| Information |  | |

Derechos | Equipo Nizkor

| ||

| Information | | |

Derechos | Equipo Nizkor

| ||

13May13

U.S.-Chinese Motor Vehicle Trade: Overview and Issues

Contents

The Chinese Motor Vehicle Industry

Profile of Chinese Auto Assembly

U.S.-China Trade Disputes over Vehicles and Parts

The Chinese Auto Parts SectorChinese Exports and Imports

Chinese Acquisitions of U.S. Auto Parts Makers

The Auto Industry in China's Five-Year Plan Process

Global Parts Competition IncreasesChina's WTO Accession

The 2005 U.S. WTO Case Against China on Auto Parts

U.S. Safeguard Measures on Chinese Tires

Rare Earth Elements

The U.S. WTO Case Against China on Auto and Auto Parts Subsidies

New Energy VehiclesFigures

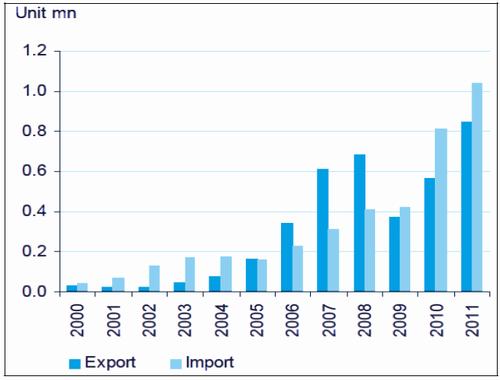

Figure 1. Chinese Vehicle Imports and Exports

Tables

Table 1. 10 Most Popular Makes in China

Table 2. U. S. Auto Parts: Exports and Imports

Table A-1. 10 Largest North American Auto Parts Suppliers, 1999 vs. 2011Appendixes

Appendix. Largest North American Auto Parts Suppliers

Summary

The U.S. auto industry employs nearly 800,000 workers and is a major employer in certain parts of the country. International competition is fierce, with many automakers and thousands of parts makers vying for market share. Because of the industry's importance to the U.S. economy, the rapid rise of China's auto assembly and auto parts industries in recent years has raised concerns among some Members of Congress.

In 2009, China overtook the United States to become both the world's largest producer of and market for motor vehicles. In 2012, assemblers in China sold 19 million vehicles, and forecasts project more than 30 million vehicles will be sold there in 2020. China's increasing importance in this industry presents a unique set of opportunities and challenges for the United States. On the one hand, China is in some respects a relatively open market; it was the fourth-largest export market for U.S. autos and auto parts in 2012 at $7.3 billion ($5.7 billion for autos and $1.6 billion for auto parts), and has welcomed foreign direct investment by U.S.-based auto and auto parts manufacturers. Every year since 2010, General Motors has sold more cars in China (through exports and its joint ventures there) than in the United States.

On the other hand, China maintains a number of trade and investment barriers that affect trade flows in autos and auto parts. Foreign automakers can produce autos in China only through 50/50 joint ventures with Chinese partners. In addition, U.S. and other foreign auto firms have reportedly faced pressures relating to transfer of technology, export performance, and domestic content requirements. Although the United States imports few vehicles from China, China has become the fourth-largest source of U.S. auto parts imports, with shipments of $14.5 billion in 2012.

The Chinese government has made the development of its auto and auto parts industries, including "new energy vehicles," a major economic priority, and has implemented a number of industrial policies to promote and protect Chinese auto firms with the long-term goal of making them globally competitive. As a result, auto and auto parts trade has become a source of conflict between the United States and China, most recently in 2012, when the Obama Administration asked the World Trade Organization (WTO) to consider whether alleged Chinese subsidies of auto and auto parts manufacturers violate international rules.

China's demand for motor vehicles is likely to continue growing rapidly because its population of 1.3 billion is just beginning to have the financial resources to purchase automobiles. For the United States, this will mean many new opportunities and challenges. Unlike some other markets, such as Korea, China's large internal demand may well shape the industry for many years, with exporting a secondary interest. China's rising investments in U.S. parts makers such as Nexteer and B456 Systems may help develop a U.S. technology lead in fuel-efficient, low-emission vehicles. But the prevalence of state and municipal ownership of many Chinese auto and auto parts companies may also cause friction. Many in Congress have called on the Obama Administration to take a tougher stand against China's industrial policies that may favor Chinese automakers over foreign automakers.

The U.S. auto industry is of interest to many in Congress because of its large employment, economic impact, and geographic reach. Around the world, there are many automakers and thousands of parts suppliers, leading to intense international competition. Through the 2009 stimulus bill |1| and financial support for General Motors, Chrysler, and their suppliers, the recovery of the domestic auto industry has been made a national priority. The federal government has also provided loans and grants for electric vehicle manufacturing operations, |2| research and development support for new electric, fuel cell, and natural gas vehicles, and federal tax credits for purchase of hybrid and electric vehicles.

In addition to steps supporting the domestic auto industry, Congress and the Office of the U.S. Trade Representative (USTR) have taken an interest in foreign trade and investment practices that adversely affect U.S. automakers. For example, the emergence of Japan's auto industry as a major global competitor in the 1980s and 1990s led to frequent conflict with the United States, as many U.S. policymakers argued that Japan's trade policies harmed U.S. domestic auto and auto parts producers at home and abroad. |3| Trade in autos and auto parts was one of the most contentious issues in negotiating the U.S.-South Korea free trade agreement, which went into effect in 2012. |4|

The rapid rise of China's auto and auto parts industries in recent years has raised similar concerns and led to questions about some of the trade practices employed by the Chinese government. Some in Congress have called on the Obama Administration to take a tougher stand against China's industrial policies and other measures that may be distorting trade, including by making greater use of the World Trade Organization (WTO) dispute settlement process to challenge Chinese policies that may violate WTO rules.

This report examines the rise of China's auto and auto parts industries, Chinese government policies to promote these industries, trends in U.S.-China trade in autos and parts, auto-related trade disputes, and implications for U.S.-China commercial relations.

The Chinese Motor Vehicle Industry

In the past five years, rising incomes and central government stimulus have made China into the world's largest auto market, in terms of both production and unit sales of vehicles. |5| China's annual output of cars and light trucks increased from less than 9 million units in 2007 to more than 19 million in 2012, largely destined for domestic consumption. By comparison, in the United States, just over 10 million vehicles were produced in 2012. |6|

Profile of Chinese Auto Assembly

Sales are expected to continue rising, as China's ownership rate of 58 motor vehicles per 1,000 people is half the global average of 175 per 1,000 people |7| and well below the U.S. rate of 797 per 1,000 people. A major project under way to build a network similar to the U.S. Interstate Highway system may also support sales growth. It has been forecast that as many as 30 million vehicles will be sold annually in China by 2020, with most of them being produced there. |8| Chinese production capacity is expanding even faster than demand, resulting in a drop in average vehicle prices at a time when personal income is on the rise.

The transformation of China's auto industry has been a central government goal since the 1980s, when American Motors Corp. |9| signed the first joint venture agreement to produce Jeeps in China. |10| At that time, there were a large number of local Chinese automakers, but the government reasoned that its domestic manufacturers would not reach higher quality, technology, and management standards without assistance from foreign automakers. Foreign automakers were allowed to produce vehicles in China, but only through joint ventures in which local partners have at least 50% control. Some of these partners are controlled by local or provincial governments. Thus, SAIC Motor Corp. (formerly Shanghai Automotive Industry Corp.) |11| has joint carmaking ventures with both Volkswagen AG (VW) and General Motors Co. (GM), while GM also makes cars in China in partnership with Wuling Automobile Co. |12|

Such joint ventures between foreign companies and Chinese partners produce about 70% of new passenger cars sold in China. |13| GM and VW are the leading non-Chinese automakers, and China is also the biggest market (in terms of number of cars sold) in their respective global portfolios.

GM now sells more cars in China than in the United States. |14| Ford Motor Co. is a more recent entrant, and has about 3% of the market. |15| Chrysler does not currently build cars in China but reportedly plans Jeep production there in the near future. |16|

In addition to the joint ventures, Chinese firms such as Chery, FAW, and Dongfeng make vehicles for sale under their own brands. Table 1 shows the largest makes of vehicles--whether built in China or imported--by unit sales in 2012, including vehicles made in joint ventures. |17|

Table 1. 10 Most Popular Makes in China

Unit Sales

Company

2012 Vehicle Sales

General Motors 2,821,720 Volkswagen 2,608,896 Hyundai-Kia 1,367,303 Dongfeng 981,419 Nissan 778,793 Toyota 751,317 First Automotive Works (FAW) 739,318 Honda 627,610 Great Wall Zhonxing 624,602 Chery 563,305 Source: Ward's Automotive Database, released February 2013.

