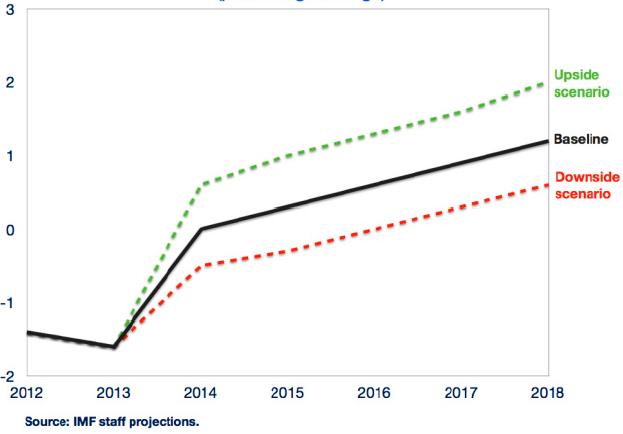

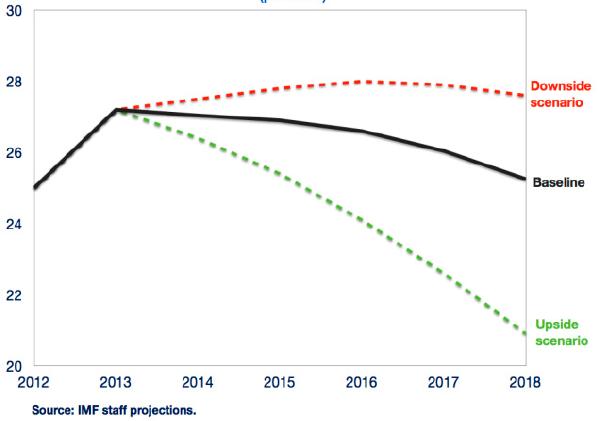

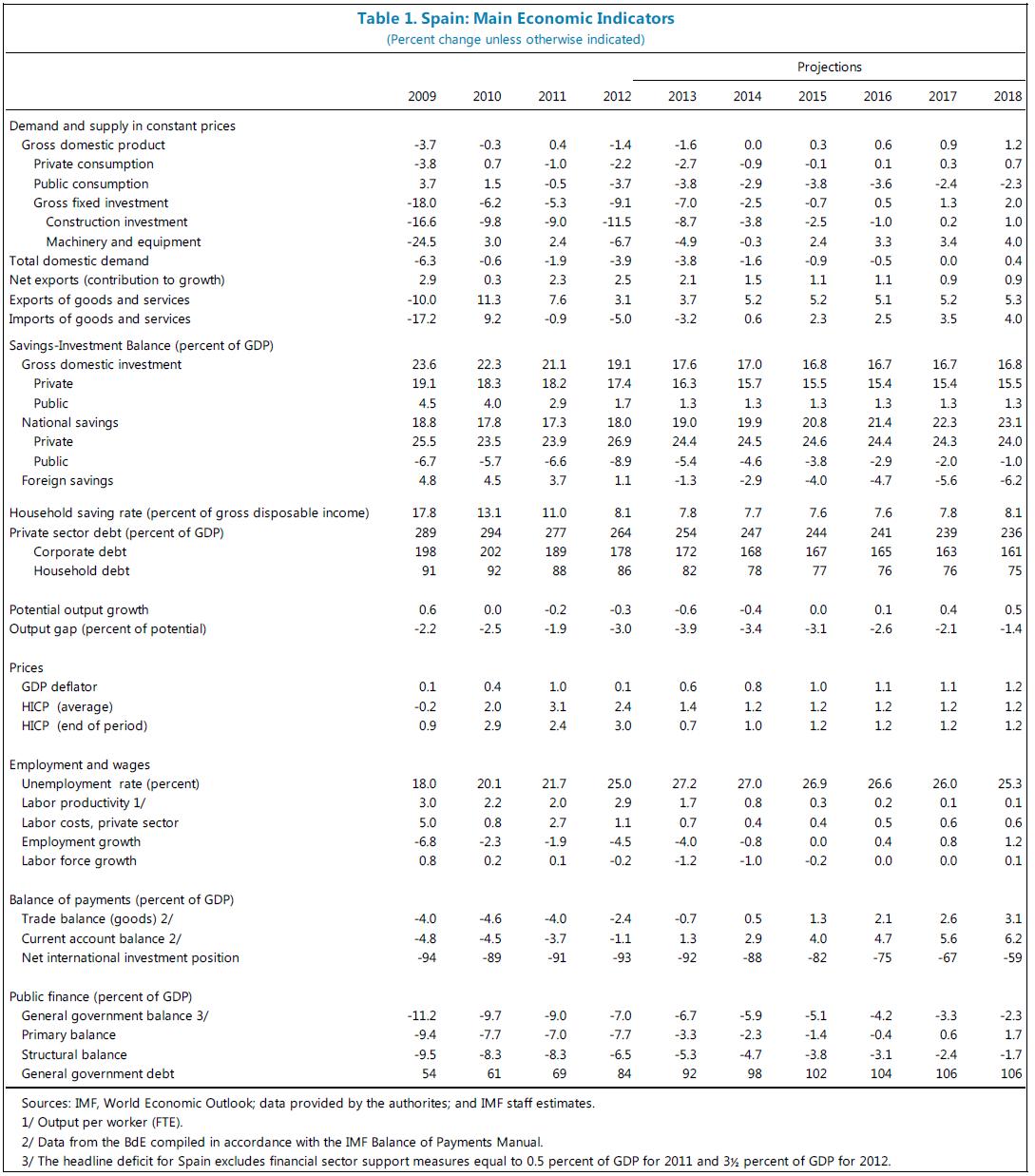

- Baseline--prolonged weakness. The government is expected to meet its structural consolidation targets, implying (inevitably) a drag on growth during the medium term--staff assume a multiplier of around 0.9 on average, reflecting the recession, the relatively closed economy, the exogeneity of monetary policy, high private debt, and the reliance on expenditure reduction. (Important note: staff's baseline, including in the April WEO, had previously assumed no additional discretionary fiscal consolidation as measures had not been fully identified. However, given the government's strong fiscal effort, staff now consider likely that additional measures will be taken to achieve structural targets, even if not yet specified. The incorporation of higher fiscal consolidation improves the proj'ected debt dynamics but also implies a lower growth path; absent this effect, the underlying growth outlook has improved slightly since the April WEO.) Private consumption is likely to remain constrained by modest wage and employment growth, the need to reduce high leverage ratios, and the historically low savings rate. Strong net exports will remain the key driver of the gradual recovery, as exports increase market share in the near future (reflecting gains from a growing export base) and domestic demand restrains imports, resulting in a large current account surplus. Growth, following recent indicators, is expected to turn positive later this year and to gradually pick up to around one percent in the medium term. The weak recovery will constrain employment gains, with unemployment remaining above 25 percent in 2018.

Figure 2. Spain: Private Sector Debt is Weighing on Demand

- Upside. A possible alternative scenario, where reforms (both by Spain and Europe) accelerate and gain more traction, would entail a stronger recovery, in line with the government's projections. The recovery may also benefit from more growth-friendly fiscal measures and would result in growth accelerating to 2 percent by 2018 and significantly boosting employment as labor reforms restrain labor costs over the medium term.

- Downside. Deleveraging pressures and financial distress could intensify, creating a negative macro-financial feedback loop that leaves both private and public debt at elevated levels for the foreseeable future. The fiscal measures adopted could also have high multipliers. As a result, growth would only turn positive in 2017 and unemployment remains above 27 percent.

Chart 9. GDP Growth

(percentage change)

Chart 10. Unemployment Rate

(percent)

4. That Spain adjusts smoothly is of critical importance for the euro area, and hence for the global economy. Spain's outward spillovers through financial markets have been systemic for Europe. Strong sovereign-bank linkages and sizable exposures to the rest of the world through asset and liability cross holdings have made Spain an important hub for receiving and transmitting shocks (see background note). Some of the key global risks emanate from Europe, in particular, that problems in the euro area could re-ignite financial stress in global markets, and prospects for world growth could be hit by protracted stagnation in Europe. A failure by Spain to resolve its imbalances smoothly and restart growth could be one of the triggers. These externalities have been reflected in the large support from the euro area since the global financial crisis, including large-scale ECB borrowing, the ESM-supported financial sector program, the OMT announcements, and more generally the impetus for a more complete monetary union.

5. The political situation appears stable but social tension could compromise the reform effort. The government has a large majority, no general elections until late 2015, and has faced only limited social unrest. But the economic context has reduced the popularity of the two main parties, which could make public support for new difficult reforms more challenging. There is a risk that regional-center tensions could also increase and political fragmentation yield inconclusive elections in the future.

Authorities' views

6. The authorities considered that the staff's baseline medium-term scenario is overly pessimistic and stressed that the government's growth projections are prudent. In particular, they argued that staff's estimated impact of the ongoing structural reforms on growth is very small and that staff assumes an excessively high fiscal multiplier in the medium term. The authorities considered that relatively high fiscal multiplier estimations might be applicable for recessionary periods in the short term in an environment of financial crisis that impedes the reallocation of resources, but less so for the medium term. They also pointed out that there are recent encouraging indicators that the economy is stabilizing. Investment, employment and confidence were gravely affected by the broader euro area financial crisis and financial fragmentation in 2012. In an improved environment in which the financial sector channel ceases to be impaired, the authorities argued that fiscal consolidation will be less of a drag on growth beyond the short term. That said, the authorities recognized the challenges, including the difficult initial conditions, and reaffirmed their commitment to advance the reform process, which will help increase competitiveness, employment, and growth.

THE POLICY IMPERATIVE: JOBS AND GROWTH

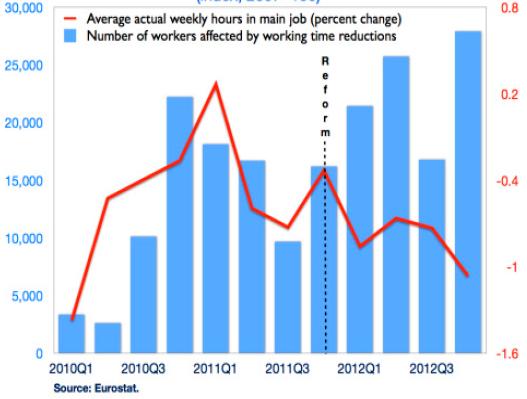

Chart 11. Working Hours Flexibility

(index, 2007=100)

7. This outlook calls for raising the reform effort to the level of the challenge. Spain-- supported by euro-area policies--needs to deliver on its announced program, and indeed go further in key areas. The focus should be on a jobs-friendly strategy that allows the economy to grow and hire rather than shrink and fire. This means making prices adjust rather than quantities, helping the private sector delever, making sure banks can extend credit to healthy businesses, and minimizing the drag from the inevitable fiscal consolidation. It also means avoiding any tendency to take the prospective economic stabilization as a reason to slow the reform effort.

A. Labor: Reinforcing the Reform to Generate Jobs

8. The recent reform is having some positive effects. Wage growth has moderated, firms are using the increased flexibility to reduce working hours instead of reducing jobs, and opt-outs are increasing. Wages in the public sector and large firms have fallen. The share of "objective dismissals" has increased and dismissal costs have fallen.

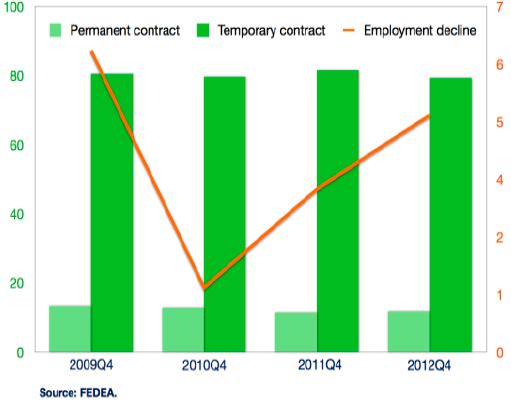

Chart 12. Probability of Finding a Job by Type of Contract

and Employment Destruction (percent)

9. But other components of the reform have been less successful. There has been little change in the sharp division (i.e., duality) of the labor market between those with permanent jobs (with high dismissal costs) and those with temporary jobs (with low dismissal costs). The probability of finding a permanent job remains too low and that of losing a temporary job too high. Recruitment under the new permanent contract was only a small fraction of hiring. While the use of opt-outs clauses is growing, in the 12 months following the reform, they covered less than one percent of industry-region wide contracts. There is still some uncertainty about the judicial interpretation of the criteria for objective dismissal.

