| Information |  | |

Derechos | Equipo Nizkor

| ||

| Information | | |

Derechos | Equipo Nizkor

| ||

09Feb17

See updated versions: 23Jan18 - 02Apr18

China-U.S. Trade Issues

Back to topContents

Introduction

Most Recent Developments

U.S. Trade with ChinaU.S. Merchandise Exports to China

Major U.S. Merchandise Imports from China

Trade in Services

The U.S. Merchandise Trade Deficit with China

The Transfer of Pacific Rim Production to China by Multinational Firms

China as a Major Center for Global Supply Chains

Jobs and TradeU.S.-China Investment Ties: Overview

Chinese "State Capitalism" New Restrictions on Information and Communications Technology

Intellectual Property Rights (IPR) Issues China's Obligations in the World Trade Organization China's Currency PolicyThe U.S.-China Strategic and Economic Dialogue

Concluding ObservationsFigures

Figure 1. Top 5 U.S. Merchandise Export Markets in 2016

Figure 2. Major Sources of U.S. Merchandise Imports: 2016

Figure 3. Major U.S. Services Trading Partners in 2015

Figure 4. U.S. Merchandise Trade Balance with China: 2000-2016

Figure 5. Five Largest U.S. Merchandise Trade Imbalances in 2016

Figure 6. U.S. Manufactured Imports from Pacific Rim Countries as a Percentage of Total U.S. Manufactured Imports: 1990, 2000, and 2015

Figure 7. U.S. Manufactured Imports from China and Japan as a Percentage of U.S. Total: 1999-2015 (%)

Figure 8. U.S. Computer Imports from China as a Percentage of Total U.S. Computer Imports: 2000-2015

Figure 9. Estimated Percentage Foreign Value-Added to China's Exports in 2011

Figure 10. Top Five Country Sources of Facilities that Supply Apple Corporation in 2015

Figure 11. China's Holdings of U.S. Treasury Securities: 2002-November 2016

Figure 12. BEA and Rhodium Group Estimates of the Stock of U.S.-China FDI through 2015

Figure 13. BEA and Rhodium Group Data on Annual U.S. FDI Flows to China: 2005-2015

Figure 14. BEA and Rhodium Group Data on Chinese FDI Flows to the United States: 2005-2015

Figure 15. RMB-Dollar Exchange Rates: January 2015 to December 2016

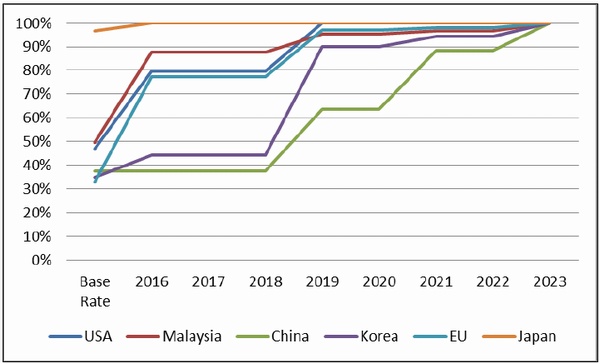

Figure B-1. Current MFN Duty Levels on Products Covered in ITA-2

Figure B-2. ITA-2 Tariff Phase-out Schedule for Major MembersTables

Table 1. U.S. Merchandise Trade with China: 1980-2016

Table 2. Major U.S. Exports to China in 2016

Table 3. Major U.S. Merchandise Export Markets: 2001-2016

Table 4. Major U.S. Merchandise Imports From China in 2016

Table 5. China's Holdings of U.S. Treasury Securities: 2002-November 2016

Table 6. Summary of BEA Data on U.S.-China FDI Flows: 2015

Table 7. Top 20 Chinese Companies on Fortune's Global 500 in 2016

Table 8. Summaries of WTO U.S. Dispute Settlement Cases Against ChinaAppendixes

Appendix A. Chinese Policies to Boost Innovation

Appendix B. Plurilateral Agreements

Appendix C. S&ED Outcomes

Summary

U.S.-China economic ties have expanded substantially over the past three decades. Total U.S.China merchandise trade rose from $2 billion in 1979 (when economic reforms began) to $579 billion in 2016. China is currently the United States' second-largest merchandise trading partner, its third-largest export market, and its biggest source of imports. According to one source, China is a $400 billion market for U.S. firms when U.S. services exports to China, sales by U.S. foreign affiliates in China, and re-exports of U.S. products through Hong Kong to China are factored in. Many U.S. firms view participation in China's market as critical to staying globally competitive. General Motors (GM), for example, which has invested heavily in China, sold more cars in China than in the United States each year from 2010 to 2016. In addition, U.S. imports of lower-cost goods from China greatly benefit U.S. consumers, and U.S. firms that use China as the final point of assembly for their products, or use Chinese-made inputs for production in the United States, are able to lower costs. China is the second-largest foreign holder of U.S. Treasury securities ($1.0 trillion as of November 2016), and its purchases of U.S. government debt help keep U.S. interest rates low.