Note: Includes passenger cars; sport utility vehicles; light, medium and heavy trucks.China became a net exporter of vehicles in 2005, when it sold more than 172,000 units abroad. It retained that status, though, for only four years; since 2009, it has again been a net importer. In 2011, as shown in Figure 1, it exported nearly 850,000 units, of which 56% were passenger cars and 44% commercial vehicles. |18| About 70% of the vehicle exports are manufactured by domestic Chinese companies such as Geely and Chery, with the remainder by foreign-Chinese joint ventures. The main destinations for these vehicles are developing markets in South America, Africa, and the Middle East. Chinese vehicle exports accounted for about 4.5% of total output in 2011, |19| a far smaller share than in some other auto-producing nations. |20|

The only Chinese-made vehicles now exported to the United States are small trucks and off-road vans such as the Wuling Minimax. |21| Honda's Chinese-made FIT subcompact is exported to Canada, but is not sold in the United States. |22| While there have been reports of plans to build passenger cars in China for export to the United States, none of these plans has yet come to fruition. |23|

Figure I. Chinese Vehicle Imports and Exports

2000-2011, in Millions of Units

Source: BBVA Research, Automobile Market Outlook: China, Hong Kong, June 19, 2012, p. 4.

As also shown in Figure 1, Chinese vehicle imports have risen, too, from just under 228,000 units in 2006 to over a million in 2011; in the latter year, 58% of imports were sport utility vehicles (SUVs). |24| Most of the imported vehicles are in the luxury segment. |25| The major countries of origin were Germany (28% of the Chinese import market), Japan (24%), United States (12%), United Kingdom (6%), and South Korea (4%). |26| Among luxury brands, BMW and Mercedes-Benz top the list. In addition to having a greater range of luxury vehicles in their fleets, European makers do well because the substantial Chinese consumption tax on cars with large engines falls more heavily on American-made vehicles. |27|

The United States exported many more vehicles to China in 2011 than China exported to the United States. In both 2011 and 2012, China was fourth-largest export market for U.S. vehicles, behind Canada, Mexico, and Germany. |28|

With the rapid growth of the Chinese auto sector has come rising demand for the thousands of auto parts that are combined into final product motor vehicles. The Chinese parts industry is fragmented and comprises both Chinese and foreign parts makers, including many U.S.-based companies.

A 2011 U.S. Commerce Department report on auto parts trade with China summarized the foreign investment trend:

In 2000, the majority of indigenous Chinese [auto parts] suppliers were uncompetitive and produced low quality products. International automakers helped spur foreign supplier investment in China over the past decade which made those rising exports possible by pressuring their international suppliers to locate production there. The automakers did so in an effort to hold down costs and maintain their own competitiveness both in China and in markets like the United States. Thus, many U.S. and other international auto parts companies opened plants and expanded their Chinese production in order to supply the international automakers' Chinese joint ventures, and to use their operations in China to export to the global automotive OE [original equipment] and aftermarket, including the United States. In the process, some have also become suppliers to domestic Chinese automakers, which have [sic] helped improve the product quality of these firms. |29|

China's exports of auto parts grew from $7.4 billion in 2002 to more than $69 billion in 2011, a nine-fold increase. |30| According to U.S. government data, about 25% of China's auto parts production is exported, including to the United States, where more than $14 billion in parts from China were imported in 2012, a 60% increase since 2008. |31| As discussed later in this report, some U.S. producers and the U.S. government have alleged that many auto parts exports are subsidized in ways that violate WTO rules.

The U.S. parts market comprises both parts destined for assembly plants and aftermarket sales, with sales to automakers the larger of the two markets. According to the U.S. Department of Commerce, about two-thirds of parts sold domestically are sourced from suppliers located in the United States. |32| Customs import data do not break down the destination of auto parts, so it is not known how many Chinese parts flow to the automakers and how many to the aftermarket. Some analysts believe that most of the imports are for aftermarket use. |33| One analysis, however, searched the U.S. government's Automated Manifest System (AMS) |34| and found that in 2010 and 2011 the Detroit 3 imported not only relatively simple auto parts from China, such as knobs, lights, rearview mirrors, and exhaust manifolds, but also more sophisticated products such as transmission electro-hydraulic control modules and control resistors. |35|

It is possible that some Chinese parts might be incorporated into more complex components, such as transmissions, at U.S., Mexican, or Canadian plants. However, no Chinese-made engines and only a single model of Chinese-made transmission, the manual transmission offered on the Ford Mustang, were installed on cars built at U.S. assembly plants in 2012. |36|

China's most recent Five Year Plan, discussed later in this report, emphasizes production of "new energy vehicles," such as electric and fuel cell cars. Toward this end, the plan identifies electric vehicle batteries, electric motors, sensors, and electronic fuel cells as particularly important. Should China develop exports of such products, they would compete directly with more sophisticated parts manufacturing in other industrialized countries.

China is also a major importer of auto parts. In 2010, China imported about $27 billion in transmissions, engine parts, car bodies, and accessories and electronics. These goods were sourced primarily from Japan, Germany, South Korea, France, and the United States. |37| U.S. parts plants exported about $1.6 billion in auto parts to China in 2012. |38|

The Economic Policy Institute, a Washington think tank close to the U.S. labor movement, has estimated that there were upwards of 10,000 registered auto parts companies in 2008 in China (more than double the number in 2002) and another 15,000 nonregistered companies that had some portion of their business in auto parts. |39| By contrast, there are about 5,600 U.S. parts suppliers operating in the United States. |40| The Chinese government does not have the same strictures on investment in the auto parts sector as in auto assembly, so foreign auto parts companies can own more than 50% of a Chinese parts maker. Many U.S.-based parts producers have established operations there. Seven of China's 10 largest parts manufacturers are foreign-based, according to an analysis by a Washington consulting firm. |41|

Among Tier 1 auto suppliers--the companies that furnish entire assemblies, such as braking systems and seating systems--U.S.-based companies Delphi, Visteon, Johnson Controls, Lear, Arvin Meritor, and TRW manufacture in China, along with other leading producers such as Bosch, Denso, Magna, and Yazaki. Michigan-based Visteon, for example, has 23 manufacturing, technical, and customer centers in China to provide vehicle climate equipment, electronics, and interiors, and its Asia-Pacific regional operations are based in Shanghai. (Visteon has 11 such centers in North America.) TRW has forecast that China could become its largest single market by 2020. |42|

Chinese Acquisitions of U.S. Auto Parts Makers

China's auto parts sector is also being bolstered through the acquisition of assets of foreign auto parts makers. Through such purchases, Chinese parts makers can target technology and product innovations to enhance their Chinese operations. In addition, acquisitions may help the Chinese companies develop the expertise to shift from supplying low-margin parts to more profitable activities, such as integrating parts into component systems.

Among the Chinese investments in recent years were the following:

- Beijing West Industries (BWI), a joint venture of two Chinese state-owned enterprises, bought the suspension and brake units of Delphi Corp. in 2009 for about $100 million as Delphi was emerging from bankruptcy and shedding assets. |43| BWI operates former Delphi plants in Ohio and Michigan that make components for Chevrolet, Audi, and other automakers.

- Pacific Century Motors (PCM), a joint venture between the Beijing municipal government and another Chinese partner, bought Nexteer Automotive from GM in 2010. |44| Nexteer's plant in Saginaw, MI, builds electronic steering assemblies for GM pickups and SUVs. Nexteer has 22 manufacturing facilities, 6 engineering facilities, and 14 customer support centers in the United States and other countries. The reported $450 million sale is the largest Chinese acquisition of a U.S. auto parts company. |45|

- The Chinese conglomerate Wanxiang outbid Johnson Controls and several other bidders to win control of lithium-ion battery maker A123 Systems, |46| which filed for bankruptcy in 2012. The Chinese company's $257 million bid enabled it to take control of the commercial parts of A123 Systems after the Committee on Foreign Investment in the United States (CFIUS) approved. |47| The deal initially raised questions in Congress because A123 Systems was awarded $249 million in stimulus funding in 2009. |48| At the time of the transaction, Wanxiang already had bought other U.S. auto parts companies and had over 3,000 U.S. employees.