10. Labor market dynamics do not seem to have improved sufficiently. Increasingly, wage inflation in the private sector is moderating, but has not fallen commensurately with the large excess supply of labor. Although this situation may change in the coming months with the expiry of many agreements, private sector wages have grown 10 percent between 2008 and 2012 (in line with the euro area) while employment fell 15 percent (much more than in the euro area). Other countries facing similar shocks but with more flexible labor and product markets have fared better.

Chart 13. Nominal Wage

(Index, 2000Q1=100)

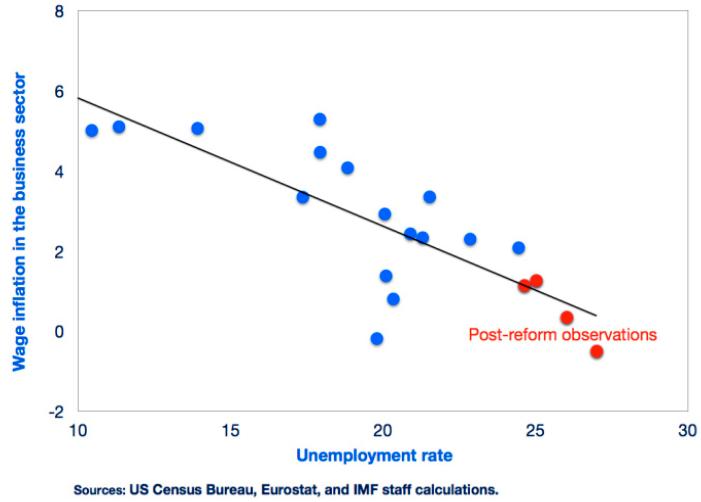

Chart 14. The Wage Philips Curve since 2008

11. Thus, labor market dynamics need to improve to reduce unemployment sufficiently. The burden of adjustment is still falling on employment (especially temporary and youth) rather than wages. Spain has historically never generated net employment when the economy grew less than 1˝-2 percent. Yet growth is not projected to reach these rates even in the medium-term. Thus reducing unemployment to its structural level (still likely very high at around 18 percent) by the end of the decade would require a significant improvement in labor market dynamics. In particular, faster wage adjustment would likely lead to fewer people losing jobs (or consuming less for fear of this risk) and more unemployed being hired, both of which would lead to more private consumption. Businesses would also be more likely to hire and invest and net exports would contribute even more to demand.

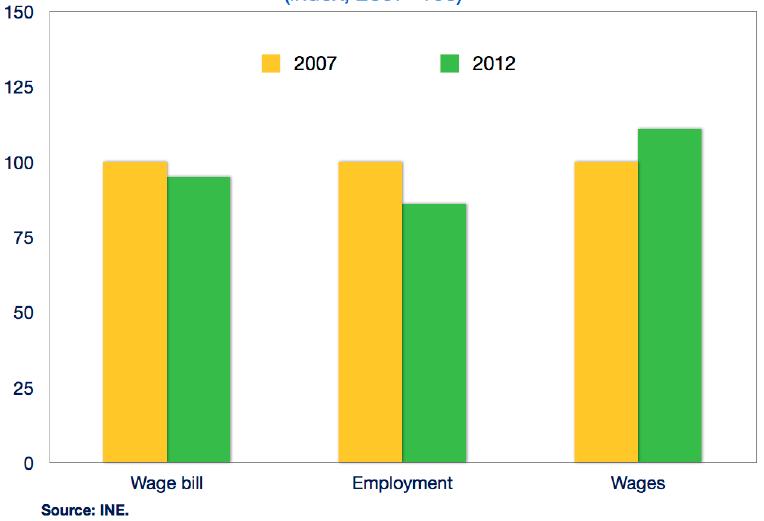

Chart 15. Spain: Nominal Wage Bill Evolution

(index, 2007=100)

Chart 16. Growth and Unemployment, 1978-2008

12. This suggests that the recent reform should go further. The government encouragingly intends to review the reform in the coming months, involving an international expert organization, such as the OECD. In the context of such a review, consideration should be given to:

- Increasing flexibility. Wages and work arrangements should be more responsive to economic conditions. If no major improvement is seen as many agreements are re-negotiated this summer, deeper reform of collective bargaining may be needed, e.g., liberalizing opt-outs further or moving to a fully decentralized system. Eliminating "ultra-activity" (whereby contracts remain valid after they expire) and indexation would also support wage flexibility.

- Reducing duality. This should ideally entail greatly reducing the number of contracts, based on a permanent contract with dismissal costs initially low and progressively increasing with job tenure. Alternatively, severance payments for permanent contracts should be aligned to EU average levels, the scope for judicial interpretation in dismissal proceedings reduced, and eligibility criteria for the recently-introduced permanent contract relaxed.

- Enhancing employment opportunities. To help the unemployed find jobs, they need better training and placement services. For certain groups, such as the young and the low-skilled, more ambitious policies to reduce the cost (including tax cost) of employing them may be required.

13. An agreement between unions and employers could bring forward the job gains from structural reforms. Even under an upside scenario, wages and hiring would only adjust gradually, implying a protracted period of very high unemployment. Such an agreement could help accelerate this process and coordinate the economy to a better outcome (see Box on model-based simulations) and comprise: (1) employers committing to significant employment increases in return for unions agreeing to wage reductions and (2) some fiscal incentives in the form of immediate cuts in social security contributions offset by indirect revenue increases in the medium term. A large employment response and reduction in inflation will be critical so that household purchasing power in the aggregate does not suffer. Such an agreement should complement, not substitute, for structural reforms. The challenges for all parties involved are enormous, and it will be crucial to avoid an agreement that waters down or delays needed structural reforms.

14. This is a complex issue and various interlocutors expressed misgivings. Some argued that a strong agreement would be difficult to negotiate and enforce, there being currently little common ground between the different stakeholders. Unions will understandably be reluctant to accept further wage moderation and employers equally to give employment assurances. Others argued that if the employment response is not forthcoming, the result could be a significant drop in demand, a larger household debt overhang, and a higher deficit. There is also the risk that other structural reforms are delayed. Nevertheless, given the enormous size of the challenge faced and recognized by all parts, staff sees merit in exploring this option--if not now, in the future were unemployment not to fall significantly.

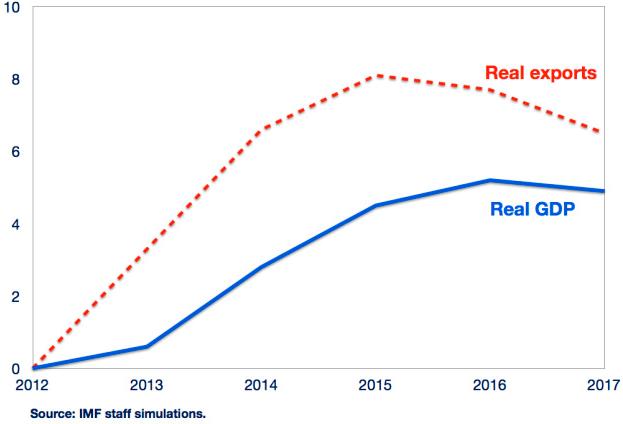

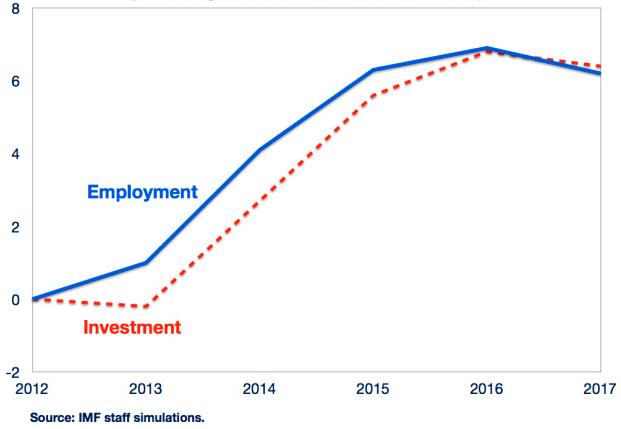

Model-simulations illustrate the potential benefits from an ambitious social agreement on growth and employment from a faster process of internal devaluation. The assessment uses the IMF Global Integrated Monetary and Fiscal Model and is based on: (1) an agreement to reduce nominal wages, for illustrative purposes, by 10 percent over two years; and (2) a temporary fiscal stimulus to the wage cuts: social security contributions are reduced (the contribution rate is cut by about 1% percent), followed by an increase in the VAT two years later (e.g. by broadening the base rather than raising the main rate)--the lag helps households during the period of falling wages. The adjustment in wages and prices is relatively fast, as the social agreement is assumed credible.

Real GDP and Exports

(percentage, difference relative to baseline)

Employment and Investment

(percentage, difference relative to baseline)

The results, while subject to inherent limitations of the model, suggest the wage reduction, and associated fall in prices, would have a significant positive impact on economic growth and support the fiscal adjustment. The wage/price decline would result in a real depreciation of around 5 percent over 3 years, boosting exports and slowing imports. Importantly, a credible social agreement would also have a large positive impact on investment given the lower production costs and improved outlook. As a result, GDP would be 5 percent higher than in the baseline. The fiscal deficit increases, but would fall rapidly afterwards as the fiscal accounts benefit from the VAT revenue increase and the stronger economy-- in both cases public debt is lower than in the baseline in the medium term.

Employment would be 7 percent above the baseline scenario. With the fall in nominal wages, employment would grow at a faster pace especially in the second and third years--reducing the unemployment rate by about 6-7 percentage points by 2016. Private consumption could fall somewhat in the first year, but the drop would be limited as households benefit from lower social contributions. Nevertheless, the simulations suggest that the rise in employment and lower CPI inflation (prices would be lower by 4-5 percent after two years) would prove enough to boost consumption growth already in the second year. The model also has savings rising by 2-2˝ percent in the first years (to proxy for household debt effects)--if this does not happen, consumption could be further supported. Over the medium term, consumers are better off in both scenarios given stronger output and employment.

Authorities' views

15. The authorities argued that the labor market reform is working but will take more time to see its full impact. They underscored that economic agents are still learning how to use the new tools. Following the reduction of 'ultra-activity', a number of collective agreements will expire, triggering an opportunity to adjust working conditions, foster labor productivity, and protect jobs. The government also pointed out that it was unrealistic to expect a quick recovery in hiring during such an intense recession and with financial fragmentation.

16. There was some recognition that a social mechanism on the lines staff suggested might have theoretical appeal, but it was viewed as difficult to be achieved and entailing some risks. The authorities did not see the present social environment as sufficiently receptive for such an agreement and feared that trying to reach one might stall crucial structural reforms. There was also concern about a broad range of implementation problems like the difficulty to differentiate across sectors and individual businesses, as well as the risk of unstable dynamics if the agreement is incomplete, including through the impact on household spending and the ability to service debt.

B. Helping the Private Sector Delever

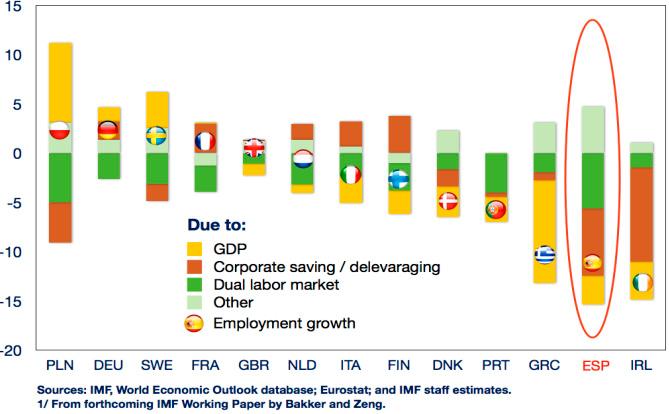

Chart 17. Drivers of Employment Loss, 2008-2011

(Employment growth percent)

17. The necessary deleveraging of high private sector debt should be made as efficient as possible. Resources currently tied up in non-viable firms need to be reallocated to viable firms that can invest and hire, and debt-overhangs should not impede profitable operations. Insolvent, but responsible, individuals should have the prospect of eventual discharge from their debts and the incentive to participate in the formal economy. While any change must not compromise financial stability, there is scope to continue to improve the insolvency regime (see background note):

- Corporate. The process could work better by: (1) reforming the legal framework to provide incentives for early rescue of viable firms and eliminate heavy procedural requirements to expedite liquidation of unviable firms (2) strengthening the institutional framework (e.g., enhancing commercial courts' capacity) and (3) setting up frameworks to further encourage out-of-court debt restructurings, particularly for SMEs (e.g., mediation).