Despite growing commercial ties, the bilateral economic relationship has become increasingly complex and often fraught with tension. From the U.S. perspective, many trade tensions stem from China's incomplete transition to a free market economy. While China has significantly liberalized its economic and trade regimes over the past three decades, it continues to maintain (or has recently imposed) a number of state-directed policies that appear to distort trade and investment flows. Major areas of concern expressed by U.S. policymakers and stakeholders include China's alleged widespread cyber economic espionage against U.S. firms; relatively ineffective record of enforcing intellectual property rights (IPR); discriminatory innovation policies; mixed record on implementing its World Trade Organization (WTO) obligations; extensive use of industrial policies (such as financial support of state-owned firms and trade and investment barriers) in order to promote and protect industries favored by the government; and interventionist policies to influence the value of its currency. Many U.S. policymakers argue that such policies adversely impact U.S. economic interests and have contributed to U.S. job losses.

There are different views on how the United States could better address commercial disputes with China. Trump Administration officials contend that the United States should take a more aggressive stance against China's trade policies, such as by increasing the number of U.S. WTO dispute settlement cases brought against China, expanding the use of U.S. trade remedy laws on certain imports from China, designating it as a "currency manipulator" and/or threatening to impose sanctions against China unless it addresses various policies, such as cyber theft of U.S. business trade secrets, that hurt U.S. economic interests. Others contend that U.S. trade policy toward China should focus on intensifying and broadening ongoing bilateral dialogues and trade negotiations, such as the U.S.-China Strategic and Economic Dialogue (S&ED), which was established in part to discuss global and bilateral economic and trade issues. Another objective often cited is to complete ongoing bilateral and plurilateral negotiations involving China that would produce agreements expanding market access in China, including a U.S.-China bilateral investment treaty (BIT), China's accession to the WTO's Procurement Agreement (GPA), and a WTO plurilateral environment goods agreement (EGA).

This report provides background and analysis of U.S.-China commercial ties, including history, trends, issues, and outlook.

Introduction

Economic and trade reforms begun in 1979 have helped transform China into one of the world's fastest-growing economies. China's economic growth and trade liberalization, including comprehensive trade commitments made upon its entry to the World Trade Organization (WTO) in 2001, have led to a sharp expansion in U.S.-China commercial ties. Yet, bilateral trade relations have become increasingly strained in recent years over a number of issues, including a large and growing U.S. trade deficit with China, resistance by China to appreciate its currency to market levels, China's mixed record on implementing its WTO obligations, infringement of U.S. intellectual property (including through cyber theft of U.S. trade secrets), and numerous Chinese industrial policies that appear to impose new restrictions on foreign firms or provide unfair advantages to domestic Chinese firms (such as subsidies). As a presidential candidate, Donald Trump pledged to take a tougher stance against China to induce it to eliminate trade and economic policies deemed harmful to U.S. economic interests and/or inconsistent with WTO rules. This report provides an overview of U.S.-China commercial relations, including major trade disputes.

Most Recent Developments

U.S.-China commercial ties are increasingly complex and at times contentious, as reflected in the recent developments summarized below.

- On January 12, 2017, the U.S. Trade Representative (USTR) announced that it had filed a WTO dispute settlement case against China over subsidies given to certain Chinese aluminum producers.

- On January 6, 2017, the President's Council of Advisors on Science and Technology issued a report on U.S. semiconductor innovation, competitiveness, and security, which warned that a "concerted push by China to reshape the market in its favor, using industrial policies backed by over one hundred billion dollars in government-directed funds, threatens the competitiveness of U.S. industry and the national and global benefits it brings." |1|

- On December 15, 2016, the USTR announced that it had initiated a WTO dispute settlement case against China over its administration of tariff-rate quotas (TRQs) for rice, wheat, and corn.

- On December 12, 2016, China initiated a WTO dispute resolution case against the United States (as well as the European Union) over its continued treatment of China as a non-market economy for the purposes of calculating and applying antidumping measures.

- From November 21-23, 2016, the 27th session of the U.S.-China Joint Commission on Commerce and Trade (JCCT) was held in Washington, DC. Several Chinese trade policies were discussed, including market access for agricultural products (including biotech approvals), indigenous innovation policies, pharmaceutical and medical device market access, semiconductor policies, overcapacity in China's steel and aluminum industries, competition policies, and IPR protection.

- A report by the U.S. Chamber of Commerce released on November 11, 2016, estimated that U.S. agricultural exports to China could increase by an additional $17.6 billion (or 40%) from 2016 to 2025 if Chinese agricultural trade barriers were eliminated.