The Auto Industry in China's Five-Year Plan Process

The Chinese government has an ambitious plan to transform its auto manufacturing sector, which was designated a national "pillar industry" in China's Seventh Five-Year Plan in 1986. |49| In 1994, the "Formal Policy on Development of Automotive Industry" was issued by the State Council to further advance the industry, while imposing tariffs to restrict imports. Stewart and Stewart, a Washington law firm that often represents U.S. manufacturers in trade cases, claims that the 11th Five-Year Plan (2006-2010) targeted specific components for priority support and provided an estimated RMB 4.7 billion (about $760 million) to support research and development for energy-efficient vehicles, allegedly through reduced corporate income tax rates, subsidized export credits, and concessional financing by state-owned banks. In 2009, the Chinese government's "Automotive Industry Restructuring and Revitalization Plan" sought to boost domestic vehicle consumption and set as a target the expansion of indigenous vehicle and parts production, especially of hybrid and electric cars. |50|

In its 12th Five-Year Plan (2011-2015), China laid out three major steps |51| to further build up the auto assembly and parts industry:

- consolidation of the currently fragmented industry, which would reduce the number of auto making and auto parts firms and, in so doing, could create economies of scale, reduce manufacturing costs, and raise the industry's international competitiveness;

- emphasis on bolstering research and development for key auto parts, which could enhance Chinese-owned firms' innovation and productivity and help raise the quality of Chinese-made vehicles and parts; and

- incentives for production and sale of energy-saving vehicles, which could help reduce dependence on imported oil, cut emissions, and usher in a significant rise in technological knowledge that would benefit the indigenous vehicle sector.

General Motors and Electric Vehicle Technology in China The Chinese government's priorities for advancing its new-energy vehicle program were evident in its recent discussions with GM. Chinese consumers bought over a million imported vehicles in 201 1, most of them luxury cars. General Motors would like to sell its Volt extended range electric vehicle there, exported from the United States. In 2011, the Chinese government reportedly told GM that to be able to sell that vehicle in China and also take advantage of Chinese tax incentives, GM would have to provide details of its unique battery technology, electronics, and drivetrain. GM's Chairman and CEO, Daniel Akerson, reportedly declined to divulge such proprietary information, thereby preventing Chinese consumers from using a $19,000 subsidy to purchase the vehicle, likely crimping sales. |52| (The Volt sells for upwards of $40,000 in the United States.) While GM also announced in 2011 that it would work with its partner SAIC Motor to develop a "new electric vehicle architecture" in China, |53| these plans reportedly did not work out and in May 2013, the head of GM China said the companies would go their separate ways. Differing technology platforms and suppliers were reportedly behind the change. |54|

"New-energy automobiles" is one of the seven "strategic and emerging" industries (SEIs) emphasized in the 12th Five-Year Plan. Together, the seven SEIs, which represented 3% of GDP in 2011, are forecast to comprise 8% of GDP by 2015 and 15% by 2020. |55| The Chinese government aims to achieve these goals through the use of "support by treasury, tax and financial policies," including financing, credit support and central government investment, building on the support provided in the 11th Five-Year Plan. |56| In addition, some Chinese provinces and cities have their own incentives and support programs for the auto industry. |57|

Several parts of the 12th Five-Year Plan have generated charges that China is violating some of its WTO obligations in its support for the industry. Parts of its energy-saving vehicle program are alleged to violate the WTO with new local content, technology transfer, and export requirements. |58|

As discussed later in this report, the Obama Administration has notified China that it will take these and other subsidy issues to the WTO if the Chinese government does not modify its policies.

Global Parts Competition Increases

A typical automobile is made from upwards of 15,000 parts, from engines and transmissions down to tiny electronic sensors, dashboard components, tires, and windshield wiper motors. While vehicle manufacturers at one time made nearly all these parts, major automakers now buy from parts suppliers as much as 70% of the value added in production of motor vehicles. A large network of independent producers is responsible for designing and producing these parts used by the automakers and integrating parts into more complex assemblies, such as a complete dashboard or steering mechanism.

There are several types of parts manufacturers. Tier 1 manufacturers make components and systems for new vehicles. They often use parts furnished by Tier 2 and 3 suppliers, smaller companies that may focus on particular types of products, such as gaskets or valves. While Tier 2 and 3 suppliers sometimes sell directly to automakers, in many cases their main customers are the repair shops and auto supply stores that make up the aftermarket. Tier 2 and 3 suppliers often sell into the new vehicle market through the Tier 1 suppliers, which use their parts in larger assemblies, rather than through direct relationships with automakers. Many Tier 1 manufacturers also build for the aftermarket. Of the total U.S. parts market, an estimated 70% of the value originates with Tier 1 suppliers.

Around the world, a change in manufacturing and design processes is favoring a consolidation among vehicle suppliers. Many vehicle manufacturers are moving toward "global platforms," meaning that they will use a small number of chassis, engines, and transmissions as the basis for building many different cars and truck models around the world. With this emphasis, a car might have similar parts, whether it is built in North America, Europe, or Asia. Building on global platforms is expected to lower engineering costs and simplify the variety of parts that a manufacturer deals with. Ford, for example, plans to move from 15 vehicle platforms to about five in the future. |59|

The shift to global platforms is driving consolidation among suppliers, for two reasons. Auto manufacturers will want to use the same components on a given platform regardless of where the vehicle is assembled, so they prefer to deal with parts makers that can supply them worldwide rather than only in certain locations. Also, the automakers commonly ask the larger Tier 1 suppliers to furnish entire systems, such as seating or braking systems, requiring the suppliers to maintain sophisticated design and engineering operations and to handle procurement of the simpler parts used in their products.

The implications for the use of Chinese auto parts in the new platforms hinge on the ability of Chinese auto parts companies to expand their horizons in two ways. First, Chinese parts makers are seeking to increase the quality of their production so it is attractive to global automakers. Second, they likely will seek to become not just makers of individual parts, but also systems integrators, so they can make the complex assemblies that automakers now expect their suppliers to provide. Ultimately, the Chinese government is seeking to develop vehicles that will be built in China and exported more widely to other markets, as the Japanese and Koreans did earlier. Volkswagen already produces parts in China with its partner SAIC Motor, and exports those Chinese wheel hub assemblies to other countries. |60| The combination of automakers building only a few platforms and rising Chinese auto and auto parts quality and sophistication could coincide to spur exports of more parts and eventually vehicles from China.

The North American Tier 1 supplier base has changed over the past decade, with more foreign-owned companies rising into the top ranks of parts manufacturers. The Appendix of this report shows that in 1999, three of the top 10 U.S. suppliers were foreign-based companies with U.S. production facilities (Magna, Bosch, and Denso). By 2011, five of the top 10 were foreign-based suppliers, including the three cited above as well as Continental and Faurecia. It has been estimated that 800 to 1,000 suppliers built plants in the United States in the past 20 years; many are Asian and European suppliers that have followed automakers from their home countries to the United States, but also are interested in selling parts to the Detroit 3. A U.S. government report noted that "suppliers in North America all face competition, historically high material costs, and demanding customers, although the foreign suppliers [with U.S. plants] face fewer legacy costs and so tend to operate more efficiently than their U.S. counterparts." |61|

The other side of industry globalization is the growth of U.S. firms abroad. As foreign-based parts makers were expanding in the United States, many of the U.S.-based parts makers were setting up operations in growing Asian markets, especially China, to serve their Detroit 3 customers that were building cars there. In some cases, according to a Department of Commerce report, they did so because "the Detroit 3 also advocated that U.S.-based suppliers move production to lower cost countries or risk losing future contracts." |62| General Motors is the largest non-Chinese automaker in China and obtains about a quarter of its annual revenues there, |63| so supplying GM's manufacturing in China from a local base became an economic imperative for many of the Tier 1 suppliers. But the auto parts makers also saw the opportunities arising from growing Chinese auto production.

Data on exports and imports show that the U.S. trade pattern in auto parts is shifting, with imports from traditional trading partners (such as Canada and Japan) leveling out while the growth in parts imports is being sourced increasingly from Mexico, China, and Germany, as shown in Table 2. While the United States' overall value of imported parts has increased by 96% in the past decade, import growth from Mexico, China, and Germany exceeds that average, with Chinese imports growing by more than 700%, albeit from a very small base in 2001.