- Personal. The authorities have implemented important measures to address residential mortgage debt distress. To strengthen the toolkit for addressing household debt distress more generally, priorities include: (1) fine-tuning existing measures to support further out-of-court restructurings (e.g., centralized guidelines for workouts; mediation) (2) further improving access to information and advice for highly-indebted individuals and (3) considering in the future establishing a special personal insolvency regime with a fresh start for financially responsible debtors.

18. Staff viewed the measures to address residential mortgage distress a step in the right direction but not enough to help over-indebted--but financially responsible--individuals. Hence, going forward, a more comprehensive approach that includes an effective personal insolvency regime with strict eligibility conditions for clearly insolvent people who dispose of their assets, including their houses, to pay their outstanding debts and remain financially responsible over a reasonable period of time (normally 3 to 5 years) to obtain a fresh start. Other countries, including several in the EU since the crisis, have already introduced such regimes without endangering financial stability or affecting credit discipline and payment culture.

Authorities' views

19. The authorities considered recent measures adequate. The measures addressed to more socially vulnerable households offer a high degree of protection for the debtor (including the possibility of cancelling the mortgage by transferring the property, and offering opportunities for public housing), and the mortgage law has been modified to rebalance the position of mortgage debtors and providing for a system of debt relief. They also consider that they represent an adequate balance between financial stability and the necessity to address household debt distress. In the current situation, a personal insolvency regime that includes a different solution for mortgages would overburden the courts, could lead to strategic defaults, and jeopardize Spain's strong payment culture. The authorities are preparing new legislation to address corporate debt overhang and were open to consider proposals to further improve the corporate insolvency regime.

C. Financial: Supporting Credit While Safeguarding Financial Stability

20. The ESM-supported financial sector program has accelerated the clean-up of the system. The Memorandum of Understanding signed in July 2012 provided a clear roadmap and the resources for implementing the necessary overhaul, under tight deadlines. Important progress has been achieved (as detailed in the Fund's quarterly monitoring reports). Weak but viable banks have been recapitalized through an independent stress test exercise and an asset quality review, and restructuring/resolution plans adopted. Additional capital augmentation has been achieved through burden sharing with subordinated debt and preference shares, the transfer of assets and loans to a newly incorporated asset management company (SAREB), and private-capital raising efforts. Through a new draft law, the regime for savings banks is being substantially improved. The Bank of Spain's regulatory and supervisory powers and procedures have also been strengthened.

Chart 18. Spanish Banking System:

Profits, Losses and Dividends (billions of euro)

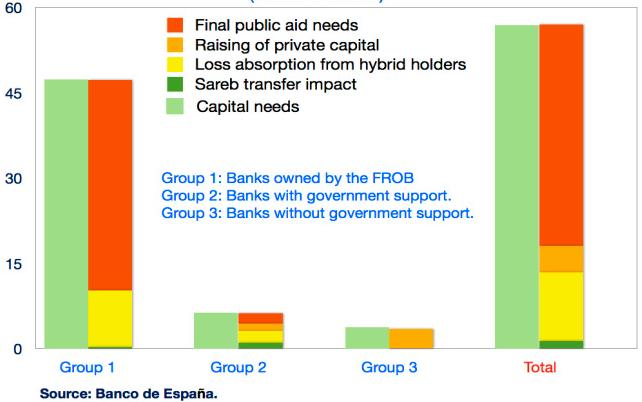

Chart 19. How the Stress Test Capitals Shortfalls Were Covered

(billions of euro)

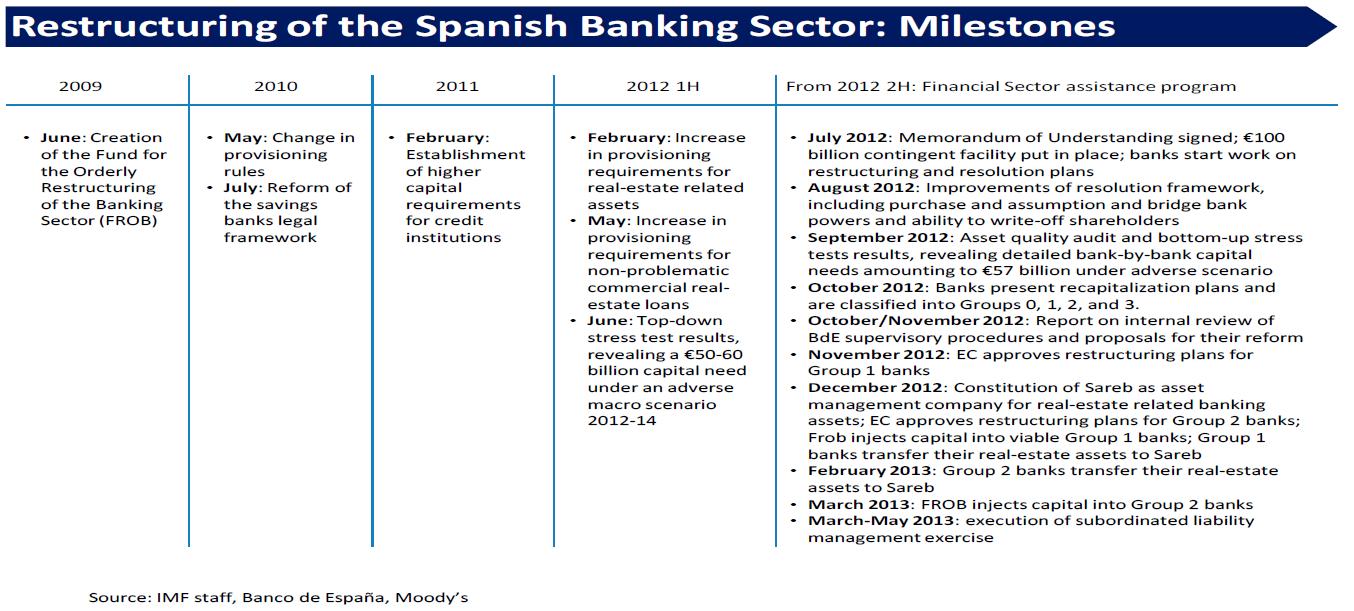

Restructuring of the Spanish Banking Sector: Milestones

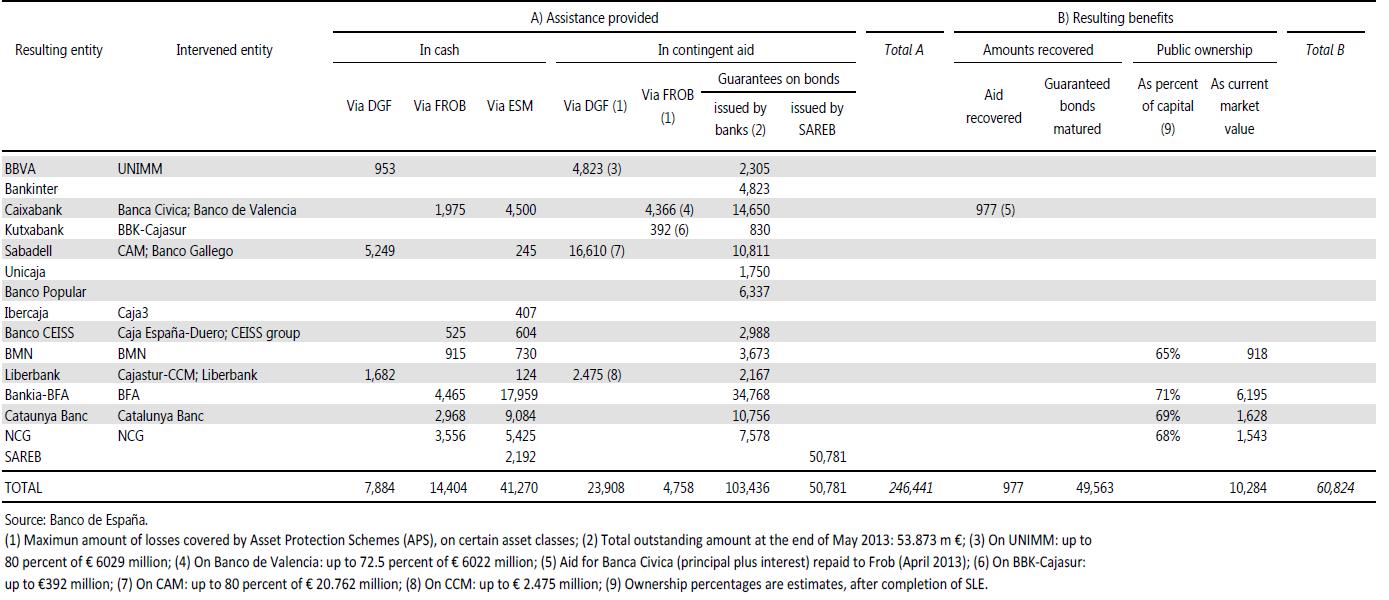

21. This clean-up has so far cost about 6 percent of GDP in public money, excluding large contingent liabilities. Since the first financial support measures launched in 2009, some €63 billion has been injected by the state into the system, of which €41 billion was drawn from the EFSF/ESM. On top of this, contingent aid has been provided under the form of either state guarantees on bonds issued by banks and SAREB (€105 billion outstanding) or asset protection schemes. While there was considerable burden sharing, the government decided not to take full ownership of the insolvent institutions recapitalized with public funds and chose to grant holders of subordinated debt and preference shares substantial equity in the new institutions (around a third on average, totaling about €4% billion at mid-June market values), reducing future potential returns to the taxpayer.

Restructuring of the Spanish Banking Sector: The Taxpayer's Balance

(cumulative balance until May 2013)

22. The banking system is now stronger, safer, and leaner. The system's capital has been boosted, with all banks covered by the stress test over the minimum regulatory requirement (9 percent core tier I) at end-March, once the estimated effects of pending capital augmentation measures (e.g., completion of burden-sharing exercises and sales/mergers under the program) are included (though core tier I ratios are still on the low side compared to peers under fully-loaded Basel III). Credit provisions have also increased and the intervened banks are implementing EC-approved restructuring/resolution plans. The number of banks fell from 50 in 2009 to 15 currently, with employees and branches reduced by about 13 percent over this period.

23. But risks remain elevated. While the ESM-supported program is helping tackle legacy problems, risks, especially macro-financial, continue to loom large, in line with the difficult macroeconomic outlook:

Chart 20. Improvements in Capital and Provisioning, 2008-12

(percent)

- Loan books will likely continue to deteriorate. As long as economic growth remains weak and unemployment stays high, nonperforming loans will continue to increase, and with them the need for banks to provision.

- Earnings will likely remain under pressure. They will be impacted by low business volumes, low margins, and high credit provisions. Some banks may struggle to generate enough profit to maintain current capital levels without further deleveraging.

- Access to markets will likely remain limited, and expensive. Unless sovereign and bank spreads decline significantly, wholesale markets will remain too expensive to be a major funding source for many banks. Indeed, bond yields and market volatility have risen since May and, if sustained, could force weaker banks to rely on the ECB for funding and/or to delever faster.

- Banking and macro interactions could generate a negative feedback loop. If the macroeconomy weakens and the outlook remains uncertain, banks could delever faster, which in turn could lead to less growth and weaker confidence.

24. There are also operational risks. SAREB has a large number of assets that are complex and costly to manage and whose price is intimately linked with economic prospects. Restructuring / resolution plans of intervened banks are complex and challenging, and the franchise value of the weaker ones might fall faster. The burden sharing exercise involves many thousands of retail investors and entails litigation risk from potential widespread allegations of mis-selling.

25. These risks call for proactive vigilance to protect the hard-won solvency of the system and to support credit and growth, in particular, continuing to:

- Keep banks' loan books clean and reinforce the quantity and quality of capital. The recent guidelines tightening classification of refinanced loans (some 15 percent of total loans) should be used for this end and the market for distressed assets should be fostered (for example, by moving the tax on real estate transactions to real estate values and tightening time limits on full write-offs). This may require more provisioning and/or capital, which in turn calls for extremely prudent capital management. To avoid exacerbating credit constraints, the focus should be on increasing the nominal amount of capital, for example, via restrictions on cash dividends or issuing more equity. Raising fresh capital would be challenging in a downside environment.

- Remove possible credit supply constraints, while preserving loan quality. There are no straight-forward solutions, but consideration could be given to credit risk sharing via targeted guarantee and securitization schemes, further fostering non-bank financing, and clearing public sector arrears. Maintaining bank access to ample and cheap Eurosystem liquidity would also help.

- Provide incentives. The above actions (e.g., issuing equity, forgoing dividends, stepping-up provisioning, disposing of distressed assets, easing the pace of credit contraction) could be further incentivized by the government offering to swap banks' deferred tax assets (some €51 billion, a third of core tier I capital) for tax claims (as recently implemented in Italy), conditional on the degree to which banks take the above actions. This would improve the loss absorbency and liquidity of banks' capital at potentially little cost to the government.

26. Supervisory practices should build on achievements under the financial sector assistance program. In particular, rigorous and regular forward-looking scenario exercises on bank resilience and capital needs should occur regularly to guide supervisory action.

27. By contrast, banks argued that falling SME credit reflects falling demand from healthy firms. They argued they have liquidity and the incentive to lend given high SME lending rates, and that the problem is one of inherent risk of lending to SMEs in the current macroeconomic context. More generally, it was desirable and inevitable that credit should fall after the boom and reflects the necessary restructuring of the system--more lending now could just mean more losses later. Staff countered that distinction between demand and supply is not clear cut--lower lending rates would increase the amount of demand--and there are also signs that there could be credit supply constraints. Survey data indicate banks have tightened lending standards for a given creditworthiness and more firms indicate "access to credit" as their most pressing problem in Spain and the periphery than the core. Rising lending rates also seem inconsistent with a pure demand shock. There could also be disruption to credit relationships as many state-aided banks downscale operations as part of their restructuring plans.

Authorities' views

28. The authorities largely agreed with the analysis and policy implications. While considering legacy problems from real estate largely addressed, they agreed that the risk now is that the hard-won bank recapitalization could be affected if macro weakness were to continue for longer than expected. They are developing an internal methodology to conduct, on a regular basis, different scenario exercises to assess bank resilience. They stressed that while earnings retention should have priority over dividends, this has to be targeted bank by bank, given the widespread differences in the system. On loan loss recognition, they underscored that the newly tightened supervisory rules will indeed improve the transparency of banks' balance sheets and enforce appropriate provisioning. The authorities shared the preoccupation on credit, but stressed the difficulty in disentangling demand and supply factors and emphasized the need to improve the monetary transmission mechanism and financial fragmentation. They are working on measures to address the financing of the real sector.

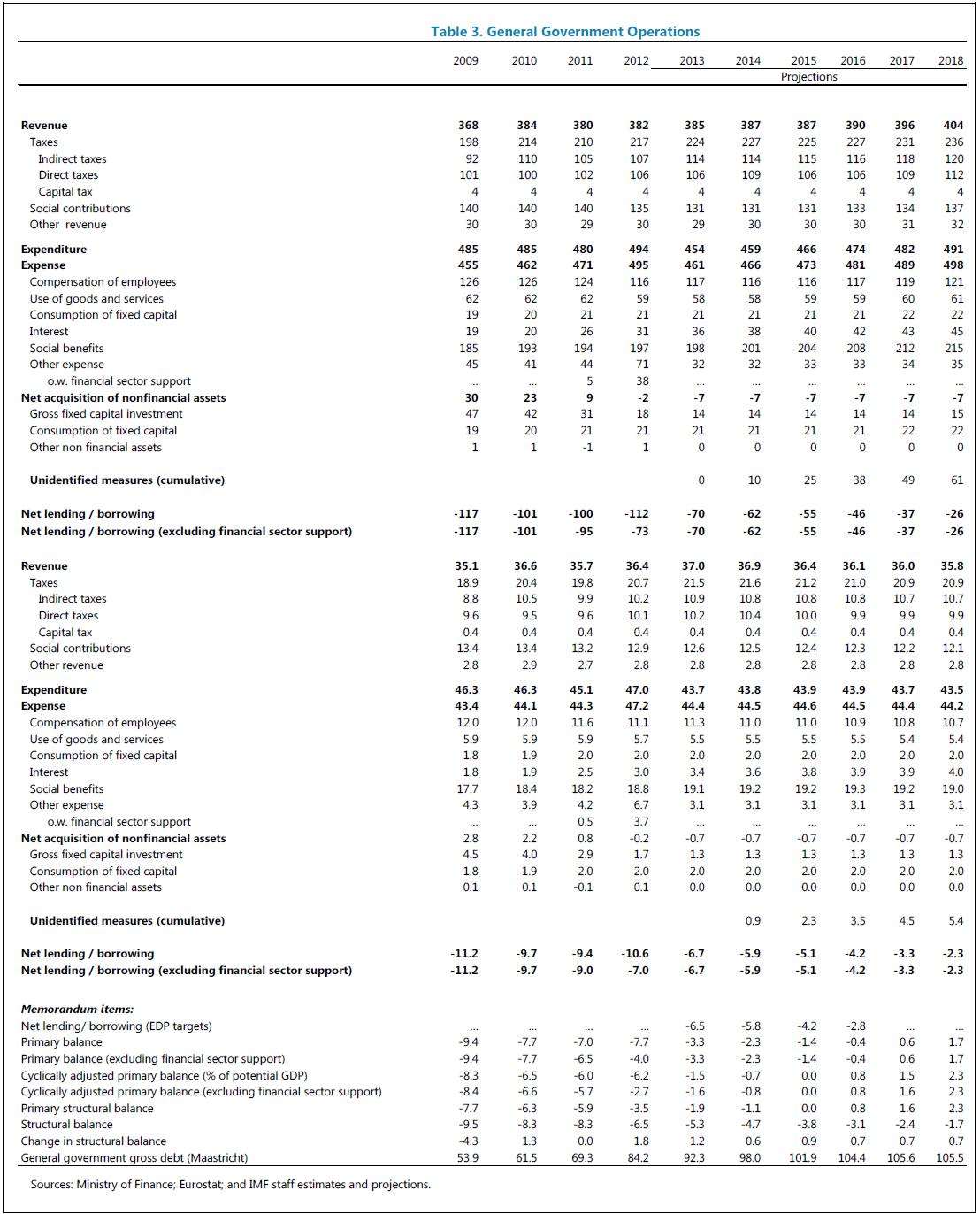

D. Fiscal Consolidation: Minimizing the Inevitable Drag

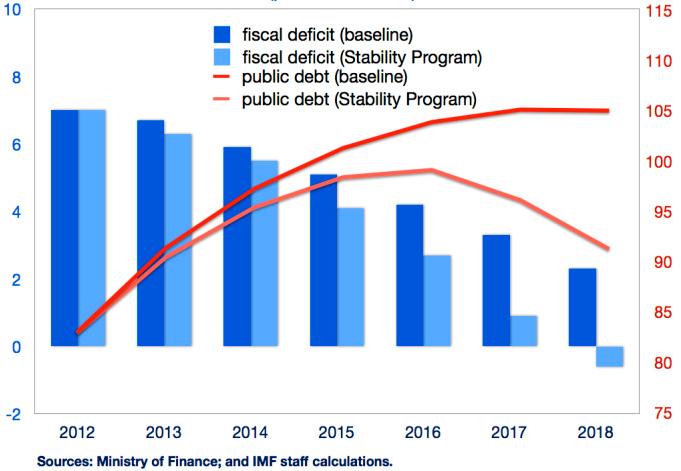

Chart 21. Fiscal Deficit and Debt

(percent of GDP)