Chinese auto parts are also exported to Mexico, where they are ultimately used in autos made there or included in parts exported to the United States or elsewhere. China accounted for almost 12% of Mexican parts imports in 2010, up from less than 1% in 2000. |64|

U.S.-made parts exports to Mexico rose 103% in the past decade, double the rise in U.S. parts exports overall. The North American Free trade Agreement (NAFTA), which created a fully integrated market for autos and parts made in the United States, Canada, and Mexico, has led to increasing investment by foreign automakers in Mexico. |65| U.S. exports to Canada and Germany also rose, but from a smaller base in 2001. U.S. parts exports to China rose by more than 400% (also from a small base), thus making China the fastest-growing market for U.S. parts exports.

Table 2. U. S. Auto Parts: Exports and Imports

Selected Years and Countries, 2001-2012, in Billions of U.S. Dollars

Region 2001 2005 2009 2012 Percent Change

2001-2012World U.S. Exports $49.8 $55.1 $42.7 $74.7 +50% U.S. Imports $62.7 $92.2 $63.0 $122.7 +96% Canada U.S. Exports 26.4 31.2 19.4 31.6 +20% U.S. Imports 15.8 21.6 10.5 16.3 +0.3% Mexico U.S. Exports 12.0 11.4 12.1 24.4 +103% U.S. Imports 18.2 24.9 18.3 38.9 +114% Japan U.S. Exports 2.0 1.5 0.8 1.5 -25% U.S. Imports 13.2 16.5 8.8 16.2 +23% China U.S. Exports 0.3 0.6 0.9 1.6 +433% U.S. Imports 1.8 5.4 7.4 14.5 +705% Germany U.S. Exports 1.1 1.4 1.2 1.6 +45% U.S. Imports 3.8 6.7 4.8 9.2 +142% Source: U.S. Census Bureau data, prepared by Office of Transportation and Machinery,

U.S. Department of Commerce, http://www.trade.gov/mas/manufacturing/OAAI/build/groups/public/@tg_oaai/documents/webcontent7tg_oaai_003765.pdf.U.S.-China Trade Disputes over Vehicles and Parts

Autos and auto parts have been the subject of a number of trade disputes between the United States and China. All of these disputes have arisen since December 2001, when China was admitted to the WTO. While China has repealed overt pre-WTO regulations favoring its domestic industry over imports, several parts of the 12th Five-Year Plan have generated charges that China is violating some of its WTO obligations in its support for the industry.

Trade concerns have been exacerbated by the challenges facing the U.S. vehicle parts sector. U.S. parts makers were severely affected by the 2007-2009 recession and the steep decline in domestic auto production, as well as by import competition. Parts employment fell in every year from 2001 to 2009, as many companies filed for bankruptcy. While the industry has added 100,000 jobs since its low point of 386,000 in July 2009, the sector provides roughly 350,000 fewer jobs than it did at the start of this century. |66| Meanwhile, parts imports have been rising throughout the past decade, from about 21% of the total U.S. parts market to nearly a third in 2010. |67|

Liberalization of China's auto trade was a major U.S. priority during negotiations over China's accession to the WTO during the late 1990s, especially in regard to its high tariffs, nontariff barriers (such as export performance and domestic content requirements), import substitution policies, license requirements, and trading rights restrictions. |68|

Under the terms of its WTO accession agreement, China agreed to lower tariffs on autos from 80%-100% to 25% by July 2006, while tariffs on auto parts would fall from an average of 23% to an average of 9.5% by the same date. |69| China also agreed to eliminate a number of nontariff barriers, such as restrictions on trading rights and quotas, and it specifically committed not to condition the issuance of import licenses on performance requirements of any kind, such as local content, export performance, offsets, technology transfer, or research and development, or on whether competing domestic suppliers exist. |70|

China initially maintained tariff rate quotas |71| on autos and auto parts, which were gradually phased out. One year after China's WTO accession in December 2001, USTR stated that from the outset, China's quota system was beset with problems due to a delay in the implementation of regulations and other problems that "seemed to reflect protectionist policies," including consumption tax regulations that taxed imported automobiles at a higher rate than domestic vehicles, and the development of unique standards for autos, despite the existence of international standards. The U.S.-China Business Council noted in its 2011 member survey that autos were among the notable industries affected by investment restrictions (along with agriculture, chemicals, energy, express delivery, insurance, securities, and telecommunications). |72|

Export performance requirements facing foreign investors in the automotive sector have also been irritants. U.S.-based Cooper Tire & Rubber, for example, reportedly won approval for investment in China after agreeing to export 100% of its tires for five years. Similarly, Honda has reportedly been allowed to own 65% of an assembly plant in Guangzhou because it agreed to export all of that plant's production. |73| Such requirements can exacerbate trade frictions, as the companies may have incentives to substitute Chinese exports for U.S. production in order to meet the conditions of their investments in China.

The 2005 U.S. WTO Case Against China on Auto Parts

A 2005 report by the American Chamber of Commerce in China (AmCham) stated that China had met or improved its compliance of its WTO obligations in several important auto policy areas, including tariff reduction, quota elimination, distribution, and auto financing. However, the report went on to state that several problems remained. For example, it stated that intellectual property violations (e.g., counterfeit auto parts and design patent and trademark infringement) were common and continued to grow. The report further charged that a 2005 regulation, "Measures on the Management of Parts Import Constituting an Entire Automobile," attempted to discourage firms in China from importing auto parts. The measure required auto manufacturers in China to pay complete built-up vehicle tariffs (25%) on imported parts used to assemble vehicles in China if the assembled vehicles included a certain level (threshold) of imported parts. The Chinese tariff on auto parts at the time was 10%. |74| Manufacturers in China were further affected by requirements by the government to maintain and submit records of their auto parts imports.

In March 2006, the United States (along with the European Union and Canada) initiated a WTO dispute settlement case against these Chinese auto parts policies. China argued that its measures were intended to prevent firms from circumventing tariffs on fully assembled vehicles by importing parts and assembling them into complete vehicles in China. The United States argued that the measures attempted to impose local content requirements on auto manufacturers by assessing additional charges on imported auto parts used in the manufacture of vehicles for sale in China. According to the U.S. WTO complaint,

China's regulations governing the importation of auto parts appear to penalize manufacturers for using imported auto parts in the manufacture of vehicles for sale in China. Although China bound its tariffs for auto parts at rates significantly lower than its tariff bindings for complete vehicles, we understand that China assesses a charge on imported auto parts equal to the tariff on complete vehicles, if the imported parts are incorporated in a vehicle that contains imported parts in excess of specified thresholds. To the extent that the charge is applied when a vehicle is manufactured within China, it would appear to constitute a tax on imported auto parts not imposed on like domestic auto parts. The tax also appears to be applied in a manner so as to afford protection to domestic products. |75|

The United States further contended that the policy not only discouraged auto firms in China from importing auto parts, but also put significant pressure on foreign auto parts producers to relocate manufacturing facilities to China. |76|

In July 2008, a WTO Panel determined that China's regulations on auto parts were inconsistent with its WTO obligations. This ruling was largely upheld by a WTO Appellate Body in December 2008. This was the first time that the WTO found a Chinese measure to be inconsistent with WTO rules. According to USTR, China repealed the measures in September 2009. |77|

After the WTO concluded the case, the New York Times cited auto industry comments indicating that automakers found little to value in the settlement:

But the Chinese action comes after lengthy negotiations during which automakers have moved production to China on a very large scale anyway. Foreign automakers with assembly plants in China have largely stopped using imported auto parts, partly to avoid paying the steep taxes on these parts and partly because international auto parts manufacturers have moved production to China.

General Motors, the automaker that accounts for three-quarters of American-brand vehicle sales in China, now manufactures or purchases in China so many of its auto parts for vehicles sold in China that the government decision to comply with the W.T.O. ruling makes little difference, said Kevin E. Wale, the president and managing director of G.M. China. |78|

U.S. Safeguard Measures on Chinese Tires

Under the provisions of China's WTO accession agreement, China agreed that other WTO members would be able to maintain a China-specific measure, allowing them to restrict imported products from China in instances when imports surged and harmed, or threatened to harm, domestic industries. Under this provision, the United States brought a case against Chinese tire imports in 2009. (This China-specific safeguard measure expires in December 2013.)

On April 24, 2009, the U.S. International Trade Commission (USITC) initiated an investigation |79| of certain types of light vehicle passenger tires, based on a petition filed by the United Steelworkers International Union (USW), which contended that U.S. imports of passenger vehicle and light truck tires from China caused or threatened to cause market disruption to U.S. domestic producers of like or directly competitive products. In June 2009, the USITC announced that it had determined such imports did in fact cause or threaten to cause market disruption, and recommended the imposition of additional tariffs over three years (55% in the first year, 45% in the second, and 35% in the third) and to provide expedited consideration of Trade Adjustment Assistance for firms and/or workers who are affected by such imports.