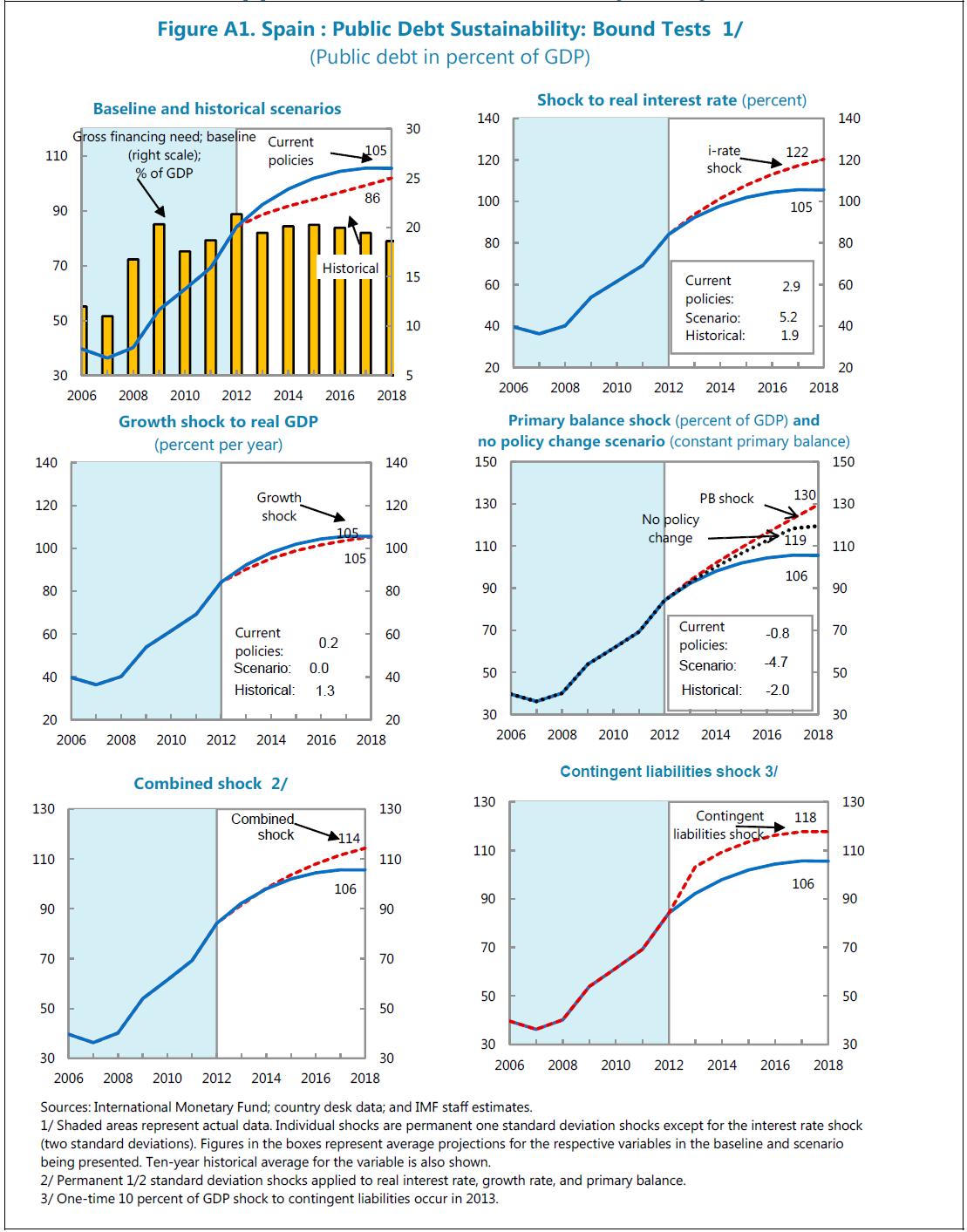

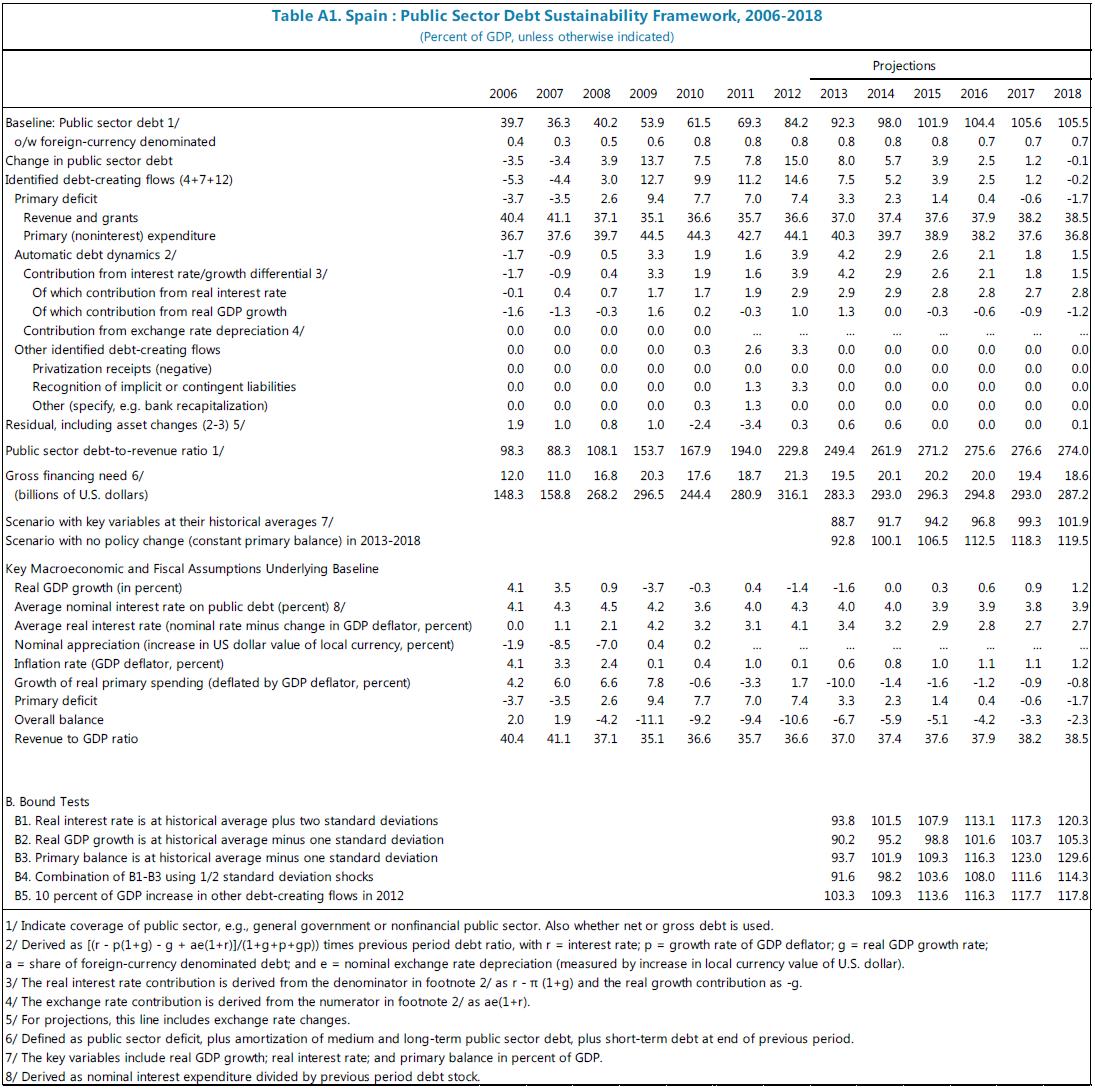

29. Even after considerable effort, Spain is only half way along its needed consolidation path. Under staff's baseline scenario (which combines the government's underlying fiscal effort with staff's more conservative macroeconomic assumptions), the public debt-to-GDP ratio will continue to grow until 2017 before declining at an accelerating pace thereafter as the structural deficit is eliminated by 2020. This structural balance anchor is consistent both with constitutional requirements and with putting debt on a significant downward path in the medium term so that public finances are sustainable and financing vulnerabilities reduced--a necessary condition for stronger growth in the future. This requires a very large structural fiscal effort given the implied need to improve the primary deficit (4 percent of GDP in 2012) to a considerable surplus (of around some 3-4 percent of GDP) in the medium term, and the weak growth outlook. Such an adjustment would be very large by international comparison.

30. To minimize the economic and social cost, the consolidation should be gradual. The government's new medium-term structural deficit reduction targets strike a reasonable balance between reducing the deficit and supporting growth (with the cyclically-adjusted primary balance improving by about 0.8 percent of potential GDP from 2014). Given the need to stabilize the economy and assuming the structural consolidation in train for 2013 is delivered, significant additional measures for 2013 are undesirable. Going forward, it will be important to be flexible on the nominal (and, if necessary, structural) targets if growth disappoints.

Stability Program Update, 2013

(percent of GDP)

31. The adjustment path should be made more concrete and growth-friendly. The lack of sufficient specific measures in the government's medium-term fiscal plan and, to a lesser extent, the lack of buffers in the macro framework (compared to staff's baseline) undermines credibility, fosters ad hoc measures, and raises uncertainty.

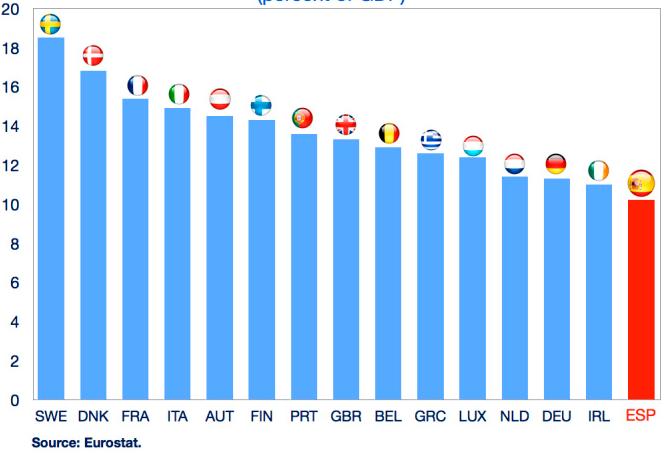

Chart 22. Eu 15: Indirect Tax Revenue, 2012

(percent of GDP)

- In the near term, measures COUld fOCUS Chart 22. EU15: Indirect Tax Revenue, 2012 more on increasing revenues from indirect taxes, which is relatively low, levied on a narrow base, and likely also to have low multipliers. This could be achieved by broadening the base of the standard rate of VAT and increasing excises.

- To develop measures for future budgets, it would be useful to conduct targeted expenditure reviews of key functions such as health and education. The tax system would also benefit from being reviewed to mobilize more revenue in a more efficient and fairer way. A deepening of the 2011 pension reform is needed given the significantly worse dependency ratio projections and recent labor market trends (see background note). The impact on the poor of the consolidation measures should also be explicitly considered and counter measures implemented.

32. The fiscal framework is being substantially upgraded and should be followed through with ambitious legislation and rigorous implementation. In particular:

- Developing a more predictable and transparent approach to applying the enforcement provisions of the recent Organic Budget Stability Law. The strong performance by the regions in 2012 owed less to these enforcement provisions than to conditions (especially the reliance on financing from the center) which may not apply in the future. Thus continuing to develop the enforcement of the Organic Law would address the risk of future slippage and cement recent gains (see background note).

- Strengthening the independence, both real and perceived, of the planned fiscal council is paramount. This would be helped by a non-renewable presidential term of at least five years.

- Securing the sustainability of the pension system. The expert committee's proposal on the "sustainability factor" provides a strong framework for sustainability and for evaluating alternative reform options.

- Following through on the creation of a panel of experts to advise on tax and regional financing reform. Expenditure reviews, looking across several levels of public administration, would help find synergies, more efficient delivery of public services, and identify growth-enhancing measures.

- Further improving budgeting and transparency, especially by combining the dispersed budgets and regional multi-year consolidation plans into one medium-term budget based on a detailed general government macro-fiscal projection, a baseline under unchanged policies, and with the impact of specific measures identified. Short of medium-term budgeting, future measures legislated now could ensure that targets are met. Risk reporting could improve by including stochastic and alternative medium-term scenarios and improving coverage of contingent risks (e.g. financial sector, road concessions, PPPs).

Authorities' views

33. The authorities underscored the remarkable reduction in the fiscal deficit in 2012 in the middle of a recession and agreed with many of the above proposals. They also highlighted that all regional governments made significant progress in reducing their deficits and that fiscal reporting at the sub-national level was substantially upgraded. They also argued that the recently revised fiscal targets are more adequate, considering the state of the economy, and they are confident of meeting them. They agreed with the need to conduct tax and expenditure reviews and they pointed to the recent proposal on the pension sustainability factor by a panel of experts. The authorities viewed the new system of fiscal control as working well, even though modalities for its implementation are still being developed. They also highlighted that extraordinary liquidity facilities are complementing the enforcement provisions in the new Organic Budget Stability Law.

E. Structural: Building a World-Class Business Environment

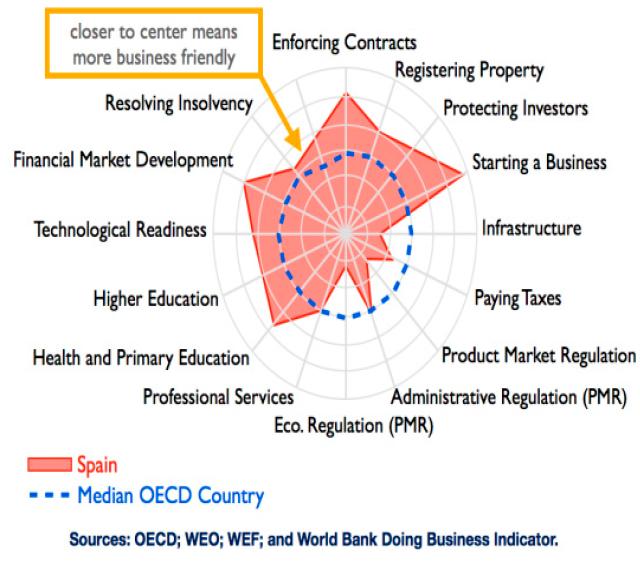

34. Spain needs to do more to improve its business environment and boost competition.

Spain ranks only modestly in international comparisons, benefiting from strong infrastructure, but suffering from the high burden of starting a business, administrative regulations in product markets that limit trade, and professional services that are not fully liberalized. Spain's production structure is dominated by SMEs, which tends to slow productivity growth. These factors result in a lack of competition, highlighted by the lack of progress since the crisis in reducing the inflation differential built up during the boom years. Greater competition would also complement the labor reform by reducing profit margins and prices, and increasing the demand for labor.

Chart 23. Consumer Prices

(cumulative change in the period, percent)

Chart 24. Business Environment:

Selected Rankings within OECD, 2013

Chart 25. Impact of Structural Reforms

(percent of potential GDP)

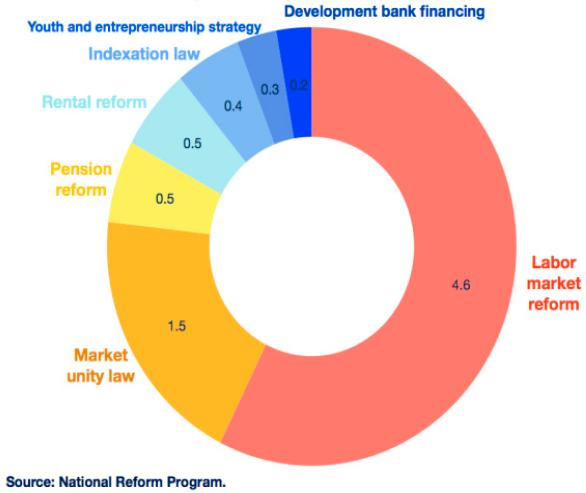

35. The government plans a range of reforms in its National Reform Program (NRP) on which it needs to deliver fully and quickly. This will help Spain gain credibility in the short term and reap the growth benefits (estimated by the government at around 8 percent of GDP) in the medium term. The program for Market Unity, which will facilitate trade across regions in Spain, is potentially important and is underway. The much-delayed law to liberalize professional services needs to be delivered quickly and without being undermined by vested interests. With the aim of containing second round effects in inflation, the government has announced legislation to reduce indexation of prices in government operations. Consideration should also be given to reforms that encourage firms to grow (e.g., thresholds on firm size in the tax code). An independent "growth commission" (e.g., Australia's Productivity Commission) could help set priorities, identify key measures and overcome political obstacles.

Authorities views

36. The authorities agreed that Spain needs to boost competition, which their policies are targeting. The authorities are committed to fully implement their National Reform Plan. In addition to the flagship reforms, which will be approved according to the announced schedule, they are also continuously reviewing regulations to improve the business environment.