The USW argued that the "extraordinary increase in imports" of tires from China had hurt tire producers in the United States, contributing to the loss of 5,100 U.S. tire-related jobs from 20042008, and warned that 3,000 more jobs would be lost in 2009. Producers of tires in the United States, many of which have joint-venture operations in China, did not express support for the safeguard case, and some actively opposed it. Some industry representatives argued that a large share of U.S. tire imports from China were low-end products, and that the USITC's proposed increase in tariffs was excessive, would hurt U.S. consumers, and would do little to boost employment in the U.S. tire industry. On September 11, 2009, President Obama announced that he would impose additional tariffs on certain Chinese tires for three years (35% in the first year, 30% in the second year, and 25% in the final year); these levels were less than the USITC's recommendations. The tariffs on tires expired in 2012. |80|

The safeguard tariffs seem to have shifted the source of imports from China to other countries. During the period of the safeguards, total U.S. imports of the types of tires covered by those tariffs rose from 125 million units in 2009 to 158.3 million in 2012, but imports of Chinese tires covered by the safeguards fell from 45.5 million units in 2009 to 30.2 million in 2011. When the tariffs were removed in 2012, tire imports from China rose to 38.9 million units, resuming their earlier growth. During the time the safeguard tariffs for Chinese tires were in effect, imports of the same kinds of tires from Korea, Canada, Thailand, Mexico, Indonesia, Taiwan, and Chile rose in volume. China's share of these types of tires sold in the United States fell from 36% in 2009 to 20% in 2011, before rising to 25% in 2012, after the tariffs came off. |81|

China called the imposition of increased U.S. tariffs on Chinese tires protectionist, and responded by initiating a WTO trade dispute settlement case against the United States on September 14, 2009. The WTO ruled that U.S. actions did not violate U.S. WTO commitments.

On November 11, 2009, shortly after imposition of the U.S. safeguard measures on tires, China launched antidumping and countervailing cases against U.S. autos (as well as poultry). In December 2011, China imposed anti-dumping duties (ranging from 2.0% to 21.5%) and countervailing duties (ranging from 6.2% to 12.9%) on American-produced cars and SUVs over two years. The United States charged that the action was unjustified because Chinese authorities did not objectively examine the evidence as to whether certain U.S. policies to support the U.S. auto industry caused injury to China's domestic industries. On July 5, 2012, the United States initiated a WTO dispute settlement case against China, calling the imposition of duties on American-made automobiles "yet another abuse of trade remedies by China." A WTO dispute panel was named in February 2013, but no action has been taken on the U.S. complaint.

China has increasingly used a number of export restrictions (including export taxes, quotas, licenses, and prohibitions) on a wide range of raw materials, |82| such as rare earth minerals used in automaking. |83| China produces an estimated 97% of all rare earths, a unique group of 17 metal elements on the periodic table that exhibit a range of special properties, such as magnetism, luminescence, and strength. Rare earths are important in a number of automotive uses, including the manufacture of permanent magnets for hybrid and electric vehicle motors. |84|

In recent years, the Chinese government has implemented policies to tighten its control over the production and export of rare earths. Such restrictions include quotas, export taxes, production limits, and minimum export prices. Such policies have sharply raised prices for rare earth users, especially non-Chinese firms. In 2010, China placed an embargo on the export of rare earths and then added export duties. These restraints affected especially Toyota, which, at the time, produced more hybrid vehicles (such as the Prius) than any other automaker. |85| It has been asserted that China's rare earth export policies are leading some rare earth users, including some automakers, to move operations to China, and subsequently to transfer technology to Chinese firms. |86| China denies that its rare earth policies are discriminatory or protectionist, and claims they are intended to address environmental concerns in China and to better manage and conserve limited resources. |87|

On March 13, 2012, the United States, Japan, and the European Union jointly initiated a WTO dispute settlement case against China's restrictive policies on rare earths (as well as on tungsten and molybdenum). This case was brought shortly after the United States prevailed in a similar WTO case brought against China over its export restrictions on nine raw materials. |88| The WTO has not ruled on the rare earths case.

The U.S. WTO Case Against China on Auto and Auto Parts Subsidies

Some Members of Congress have expressed "serious concern" about China's trade practices in the auto parts sector. A letter signed by 188 Members of Congress in March 2012 stated

Seventy-five percent of the jobs in the automotive sector are in auto parts, and these jobs are at risk in every state in the nation. China has virtually closed its market to our auto parts exports and continues to take actions to further limit access. Given its importance, the Administration's vigilance in addressing China's harmful policies now, while we can still change this one-way street in trade, is essential. |89|

The letter urged the Administration's Interagency Trade Enforcement Center (created in February 2012) to "address Chinese predatory policies in auto parts" as one of its initial priorities. |90|

On September 17, 2012, the United States announced that it would initiate a WTO dispute settlement case against China's export subsidies to auto and auto parts manufacturers in China. |91| The United States has charged that China maintains an auto and auto parts "export base" subsidy program estimated to have totaled at least $1 billion from 2009-2011. The United States argues that the program constitutes an export subsidy prohibited under WTO rules because 12 Chinese municipalities have been designated as auto and auto parts export centers and receive government funding on the basis of their export performance. Such subsidies allegedly include grants, tax preferences, and reduced interest rates. |92| A 2012 report by the Economic Policy Institute contended that Chinese subsidies to the auto parts sector are more extensive, estimating that the sector received $27.5 billion in subsidies from 2001 to 2011, and has been promised another $10.9 billion in subsidies through 2020. |93|

The United States and China held consultations in November 2012, but the case is unresolved at this time.

U.S. officials have raised a number of concerns over Chinese investment restrictions related to new energy vehicles (NEVs), such as hybrid and battery electric vehicles. A Chinese government list of 400 cars eligible for the energy-saving vehicles program is reportedly restricted to vehicles produced in China, and a 2011 sales tax exemption to boost sales of such cars is similarly limited. |94| USTR has also alleged that joint venture agreements with foreign auto companies require a transfer of energy-saving vehicle technology, and that GM, Ford, Daimler, and other non-Chinese companies have agreed under pressure to share powertrain and vehicle battery technology with their Chinese joint venture partners. |95|

Chinese government draft regulations reportedly specify that automakers that intend to manufacture electric vehicles in China must demonstrate a "mastery" level of proficiency in key parts such as electric vehicle batteries, motors, or control systems before receiving a license to produce and sell electric vehicles. In addition, according to reports on current drafts, the Chinese entity that manufacturers the vehicle, either a domestic manufacturer or joint venture operation, must demonstrate clear ownership of intellectual property rights to the technologies that enable the "mastery." |96| U.S. industry representatives contended that such policies would force U.S. companies to transfer their intellectual property in order to participate in China's NEV market. China has announced plans to manufacture 1 million NEVs by 2015 and 5 million annually by 2020. |97|

At the 2011 U.S.-China Joint Commission on Commerce and Trade (November 20-21, 2011), China

- confirmed that "it does not and will not maintain measures that mandate the transfer of technology";

- clarified that "mastery of core technology" does not require technology transfer for NEVs;

- confirmed that the establishment of brands is a corporate decision and that the Chinese government does not and will not impose any requirements for foreign-invested companies to establish domestic brands in China;

- confirmed that foreign-invested enterprises are eligible on an equal basis for subsidies or other preferential policies for NEVs with Chinese enterprises, and that these subsidies and preference programs will be implemented in a manner consistent with WTO rules; and that China affirmed that as it develops possible future NEV support programs, the views of all stakeholders will be considered, including the comments and opinions of the United States.

However, these pledges have not alleviated the concerns. In 2012, USTR's National Trade Estimate Report on Foreign Trade Barriers continued to cite industry concerns over China's policies regarding NEVs.

Ten years ago, the Chinese auto industry was in its infancy, with a very low level of production and sales, few imports or exports, and vehicles whose quality was not up to par with cars and trucks produced in countries with larger and more sophisticated auto industries. The recession that hit the United States, Japan, and Europe did not affect China's economy so severely. As vehicle production and sales lagged in Europe, North America, and Japan, they expanded dramatically in China, more than doubling from 2009 to 2012. No other nation's auto industry has seen such robust growth in the past decade.