37. Much more should be done at the European level to ease Spain's adjustment. Spain is systemic to the euro area and has been a key source of outward financial spillovers. While recent euro-area actions have reduced tail risks and alleviated financial market stress, they have not been sufficient to reverse fragmentation, improve monetary transmission, and deliver higher growth and employment, neither for the euro-area nor for Spain. Faster progress to full banking union, (including, if necessary, a flexibly used ESM bank recap mechanism), could break the sovereign/bank loop, allowing Spanish firms to compete for funds on their own merits rather than their country of residence. Further measures (including by the ECB) to reduce financial market fragmentation and ease credit conditions would help Spain's adjustment. Spain would also benefit from flexible application of financial sector state-aid rules (i.e., deleveraging requirements attached to public capital injections), other European countries not ring-fencing their banks, and more support channeled through common resources (e.g., the EIB). Spain and the euro-area should also keep the option of an OMT-eligible program open as it could help cement market confidence and lower yields.

Authorities' views

38. The authorities strongly agreed that more decisive action by Europe is needed, especially with banking union and the repair of the monetary transmission mechanism. While the sovereign has benefited from recent European actions, Spanish private institutions have not, and progress at the European level has fallen short of the challenges. The authorities noted that Spanish banks and firms are facing much tighter funding conditions than their peers in core Europe, independently of the financial strength of the individual firm. The problems are particularly exacerbated for SMEs. The authorities stressed the critical issue now is to create the conditions for credit to flow and promote economic growth in the Euro area. In particular, the ECB could do more to repair the monetary transmission mechanism and faster progress should be made in implementing the banking union to create a level playing field, solve the lingering problem of ring-fencing of financial assets within the euro area, and ensure financial stability.

39. Progress on critical reforms has been strong and the needed adjustment is well underway, but the economy remains in recession amid unacceptable levels of unemployment. Decisive reforms in the labor, financial, and fiscal sectors, in line with past staff recommendations, is helping stabilize the economy. External and fiscal imbalances are correcting rapidly. Sovereign borrowing costs have improved substantially. But, hampered by private sector deleveraging, fiscal consolidation, and labor market rigidities, output has contracted for seven quarters and unemployment has reached 27 percent.

40. The outlook remains difficult and risks are high. Growth should start to turn positive later this year, but will likely only gradually pick up in the medium term, with limited gains in employment. A more favorable scenario is within reach, especially in the medium term if the envisaged reforms are fully implemented by Spain and Europe. But there are also significant downside risks which could result in a more protracted recession.

41. This calls for urgent action to generate growth and jobs, both by Spain and Europe. Spain needs to deliver on its announced program, and indeed go further in some areas, while euro area policies need to be more supportive. It also means avoiding any tendency to take the prospective economic stabilization as a reason to slow the reform effort.

42. Labor reform needs to go further to generate jobs. Last year's reform made substantial improvements and is gaining traction. But labor market dynamics need to improve to reduce unemployment sufficiently, including by further enhancing internal flexibility, reducing duality and improving active labor market policies. Policies reducing the cost (including tax cost) of employing certain groups, such as the young and low-skilled, should be considered. The labor reform should be complemented by faster progress in boosting competition and the business environment.

43. A social agreement should be explored to bring forward the employment gains from structural reforms. This could comprise: employers committing to significant employment increases (and price cuts) in return for unions agreeing to significant further wage moderation, and some fiscal incentives. The risks, however, are significant and any agreement should not stall the reform process.

44. Private sector deleveraging should be facilitated. The insolvency regime should continue to be improved, in particular, to promote early rescue of viable firms through out of court work-outs. In the future, consideration should be given to introducing a personal insolvency regime that protects payment culture and financial stability.

45. Banks also need to play their part. Losses need to be promptly recognized and distressed assets sold to avoid tying up resources. Other priorities include: continuing to reinforce the quality and quantity of capital; removing supply constraints; and implementing rigorous and regular forward-looking scenario exercises on bank resilience to guide supervisory action.

46. The required fiscal consolidation should be as gradual and growth-friendly as possible. The government's new medium-term structural targets strike a reasonable balance between reducing the deficit and supporting growth. It will be important to detail how these targets will be achieved and to ensure the measures are as growth-friendly as possible. Progress on structural fiscal reforms, such as the fiscal council and pension reform, needs to be followed through with ambitious legislation and rigorous implementation

47. It is proposed to hold the next Article IV consultation on the regular 12-month cycle.

Figure 3. Spain: Economic Activity

Figure 4. Spain: Competitiveness

Figure 5. Spain: Imbalances and Adjustment

Figure 6. Spain: Financial Market Indicators

Figure 7. Spain: Labor Markets

Figure 8. Spain: Credit conditions

Figure 9. Spain: Household's Financial Positions

Figure 10. Spain: Nonfinancial Corporates' Financial Positions

Figure 11. Spain: Balance of Payments

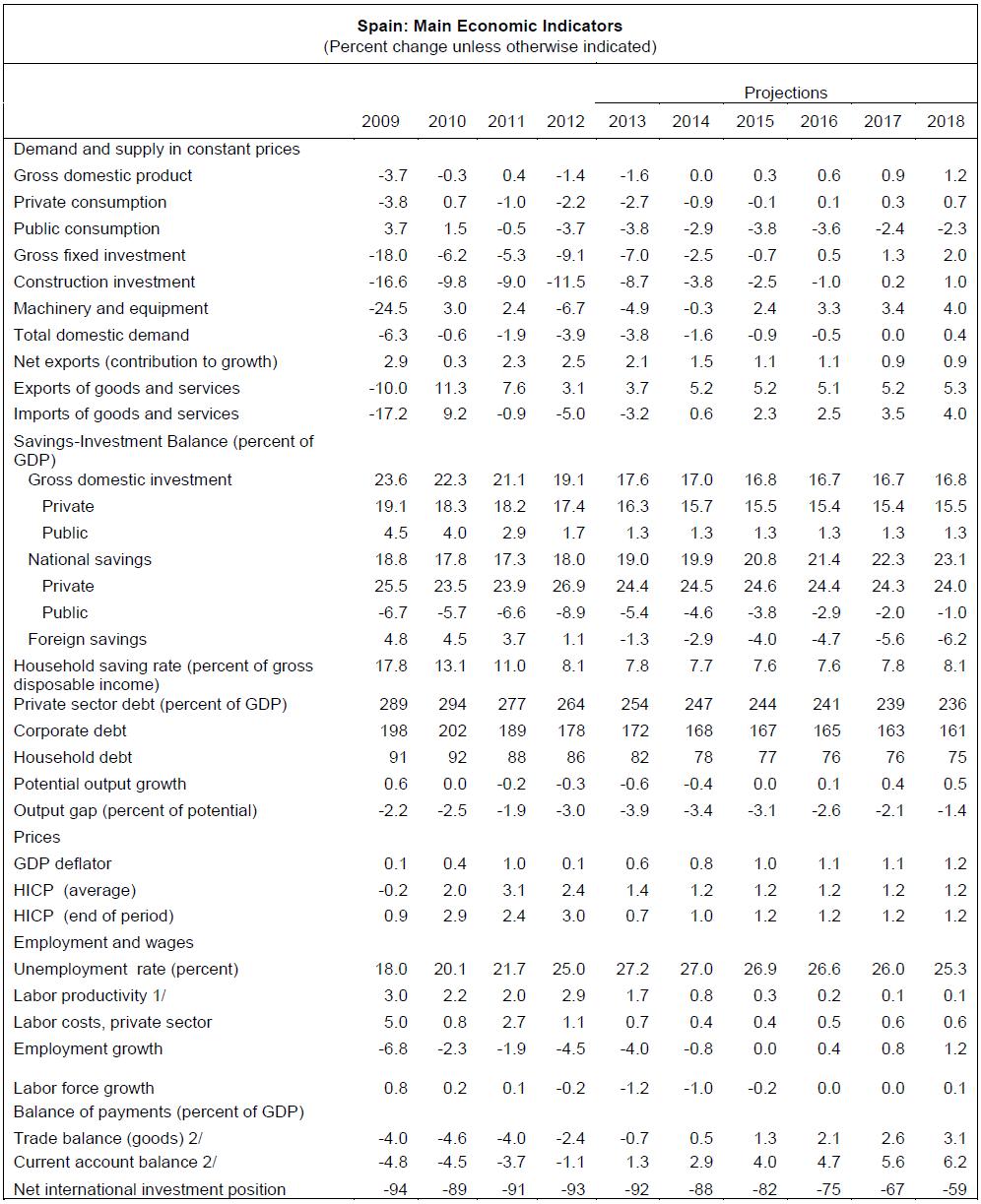

Table 1. Spain: Main Economic Indicators

Table 2. Spain: Selected Financial Soundness Indicators, 2006-2013

Table 3. General Government Operations

Table 4. General Governement Balance Sheet

Table 5. Spain: Balance of Payments

Table 6. Spain: International Investment Position, 2006-2012

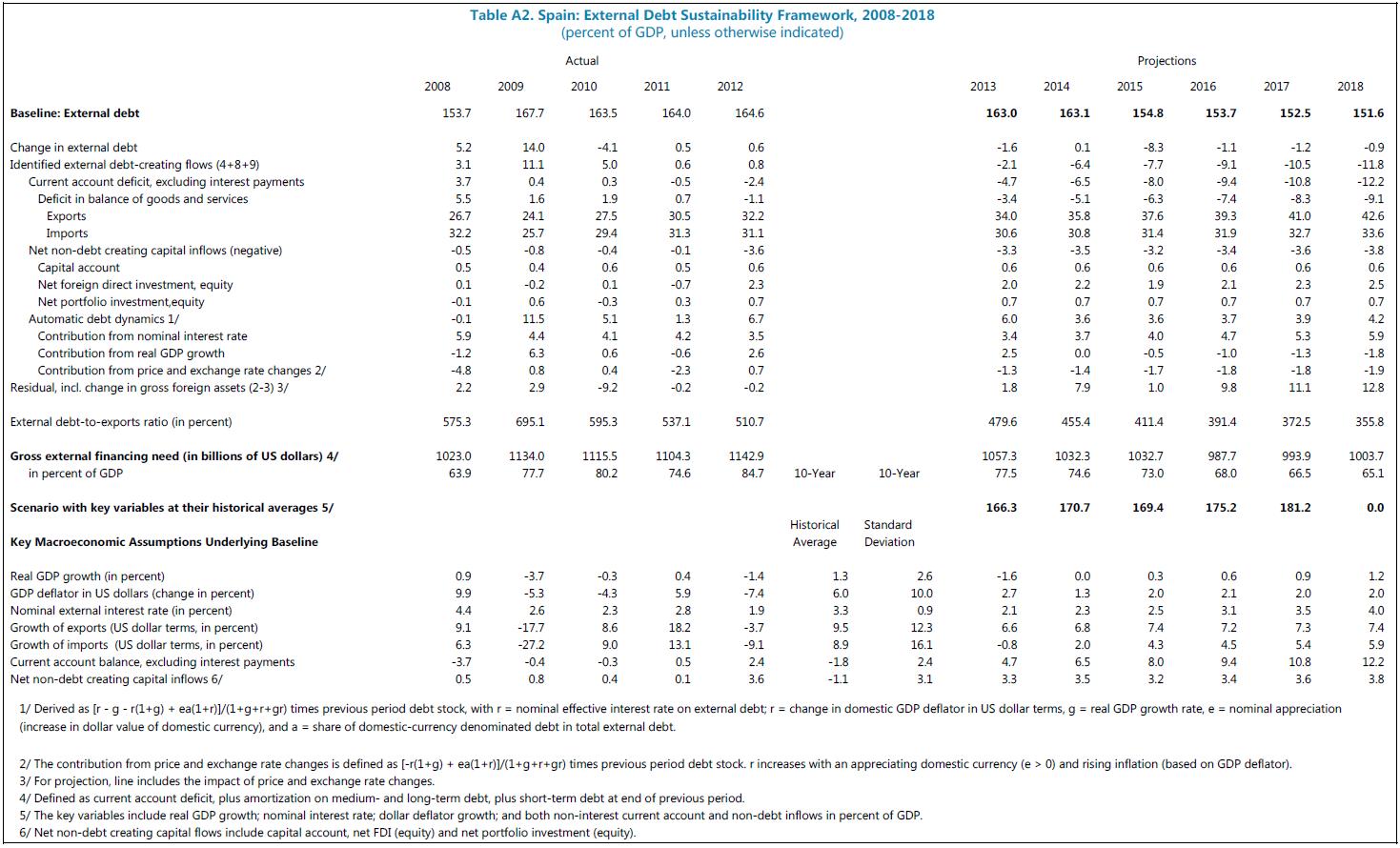

Appendix I. Debt Sustainability Analysis

Figure A1. Spain: Public Debt Sustainability: Bound Tests

Table A1. Spain: Public Sector Debt Sustainability Framework, 2006-2018

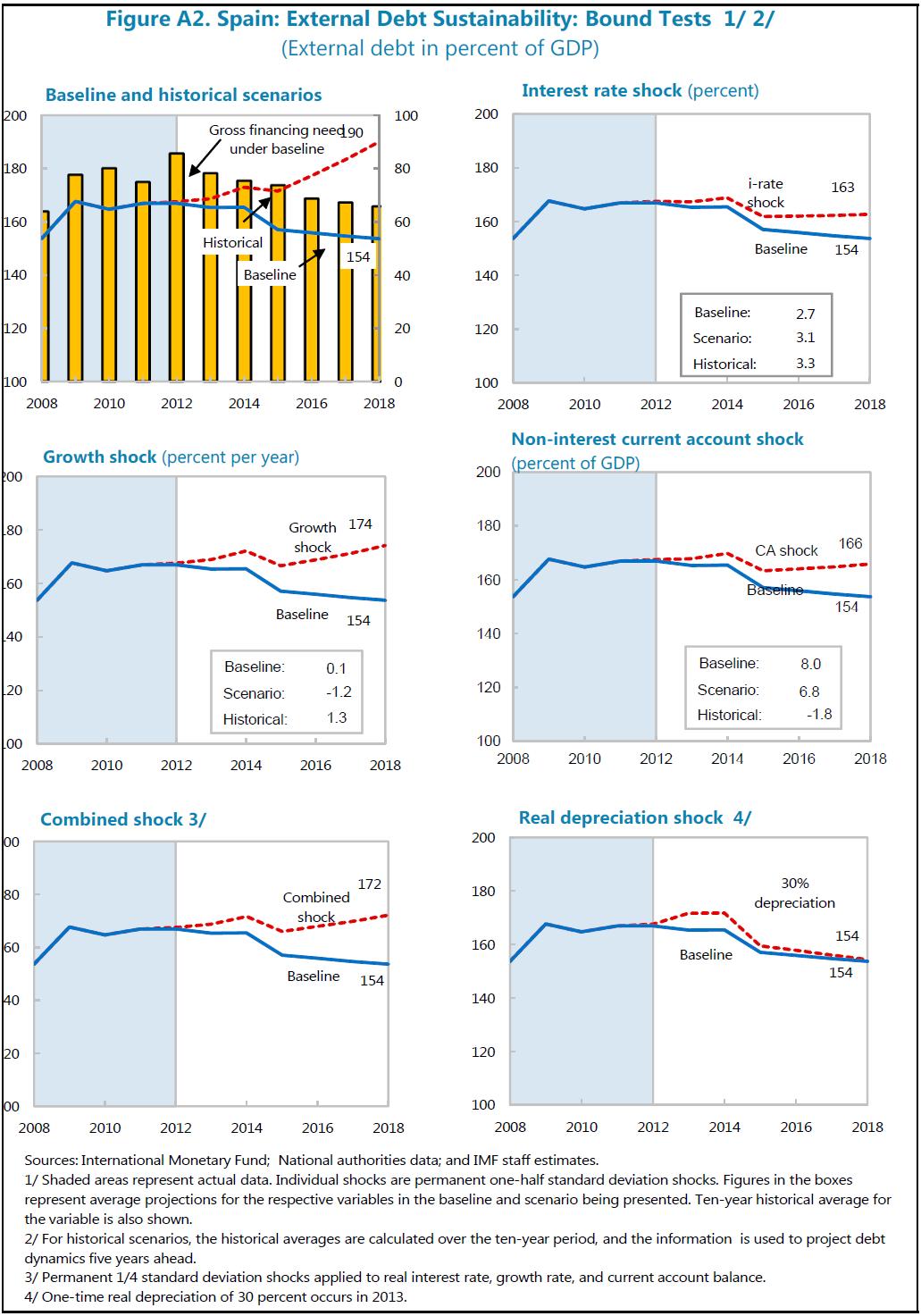

Figure A2. Spain: External Debt Sustainability: Bound Tests

Table A2. Spain: External Debt Sustainability Framework, 2008-2018

Spain: Risk Assessment Matrix

Source of Risks Relative Likelihood Impact if Realized Policy Response 1. Protracted recession High Fiscal adjustment could be a drag on growth High private sector debt could give rise to a prolonged deleveraging cycle Continued high unemployment could be self-reinforcing High Protracted recession would worsen debt outlook both for private and public sectors A longer recession could require more capital needs for the banking system Social support for reform could weaken Response at the European level to ensure accommodative financial conditions and minimize financial fragmentation Accelerate bank clean-up and private debt work-out to help restart credit. Make sure that the pace of fiscal consolidation is appropriate. Bold structural reforms to restart growth and increase employment 2. Financial stress in the euro area re-emerges Medium Market stress could be triggered by stalled or incomplete delivery of euro area policies with bank-sovereign links re-intensifying. It could also be triggered by distortions from unconventional monetary policy (e.g., side effects from exit modalities)- which is itself a global risk with "high" relative likelihood High Direct effects through financial market spillovers as well as trade links. Higher borrowing costs would complicate fiscal consolidation and private sector deleveraging Potential market tension is mitigated by the availability of the OMT Protect market access by applying for OMT European policy responses would be crucial (e.g. banking union) 3. Fiscal policy uncertainty Medium Large consolidation during the recession could have strong impact on growth in the short run Unrealistic targets could undermine fiscal efforts and credibility Medium Lack of credibility could fuel market tension Worse growth and employment could make fiscal consolidation more difficult Potential market tension is mitigated by the availability of OMT Make credible commitments to a fiscal path with well-specified measures and realistic targets 4. Structural reform slippage Medium The government may become complacent post OMT announcement Social impact of austerity could be high, with fading support for reforms High Slow structural adjustment especially in the labor market would be a drag on growth Make public commitments to key reforms with well-specified dates Pressure from Europe could also spur reform 4. Structural reform slippage Medium This could reflect lower than anticipated potential growth in Emerging Markets or capital flow reversal from a change in global risk sentiment that in turn affects Emerging Market growth Medium Spanish exports would be hurt (although the share of total exports to non-European countries is around a third, it accounts for the bulk of the growth in exports) Assist exporters to diversify their exports, especially SMEs

SPAINSTAFF REPORT FOR THE 2013 ARTICLE IV CONSULTATION--INFORMATIONAL ANNEX

Prepared By

European Department

(In Consultation with Other Departments)

CONTENTS

FUND RELATIONS

(As of May 31, 2013)Membership Status: Joined September 15, 1958.

General Resources Account: SDR Million Percent of Quota Quota 4,023.40 100.00 Fund holdings of currency 2,742.06 68.15 Reserve position in Fund 1,281.35 31.85 Lending to the Fund New Arrangements to Borrow 765.30

SDR Department: SDR Million Percent of Allocation Net cumulative allocation 2,827.56 100.00 Holdings 2,666.85 94.32 Outstanding Purchases and Loans: None

Latest Financial Arrangements: None

Projected Payments to Fund

(SDR Million; based on existing use of resources and present holdings of SDRs):

2013 2014 2015 2016 Principal Charges/Interest 0.24 0.24 0.24 0.24 Total

0.24 0.24 0.24 0.24 2013 Article IV Consultation: A staff team comprising J. Daniel (Head), K. Fletcher, P. Lopez-Murphy, P. Medas, P. Sodsriwiboon (all EUR), A. Buffa di Perrero, M. Chivakul (SPR), K. Christopherson (LEG), R. Espinoza (RES), R. Romeu (FAD) visited Madrid on June 6-19, 2013 to conduct the 2013 Article IV Consultation discussions. The mission also visited Barcelona, Sevilla, and Valencia. R. Teja (EUR) and A. Gaviria (COM) joined for the concluding meetings. F. Varela and Ms. Navarro from the Spanish Executive Director's office, joined the discussions. C. Cheptea and S. Chinta supported the mission from Headquarters. The mission met with Economy and Competitiveness Minister De Guindos, Finance and Public Administrations Minister Montoro, Bank of Spain Governor Linde, other senior officials, and financial, industry, academic, parliament, and trade union representatives. The concluding statement was published and the staff report is expected to be published as well. Spain is on a standard 12-month cycle. The last Article IV consultation discussions were concluded on July 22, 2011 (EBM/11/81-1). A Financial Sector Assessment Program (FSAP) Update was conducted in two missions (February 1-21 and April 12-25, 2012). On June 8, 2012, the FSAP discussions were concluded and the documents published.

Exchange Rate Arrangements and Restrictions: Spain's currency is the euro, which floats freely and independently against other currencies. Spain has accepted the obligations of Article VIII, Sections 2, 3, and 4, and maintains an exchange rate system free of restrictions on payments and transfers for current international transactions, other than restrictions notified to the Fund under Decision No. 144 (52/51).

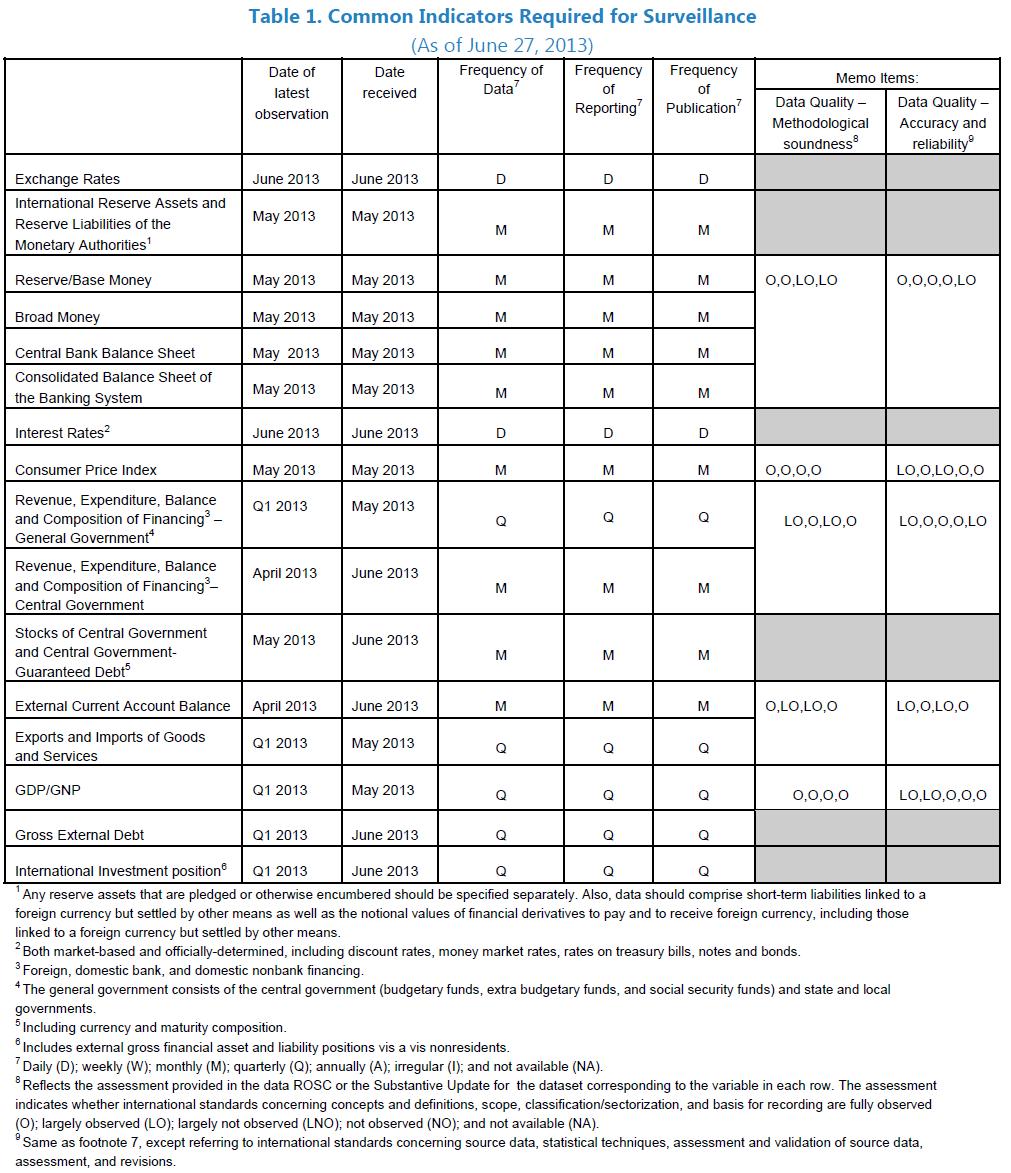

STATISTICAL ISSUES

(As of June 27, 2013)

I. Assessment of Data Adequacy for Surveillance

General: Data provision is adequate for surveillance.