China's growing middle class increasingly values car and truck ownership and, with a population of more than 1.3 billion, there is room for significant expansion of the Chinese auto market even after its recent growth spurt. China has not excluded foreign automakers from establishing a presence there, but they must be minority or 50/50 partners with Chinese firms, many of which are owned by provincial and municipal governments. Parts makers, on the other hand, are permitted to own a majority share of operations in China. It appears clear from China's Five-Year Plans that building up the size and quality of the auto assembly and auto parts industries is a very high national priority. Moreover, China's long-term plan--its feasibility as yet untested--is to leapfrog over gasoline-powered internal combustion engine technology into new energy vehicles, such as electric and fuel-cell-powered cars.

Nearly all major foreign automakers are participating in the Chinese market. The Chinese government welcomes their role in expanding its domestic industry. Similarly, the Chinese embrace investments by foreign parts makers, which build parts there to service the automakers from their home countries. The Chinese government's plan to consolidate auto and parts makers could in the future result in greater competition for U.S., European, and Japanese firms, which now have a decided edge over the fragmented Chinese domestic industry.

However, Chinese state intervention in the auto and auto parts industries could limit the benefits for non-Chinese manufacturers relative to what would occur under more open markets and trade. When China joined the WTO in 2001, it appeared to signal that it was on a path toward accelerating its transition to a market economy. However, USTR has noted that since 2006, there has been a "troubling trend in China toward intensified state intervention," and that China seems to be "embracing state capitalism more strongly." |98| At a November 2011 WTO review of China's WTO compliance, the U.S. representative stated that the auto sector was one sector that the U.S. highlighted as having been particularly plagued by government intervention.

In addition to the commercial opportunities presented by the Chinese market, there have also been growing pains in the U.S.-China motor vehicle trade relationship. A half-dozen trade disputes have developed in the past 12 years, many resulting in WTO rulings and changes in Chinese laws and regulations affecting the motor vehicle industry.

When Japanese auto companies began to export extensively to the United States in the 1980s and 1990s, many in Congress argued that Japanese auto policies were unfair, and legislation was introduced to limit imports of Japanese cars. This pressure led Japanese auto firms to restrain auto exports to the United States and to build U.S. auto plants. So far, China is exporting auto parts and not automobiles to the United States. Growing Chinese investment in the U.S. auto and auto parts industry could alleviate concerns over increased U.S. imports of automotive products from China as long as such commercial activity is not seen as unfair under U.S. trade laws or WTO rules.

A key factor in the growth of the Chinese auto industry will be how well it can generate and sustain its own innovations, which regularly mark the growth of the auto industry everywhere in the world. Consolidation without innovation and home-grown technology applications may leave the indigenous Chinese auto and parts makers reliant on foreign joint ventures.

[Source: By Bill Canis and Wayne M. Morrison, Congressional Research Service, R43071, Washington, 13May13. Bill Canis is a Specialist in Industrial Organization and Business and Wayne M. Morrison is a Specialist in Asian Trade and Finance]

Appendix. Largest North American

Auto Parts SuppliersTable A-1. 10 Largest North American Auto Parts Suppliers, 1999 vs. 2011

Company, Location, and Revenue from Sales to North American Assembly Plants

Company/U.S. Base 1999 OEM Revenue Company/U.S. Base 2011 OEM Revenue Delphi Automotive Systems

Troy, MI$22.4 billion Magna International

Aurora, Ontario$14.7 billion Visteon Automotive Systems

Dearborn, MI$15.0 Johnson Controls

Plymouth, MI$7.9 Lear Corp.

Southfield, MI$8.1 Continental Automotive Systems

Auburn Hills, MI$5.8 Dana Corp,

Toledo, OH$7.8 Robert Bosch

Farmington Hills, MI$5.6 Johnson Controls

Plymouth, MI$6.9 Denso International America

Southfield, MI$5.5 Magna International

Aurora, Ontario$5.8 Delphi Automotive Systems

Troy, MI$5.1 Robert Bosch

Farmington Hills, MI$5.1 Lear Corp.

Southfield, MI$5.0 TRW, Inc.

Cleveland, OH$4.7 Faurecia

Auburn Hills, MI$4.7 Denso International America

Southfield, MI$3.4 TRW Automotive

Livonia, MI$4.6 Eaton Corp.

Cleveland, OH$2.9 Cummins

Columbus, IN$4.1 Source: Automotive News, "Top 150 OEM Parts Suppliers to North America," 1999, and "Top 100 suppliers to North America, 201 1."

Notes: The companies shown are the largest Tier 1 suppliers; revenues shown are based on each company's sales of original equipment parts. Companies shown in bold type had their headquarters outside the United States.

Notes:

1. The American Recovery and Reinvestment Act of 2009 (P.L. 111-5) funded $2.4 billion in new federal investments in electric vehicle manufacturing facilities. [Back]

2. The Advanced Technology Vehicles Manufacturing program (ATVM) at the Department of Energy was established in 2007 (P.L. 110-140), authorizing up to $25 billion in loans to support development of more fuel-efficient vehicles. [Back]

3. Many Members of Congress continue to express concern over purportedly discriminatory Japanese policies on U.S. autos, and some have cited such policies in expressing their opposition to Japan joining the Trans-Pacific Partnership (TPP). See CRS Report R42676, Japan's Possible Entry Into the Trans-Pacific Partnership and Its Implications, by William H. Cooper and Mark E. Manyin. [Back]

4. See CRS Report RL34330, The U.S.-South Korea Free Trade Agreement (KORUS FTA): Provisions and Implications, coordinated by William H. Cooper. [Back]

5. For a more detailed look at the Chinese auto industry, see CRS Report R40924, China's Auto Sector Development and Policies: Issues and Implications, by Rachel Tang. [Back]

6. Automotive News Data Center. [Back]

7. World Bank, 2010 data, http://databank.worldbank.org/data/views/reports/tableview.aspx. [Back]

8. Nathan Bomey, "China's car market grows more slowly," Detroit Free Press, April 17, 2013. [Back]

9. Kelly Sims Gallagher, Foreign Technology in China's Automobile Industry: Implications for Energy, Economic Development, and Environment, Woodrow Wilson Center, China Environment Series, Issue 6, 2003, p. 8, http://www.wilsoncenter.org/sites/default/files/2-feature_1.pdf. [Back]

10. Kelly Sims Gallagher, Foreign Technology in China's Automobile Industry: Implications for Energy, Economic Development, and Environment, Woodrow Wilson Center, China Environment Series, Issue 6, 2003, p. 8, http://www.wilsoncenter.org/sites/default/files/2-feature_1.pdf. [Back]

11. SAIC Motor is a state-owned enterprise, held by the State Assets Supervision Administration Commission. Nathaniel Ahrens, China's Competitiveness, Case Study: SAIC Motor Corporation, Center for Strategic & International Studies, January 2013, p. 2. [Back]

12. Wuling Automobile Co. is partnered with a state-owned enterprise, Liuzhou Wuling Motors Company Ltd. Wuling Motors Holdings, http://www.wuling.com.hk/index.php?option=com_content&task=view&id=3&Itemid=30&lang=english. According to GM, its joint venture with Wuling also includes SAIC and is known as SAIC-GM-Wuling Automobile Co. Ltd., officially launched on November 18, 2002. SAIC has a 50.1% stake, GM China a 44.0% stake, and Wuling Motors a 5.9% stake, http://media.gmchina.com/media/cn/en/gm/company/facilities/sgmw.html. [Back]

13. Passenger cars make up more than half of all vehicle sales. On the other hand, in the domestic commercial vehicle market, 80% are produced by domestic Chinese automakers. Ward's Automotive Database 2012 and EUSME Centre, "The Automotive Market in China," 2012, p. 1, http://www.eusmecentre.org.cn/content/automobiles-and-autoparts. [Back]

14. GM and its joint venture partners sold 2.8 million vehicles in China in 2012; GM sold 2.6 million vehicles in the United States (including imports). Source: General Motors 2012 Annual Report. [Back]

15. Frank Langfitt, "These Days, More And More Chinese Have Driven A Ford Lately," National Public Radio, April 25, 2013, http://www.npr.org/2013/04/25/178802129/these-days-more-and-more-chinese-have-driven-a-ford-lately. [Back]

16. Brent Snavely, "Chrysler announces deal to build Jeeps in China," Detroit Free Press, January 15, 2013, http://www.usatoday.com/story/money/cars/2013/01/15/jeep-guangzhou-china/1566380/. [Back]

17. For example, the General Motors category includes cars made in China by GM in its joint ventures with SAIC Motor and Wuling, as well as imported GM vehicles. [Back]