II. Data Standards and Quality

Subscriber to the Fund's Special Data

Dissemination Standard (SDDS) since

September 1996.No data ROSC available. Table 1. Common Indicators Required for Surveillance

Press Release No. 13/292 International Monetary Fund FOR IMMEDIATE RELEASE Washington, DC 20431 USA August 2, 2013 IMF Executive Board Concludes 2013 Article IV Consultation with Spain On July 26, 2013, the Executive Board of the International Monetary Fund (IMF) concluded the Article IV consultation with Spain. |1|

The Spanish economy accumulated large imbalances during the long boom that ended with the global financial crisis. Unemployment soared, the fiscal position deteriorated sharply, and funding conditions tightened for both the public and private sectors.

Key imbalances are correcting rapidly. Sovereign yields fell sharply since the European Central Bank's announcements about Outright Monetary Transactions (OMT), the current account swung into surplus, the fiscal deficit fell sharply in 2012 despite the recession, private sector debt declined, and the banking system is stronger. But the adjustment process is proving slow and difficult. Growth has been negative in the last seven quarters, unemployment has reached unacceptably high levels, and financing conditions remain tight for small firms.

The reform process has accelerated and deepened. Decisive reforms in the labor, financial, and fiscal sectors, in line with past staff recommendations, is helping stabilize the economy. Determined action has been taken to help clean up banks in the context of a financial sector program from the European Stability Mechanism, for which the IMF is providing technical assistance. Provisions and capital were greatly increased following an independent stress test and asset quality review in summer 2012. Weak banks are being restructured and much of their real estate assets have been transferred to an asset management company (SAREB). Regulation and supervision was also enhanced.

Fiscal frameworks and transparency have been substantially upgraded. An independent council is being introduced and a commission of experts has issued a proposal to ensure pension system sustainability. Early and partial retirement rules were further tightened. Monthly reports are now available for all major levels of government.

On labor market policy, a major reform was instituted in July 2012 to improve firms' ability to adjust working conditions (including wages), reduce duality, and promote job matching and training. Unemployment insurance was reduced by 17 percent after 6 months of benefits, and hiring subsidies were reformed. In February 2013, the government announced more flexible hiring arrangements for youth and tax incentives to support youth employment and entrepreneurship.

Product and service market reforms are underway. The government liberalized the establishment of small retail stores and retail business hours. Further reforms have been announced to remove regulations that fragment the domestic market, to liberalize professional services, and to foster entrepreneurship.

Executive Board Assessment

Executive Directors commended the authorities for strong progress on critical reforms amid challenging conditions, which is helping to stabilize the economy. External and fiscal imbalances are correcting rapidly. However the economy remains in recession, with unacceptably high unemployment, and the outlook remains difficult. Directors stressed the need for decisive further action to generate growth and jobs, both by Spain and Europe, and continued strong commitment to the reform effort.

Directors welcomed the 2012 labor market reform, which appears to be gradually delivering results. However, they underscored that labor market dynamics need to improve further in order to reduce unemployment sufficiently, including by enhancing internal flexibility, reducing duality, and improving active labor market policies. Many Directors generally saw merit in exploring a social agreement between unions and employers to bring forward the employment gains from structural reforms, while they noted that it would be difficult to achieve. However, such an agreement should not delay the needed structural reforms. Directors also underscored the need to improve the business environment and boost competition, including through product and service markets reform. They looked forward to timely implementation of the plans envisaged under the National Reform Program.

Directors welcomed the authorities' commitment to fiscal consolidation and agreed that the new medium-term structural targets strike a reasonable balance between reducing the deficit and supporting growth in the short term. They encouraged the authorities to specify how the targets will be achieved and to ensure that the measures are as growth-friendly as possible. In this context, they looked forward to the tax and expenditure reviews. A number of Directors also recommended flexibility in meeting the targets should growth disappoint. Directors welcomed progress on structural fiscal reforms, such as the fiscal council, and highlighted the need to follow through with ambitious legislation and rigorous implementation. Many Directors also looked forward to further progress on developing the enforcement of the Organic Budget Stability Law, and securing the sustainability of the pension system.

Directors stressed the importance of facilitating private sector deleveraging. The insolvency regime should continue to be improved. A number of Directors encouraged the authorities to consider in the future introducing a personal insolvency regime. Directors highlighted that banks also need to play their part by promptly recognizing losses and selling distressed assets. They welcomed the progress made in the clean-up of the financial system but stressed the need to remain vigilant to risks to financial stability and to protect the hard-won solvency. Priority should be given to removing supply constraints, supporting access to credit to small and medium enterprises , implementing scenario exercises on bank resilience to guide supervisory action, and determining, in the context of the forthcoming European balance sheet review, any needs for further capital reinforcement. Directors stressed that actions at the European level, including initiatives aimed at improving monetary transmission, reversing financial fragmentation, and making progress toward a banking union are essential to support Spain's adjustment effort.

Spain: Main Economic Indicators

(continued)

Statement by Mr. Fernando Varela, Alternative Executive Director for Spain

July 26, 2013At the outset, I would like to thank staff for their candid exchange of views with the authorities, their comprehensive mission and the useful staff Report and Selected Issues paper.

Since last year's consultations, and thanks to the implementation of decisive policy actions both by the Spanish government and at the European level, the Spanish economic situation has markedly improved. However, important challenges remain ahead, particularly the high unemployment rate, which is the first and foremost concern of the government. The economy will continue in recession in 2013, but recent positive developments are clearly signaling that Spain is in a turning point in the economic cycle. By the end of this year, the growth rate will be positive and it will gradually increase throughout next year. The main task ahead to ensure that these encouraging signs of stabilization are followed by a prompt, strong and durable recovery, capable of reducing in a sustainable manner the significant imbalances accumulated during the boom years and since the beginning of the crisis. The government is fully committed with its policy agenda and is sparing no effort to that end.

In line with IMF's advice, the government's economic strategy aims at fostering growth and creating jobs and it is based on three main pillars: a fiscal consolidation effort in order to ensure a sustainable public debt level; a profound financial sector reform directed at restructuring and reinforcing financial institutions; and a comprehensive set of structural reforms to increase flexibility and competitiveness in the economy and lay the foundations for higher and more balanced future growth .

The forceful implementation of this strategy is starting to bear fruit. The main underlying imbalances are correcting rapidly. The fiscal deficit is being reduced and the current account deficit has turned into a surplus, while the net IIP has started a diminishing trend and productivity and competiveness have strongly improved. The banking system is now much stronger and resilient. However, further efforts are needed to continue correcting the remaining imbalances, especially private sector delivering and unemployment.

Economic Outlook

Growth in 2013 will still be negative, with a government forecasted rate of -1.3. Nevertheless, there are positive signs indicating that the economy will stabilize in the second part of the year. The main leading indicators point in that direction. The June PMI results for the industrial sector and for services have been 50.0 (up 1.9 points) and 47.8 (up 0.5), respectively, a level not seen since 2010. The OECD Composite Leading Indicator was 101.6 in May (up 0.3), an increase not seen since 2008. Retail sale indicators and business values indexes also support this view. According to Bank of Spain's provisional data, q-o-q GDP growth in 2Q 2013 has been -0.1 percent, which also confirms this trend.

Consistently with this information, the government believes the projected growth rate for 2013 is prudent and within reach, and it is forecasting a positive 0.5 percent in 2014. The 2014 projection is based on a less negative contribution of domestic demand and a significant positive contribution from the external sector, taking also into account that the fiscal drag will be smaller than anticipated. The consensus forecast for 2014, among independent domestic analysts, is 0.7 and 0.3 percent if foreign analysts are included.

Going forward, stronger growth in the world economy, and particularly in the EU, coupled with persistent stability in the financial markets, will go a long way for ensuring a swifter and more solid recovery in Spain.

It is also worth highlighting the improvement in competitiveness and good performance of the external sector. In this sense, the current account adjustment has been very remarkable, with the deficit falling to 0.8 percent of GDP in 2012, from a peak of 10 percent in 2007and it t is expected to turn into a surplus of around 2 percent in 2013. Most of this correction is due to structural factors and cyclically adjusted analysis shows that it is going to continue in the future. The outstanding performance of exports has been the main driver of this improvement. Spanish export-market shares have been very resilient, despite a very difficult international context and strong competition from emerging market countries. Export competitiveness has been strongly driven by non-price competitiveness and geographic and product diversification, together with improving price competitiveness. Spain has now a trade surplus with the EU and some of its more important EU trading partners, while exports have also been diversified towards other dynamic markets.

Unit Labor Costs (ULC) have been falling significantly in past years, with their improvement intensifying in 2012 thanks to productivity gains and wage moderation. In terms of ULC, the loss of competitiveness accumulated since 2004 was already corrected in 2012.

On prices, the inflation rate has been affected by fiscal adjustment, but it is expected to decrease substantially as the effects of the VAT and certain regulated prices increase fades away. Headline inflation stood at 1.7 percent in Q2, but it will decelerate during the second half of the year to end up around 1 percent below EU average.

Confidence has also improved, as reflected in the significant reduction in Treasury yields and the fact that more that 70 percent of funding needs for this year have been already covered.

Fiscal policy

The Government is strongly committed to fiscal consolidation in order to make fiscal finances sustainable in the medium term. As a sign of this commitment, a major coordinated effort within all Public Administrations was made in 2012 to reduce the public deficit. In a year in which activity contracted by 1.4 percent, the deficit (net of one-offs related to the support of financial institutions) was cut 2 percentage points of GDP (from 9 to 7 percent). The intensity of the fiscal effort was among the highest in advanced economies, as highlighted in April 2013 Fiscal Monitor.

A wide number of tax and expenditure measures have been adopted to support fiscal consolidation in 2012 and 2013 amounting to 4.2 percent of GDP in 2012 and 3.5 percent in 2013. Its distribution between the expenditure and revenue sides has been well-balanced, with around 55 percent in expenditure reductions. All public expenditures have declined, except interest payments and social benefits, which have been driven by debt and labor market trends. Public employment has also been reduced by around 375,000 persons between 3Q2011 and 1Q2013. Steps have also been taken to increase indirect tax collection, with measures to increase VAT rates and broaden its base--Spain was the EU country with the highest increase in the average VAT rate in the EU in 2010-13--but also affecting excise duties and environmental taxes. This has led to some shift of the relative tax burden towards indirect taxes. The Government is committed to continue consolidation in the most growth-friendly manner possible.

For the period 2013-16, following the recommendations made by the Council of the European Union and in line with staffs advice, the targets both for fiscal deficit and public debt have been modified to better adapt the adjustment pace to the current circumstances of the Spanish economy and to mitigate the downdraft of the consolidation measures on growth. The deadline to bring the deficit below 3 percent of GDP has been extended by two years. The deficit target for 2013 has been set at 6.5 percent of GDP (instead of the previous 6.3 percent). Despite the easing of the adjustment path, the fiscal effort will continue to be very significant, requiring a cumulative structural effort of 3.9 percent of GDP in the years 201316.

Consolidation efforts continue to yield results. The latest budget execution data published on 15 July 2013 points out that the deficit target will be met, evidenced by significant improvements recorded in all subsectors. In May 2013, the cumulative deficit and primary deficit of the Central Government were 6.5 and 14 percent, respectively, lower than the previous year. In the same period, the Autonomous Regions recorded an aggregated deficit of 0.43 percent of GDP, in line with their annual target of 1.3 percent of GDP.