18. China Association of Automobile Manufacturers (CAAM), http://www.caam.org.cn. [Back]

19. BBVA Research, Automobile Market Outlook: China, Hong Kong, June 19, 2012, p. 7. [Back]

20. By comparison, nearly half of Japan's auto production is exported annually. U.S. auto plants exported 12% of vehicle production in 2011, with about half coming from the Detroit 3 and the other half from foreign automakers such as Honda and BMW. Joann Muller, "Foreign Carmakers Ship More Made-In-USA Cars Overseas," Forbes, December 6, 2012, http://www.forbes.com/sites/joannmuller/2012/12/06/foreign-carmakers-ship-more-made-in-usa-cars-overseas/. [Back]

21. American Association of Motor Vehicle Administrators, Best Practice Regarding Registration and Titling of Mini-Trucks, January 10, 2011, Appendix B. [Back]

22. Chester Dawson and Sharon Terlep, "China Ramps Up Auto Exports," Wall Street Journal, April 24, 2012. [Back]

23. The Chinese automaker BYD announced in 2008 that it would sell an electric vehicle in the United States by 2010, but it failed to do so. GM reportedly planned in 2009 to build a small car in China for export to the United States, but during its restructuring and bankruptcy, it decided to build that car (now known as the Sonic) at a Michigan plant. In 2006, investor Malcolm Bricklin sought to build cars with Chinese automaker Chery for export to the United States, but called off his plans as a result of production issues in China. Coda, which began production of an all-electric vehicle in California with many components sourced in China, ceased production and filed for Chapter 11 bankruptcy protection on May 1, 2013; see "Company will leave autos, focus on energy," Reuters, May 1, 2013. [Back]

24. Ralph Drauz, "On the Chinese Import Car Market," China Car Times, October 25, 2012, http://www.chinacartimes.com/2012/10/25/chinese-import-car-market/. [Back]

25. EU SME Centre, "The Automotive Market in China," 2012, p. 5. [Back]

26. Ralph Drauz, "On the Chinese Import Car Market," China Car Times, October 25, 2012, http://www.chinacartimes.com/2012/10/25/chinese-import-car-market/. [Back]

27. The 2013 consumption tax on cars, by cylinder capacity, is 1% on vehicles with engines less than 1 liter; 3% on 1-1.5 liter engines; 5% on 1.5-2 liters; 9% on 2-2.5 liters; 12% on 2.5-3 liters; 25% on 3-4 liters; and 40% if over 4 liters. "China Release Announcement on Consumption Tax Policies," China Briefing, December 4, 2012, http://www.china-briefing.com/news/2012/12/04/china-releases-announcement-on-consumption-tax-policies.html. [Back]

28. Based on volume of exports. 2011 data sourced from U.S. International Trade Administration, Growth Trends in U.S. Vehicle Exports, Washington, DC, April 2012. The 2012 data were developed for CRS and have not been released publicly by ITA at this time. [Back]

29. U.S. Department of Commerce, International Trade Administration, Current State of the U.S. Automotive Parts Industry, 2011, p. 2, http://www.trade.gov/mas/manufacturing/oaai/static/Auto%20Parts%20Paper%202012%20final_Latest_tg_oaai_003966.pdf. [Back]

30. U.S. Trade Representative, "Fact Sheet: WTO Case Challenging Chinese Subsidies," September 17, 2012, http://www.ustr.gov/about-us/press-office/fact-sheets/2012/september/wto-case-challenging-chinese-subsidies. [Back]

31. U.S. International Trade Commission (USITC) Dataweb. [Back]

32. U.S. Department of Commerce, Office of Transportation and Machinery, On the Road: U.S. Automotive Parts Industry Annual Assessment, Washington, DC, 2011, p. Table 5. [Back]

33. Based on statement by Motor and Equipment Manufacturers Association to CRS. [Back]

34. AMS is a tracking system for air, rail, marine, and rail cargo transference at U.S. borders. Its purpose is to reduce international security threats, http://www.worldtraderef.com/WTR_site/AMS.asp. [Back]

35. Terence Stewart, Elizabeth Drake, and Philip Butler, China's Support Programs for Automobiles and Auto Parts Under the 12th Five Year Plan, Law Offices of Stewart and Stewart, Washington, DC, January 2012, p. 80. The analysis does not specify whether foreign-based automakers such as Honda, Toyota, or Volkswagen imported parts directly from China for assembly into U.S. vehicles. As AMS does not require importers to disclose their identities, an evaluation of parts imported by the Detroit 3 could be made only on a limited basis. [Back]

36. Under the American Automobile Labeling Act (AALA), all automakers report annually to the National Highway Traffic Safety Administration (NHTSA) the foreign and U.S./Canadian content of all cars sold in the United States, and must list the country of origin of the engine and transmission, http://www.nhtsa.gov/Laws+&+Regulations/Part+583+American+Automobile+Labeling+Act+%28AALA%29+Reports. [Back]

37. EU SME Centre, "The Automotive Market in China," 2012, p. 6. [Back]

39. Usha C.V. Haley, Putting the Pedal to the Metal: Subsidies to China's Auto-Parts Industry from 2001-2011, Economic Policy Institute, Briefing paper no. 316, Washington, DC, January 31, 2012, p. 3. [Back]

40. Bureau of Labor Statistics, Quarterly Census of Employment and Wages, identified 5,589 U.S. parts manufacturing establishments in third quarter 2012. [Back]

41. APCO Worldwide, Market Analysis Report: China's Automotive Industry, November 2010, p. 8, http://www.export.gov.il/uploadfiles/03_2012/chinasautomotiveindustry.pdf. [Back]

42. Currently, 40% of TRW's revenue comes from Europe, 35% from North America, 15% from China, and 10% from other developing markets. It makes brakes, airbags, steering systems, and other vehicle parts. Yang Jian, "TRW CEO: China May Surpass U.S. as Top Market for Supplier by 2020," Automotive News China, May 3, 2013. [Back]

43. "Beijing West nets control of Delphi's key units," China Daily, April 2, 2009. [Back]

44. In March 2011, Chinese state-owned parts manufacturer AVIC Automobile Industry Holding Co. acquired a 51% stake in Pacific Century Motors. [Back]

45. "PCM acquires GM's parts-supplier unit," People's Daily Online, December 1, 2010. [Back]

46. As part of the bankruptcy proceeding, A123 Systems changed its name to B456 Systems in March 2013. [Back]

47. The division of A123 Systems that has contracts with the U.S. Defense and Energy Departments was sold to a U.S. company, Navitas Systems. See New York Times, "Chinese Firm Wins Bid for Auto Battery Maker," December 9, 2012. CFIUS is an inter-agency committee of the U.S. government that is authorized to review foreign investment transactions that could result in control of a U.S. business by a foreign entity, in order to determine the effect of such transactions on the national security of the United States. CFIUS is chaired by the Secretary of the Treasury. [Back]

48. Under the terms of the sale, Wanxiang's ownership will prevent A123 from drawing down the remaining $120 million of the $249 million U.S. Department of Energy grant, SeekingAlpha.com, "Johnson Controls Appeals Sale of A123 to China's Wanxiang," December 18, 2012, http://seekingalpha.com/article/1071031-johnson-controls-appeals-sale-of-a123-to-china-s-wanxiang. [Back]

49. Five-year plans set out the government's goals for the upcoming five-year period. BBVA Research, Automobile Market Outlook: China, Hong Kong, June 19, 2012, p. 5, http://serviciodeestudios.bbva.com/KETD/fbin/mult/120619_China_Automobile_Outlook_EN_Edi_tcm348-334127.pdf?ts=1122013. [Back]

50. Terence Stewart, Elizabeth Drake, and Philip Butler, China's Support Programs for Automobiles and Auto Parts Under the 12th Five Year Plan, Law Offices of Stewart and Stewart, Washington, DC, January 2012, p. 27. [Back]

51. Sharon Terlep, "Road Gets Bumpy for GM in China," Wall Street Journal, September 16, 2011. [Back]

52. General Motors, "SAIC and GM Sign Agreement for Electric Vehicle Development," press release, September 20, 2011, media.gm.com/content/media/us/en/gm/news.detail.html/content/Pages/news/us/en/2011/Sep/0920_saic.html. [Back]

53. "GM Ends Joint EV Project with SAIC, Report Says," Automotive News China, April 26, 2013. The report says that GM is using LG Chem of Korea for its batteries, while SAIC Motor is partnered with B456 Systems (formerly A123 Systems). [Back]

54. BBVA Research, Automobile Market Outlook: China, Hong Kong, June 19, 2012, p. 9. [Back]

55. "Strategic emerging industries likely to contribute 8% of China's GDP by 2015," People's Daily, October 19, 2010, http://english.peopledaily.com.cn/90001/90778/90862/7170816.html. [Back]

56. Terence Stewart, Elizabeth Drake, and Philip Butler, China's Support Programs for Automobiles and Auto Parts Under the 12th Five Year Plan, Law Offices of Stewart and Stewart, Washington, DC, January 2012, p. 7. [Back]

58. Terence Stewart, Elizabeth Drake, and Philip Butler, China's Support Programs for Automobiles and Auto Parts Under the 12th Five Year Plan, Law Offices of Stewart and Stewart, Washington, DC, January 2012, pp. 43-44. [Back]

59. Mike Ramsey, "Ford SUV Marks New World Car Strategy," Wall Street Journal, November 16, 2011. [Back]

60. Anthony Fontanelle, "Chinese Automakers to Develop Car for Global Market," streetdirectory.com, http://www.streetdirectory.com/travel_guide/51467/car_focus/chinese_automaker_to_develop_car_for_global_market.html, viewed April 8, 2012. [Back]

61. U.S. Department of Commerce, Office of Transportation and Machinery, On the Road: U.S. Automotive Parts Industry Annual Assessment, Washington, DC, 2011, p.8. [Back]

63. General Motors 2012 Annual Report. [Back]

64. Vehicles are assembled in Mexico by U.S., Japanese, Korean, and European manufacturers. More than 80% of Mexican auto production is exported, with about 90% of the exports sold in the United States. Enrique Dussel Peters, "The Auto Parts-Automotive Chain in Mexico and China: Co-operation Potential?," China Quarterly, Number 209, March 2012, pp. 94-95, http://www.dusselpeters.com/55.pdf. [Back]

65. Ibid. According to this source, the United States accounted for 53% of the parts imported into Mexico in 2010, down from more than 70% in 2000. Germany and Japan were the second- and third-largest auto parts exporters to Mexico in 2010; China was fourth-largest. Vehicles are assembled in Mexico by U.S., Japanese, Korean, and European manufacturers. More than 80% of Mexican auto production is exported, with about 90% of the exports sold in the United States. [Back]

66. Bureau of Labor Statistics, Current Employment Statistics, http://www.bls.gov/ces/, viewed April 30, 2013. [Back]

67. Office of Transportation and Machinery, U.S. Department of Commerce, On the Road: U.S. Automotive Parts Industry Annual Assessment, 2011, p. Table 5. [Back]

68. USTR Press Release, December 2008, at http://www.ustr.gov/archive/assets/Document_Library/Press_Releases/2008/December/asset_upload_file341_15242.pdf. [Back]

69. USTR, 2002 Report to Congress on China's WTO Compliance, December 11, 2002, p. 9. [Back]

70. USTR, 2003 Report to Congress on China's WTO Compliance, December 2003. [Back]

71. A tariff rate quota is a quota system with a two-tiered tariff. Products that enter under the quota enter at a lower tariff rate, with a higher (out-of-quota) tariff rate used for imports above the concessionary access level. [Back]

72. https://www.uschina.org/public/documents/2011/10/membership_survey_english.pdf. [Back]

73. Eric Thun, Changing Lanes in China: Foreign Direct Investment, Local Governments, and Auto Sector Development (New York: Cambridge University Press, 2006), p. 243. [Back]

74. Manufacturers in China that imported auto parts paid a 10% tariff, and if those parts fell below a local-content threshold, they were required to pay an additional internal charge of 15%. [Back]

75. WTO, Dispute Settlement, China--Measures Affecting Imports ofAutomobile Parts, Request for Consultations by the United States, April 3, 2006. [Back]

76. USTR, Press Release, December 15, 2008. [Back]

77. USTR, 2009 Report to Congress on China's WTO Compliance, December 2009, p. 6. [Back]

78. Keith Bradsher, "Despite Trade Rulings, Beijing Gains From Delay Tactics," New York Times, August 30, 2009. [Back]

79. U.S. International Trade Commission, Certain Passenger Vehicle and Light Truck Tires from China, Investigation No. TA-421-7, Publication 4085, Washington, DC, July 2009. The petition was filed under Section 421 of the 1974 Trade Act, as amended, 19 U.S.C. 2451. [Back]

80. For additional information on this issue, see CRS Report R41551, The U.S. Tire Industry: Technological Change and Import Competition, by Glennon J. Harrison and Michaela D. Platzer. [Back]

82. According to the U.S. Geological Survey (USGS), China is a major global producer and, in some cases, a dominant producer of many raw and processed materials. For example, in 2010, China accounted for more than 80% of global production of antimony, magnesium metal, rare earths, and tungsten. It also accounted for between 50% and 80% of global production of more than a dozen other materials. China was the largest global producer of 37 out of the 80 mineral commodities tracked by USGS. Statement of W. David Menzie, Chief of Global Minerals Analysis, National Minerals Information Center, USGS, before the U.S.-China Economic and Security Review Commission hearing on "China's Global Quest for Resources and Implications for the United States," January 26, 2012. [Back]

83. According to the WTO, raw materials affected by Chinese restraints include sawn timber, coke, oil, rare earth elements, antimony and its products, tungsten and its products, zinc ore, tin and its products, silver, indium, molybdenum, phosphate rocks, carbide, fluorspar, talc, magnesium, and bauxite. China also imposes export restraints on a number of agricultural products. [Back]

84. Neodymium is the rare earth element used in electric motor magnets. [Back]

85. Since the Chinese embargo and imposition of export duties, efforts have intensified to find other sites outside of China that could produce rare earths, including in the United States. In addition, Toyota and other automakers have sought to find ways around using some of the rare earths in hybrid vehicles. [Back]

86. Yuko Inoue and Julie Gordon, "Analysis: Japanese rare earth consumers set up shop in China," Reuters, August 12, 2011. [Back]

87. For a further discussion of rare earths, see CRS Report R42510, China's Rare Earth Industry and Export Regime: Economic and Trade Implications for the United States, by Wayne M. Morrison and Rachel Tang. [Back]

88. However, prices of U.S. imports of Chinese rare earths have fallen sharply, declining from $158,389 per metric ton in September 2011 to $15,739 in March 2013, caused in part by a relaxation of Chinese restrictions on output, increasing smuggling, and slumping foreign demand. Rare earth pricing data are from USITC Dataweb. [Back]

89. The letter is available at http://www.brown.senate.gov/newsroom/press/release/following-release-of-reports-showing-16-million-auto-parts-jobs-at-risk-brown-leads-188-members-of-congress-in-calling-for-more-aggressive-trade-enforcement-to-protect-american-jobs. [Back]

90. During his State of the Union Address on January 24, 2012, President Obama announced that he would create a new federal trade enforcement unit "charged with investigating unfair trade practices in countries like China." On February 28, 2012, President Obama issued an executive order establishing an Interagency Trade Enforcement Center within USTR to more effectively address trade enforcement issues. [Back]

91. For a list of alleged Chinese subsidies for auto and auto parts "export bases," see USTR Consultation Request Letter, ustr.gov/webfm_send/3541. [Back]

92. This WTO case is described further by USTR in The President's 2013 Trade Policy Agenda, Washington, DC, March 2013, pp. 64-65. [Back]

93. Usha C.V. Haley, Putting the Pedal to the Metal: Subsidies to China's Auto Parts Industry from 2001 to 2011, Economic Policy Institute, Washington, DC, January 31, 2012, p. 1, http://www.epi.org/ffiles/2012/bp316.pdf. [Back]

94. USTR, The President's 2013 Trade Policy Agenda, pp. 64-65. [Back]

97. U.S.-China Joint Commission on Commerce and Trade, Press Release (November 22, 2011). [Back]

98. USTR, 2011 Report to Congress on China's WTO Compliance, December 2011, p. 2. Many of the industrial policies that China has implemented or formulated since 2006 appear to stem largely from a comprehensive document issued by the State Council (the highest executive organ of state power) in 1996 titled the National Medium- and Long-Term Program for Science and Technology Development (2006-2020). The plan, often referred to as the MLP, appears to represent an ambitious initiative to modernize the structure of China's economy by transforming it from a global center of low-tech manufacturing to a major center of innovation by 2020 and a global innovation leader by 2050. One of the central goals is to lessen the country's dependence on foreign intellectual property through government support to develop indigenous intellectual property. [Back]

| This document has been published on 22May13 by the Equipo Nizkor and Derechos Human Rights. In accordance with Title 17 U.S.C. Section 107, this material is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. |