- On September 13, 2016, the United States initiated a WTO dispute settlement case against China over its use of excessive domestic subsidies for rice, wheat, and corn.

- On September 3, 2016, President Obama held a bilateral meeting with Chinese President Xi a day before the start of the G-20 summit in Hangzhou, China. They discussed a number of global, regional, and bilateral subjects, including cybersecurity. At the G-20 summit, major topics included excess capacity in steel and other industries, currency policy, the environmental goods agreement, international cooperation on taxation and corruption, and promoting innovation and the digital economy.

- On August 10, 2016, an international coalition of 46 business groups sent a letter to Chinese Premier Li Keqiang calling on China to address growing concerns over its growing restrictive policies on foreign technology, especially information communications technology.

- At the WTO's Council on Trade in Goods held on July 14, 2016, China requested all WTO members to extend it market economy status (MES) for the purposes of antidumping measures by December 11, 2016, arguing that its 2001 WTO protocol of accession included a provision mandating this change. The United States responded by asserting that the cited WTO provision does not automatically grant China MES, but rather, that status should be determined by the "facts on the ground" relative to each WTO member's domestic laws and rules for making such an assessment.

- On July 13, 2016, the United States initiated a WTO dispute settlement case against China over its export duties on 15 different raw materials.

- From June 5 to 7, 2016, the United States and China held their 8th round of talks under the U.S.-China Security and Economic Dialogue (S&ED).

- On June 2, 2016, the United States at the WTO Committee on Trade-Related Investment Measures urged China to delay or suspend draft regulations that would require insurance companies operating in China to use information and communication technology (ICT) products that have been deemed by the government to be "secure and controllable."

U.S. Trade with China |2|

U.S.-China trade rose rapidly after the two nations reestablished diplomatic relations in January 1979, signed a bilateral trade agreement in July 1979, and provided mutual most-favored-nation (MFN) treatment beginning in 1980. |3| In that year (which was shortly after China's economic reforms began), total U.S.-China trade (exports plus imports) was approximately $4 billion; China ranked as the United States' 24rd-largest trading partner, 16th-largest export market, and 36th-largest source of imports. In 2016, total U.S. total merchandise trade with China was $579 billion, making China the United States' largest trading partner (see Table 1). The U.S.-China Business Council estimates that China is a $400 billion market for U.S. firms, based on U.S. merchandise and services exports to China, re-exports of U.S. goods from Hong Kong to China, and sales by U.S. affiliates in China.

Table 1. U.S. Merchandise Trade with China: 1980-2016

($ in billions)

Year U.S. Exports U.S. Imports U.S. Trade Balance 1980 3.8 1.1 +2.7 1990 4.8 15.2 -10.4 2000 16.3 100.1 -83.8 2010 91.9 365.0 -273.0 201 1 104.1 399.4 -295.3 2012 1 10.5 425.6 -315.1 2013 121.7 440.4 -318.7 2014 123.6 468.5 -344.9 2015 1 16.1 483.2 -367.2 2016 1 15.8 462.8 -347.0 Source: U.S. International Trade Commission (USITC) DataWeb.

U.S. Merchandise Exports to China

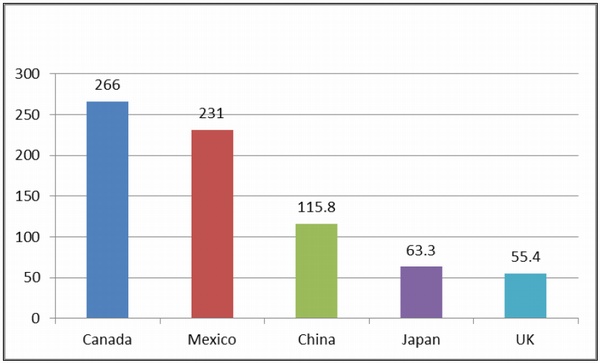

U.S. merchandise exports to China in 2016 were $115.8 billion, down 0.3% over the previous year (they fell by 6.1% in 2015), due in part to the effects of a slowing Chinese economy. |4| In 2016, China was the third-largest U.S. merchandise export market after Canada and Mexico (see Figure 1). From 2000 to 2016, the share of total U.S. merchandise exports going to China rose from 2.1% to 8.0%. As indicated in Table 2, the top five merchandise U.S. exports to China in 2016 were (1) oil seeds and grains (mainly soybeans); (2) aerospace products (mainly civilian aircraft and parts); (3) motor vehicles; (4) semiconductors and electronic components; and (5) navigational, measuring, medical, and controlling instruments. As indicated in Table 3, from 2001 to 2016, U.S. exports to China increased by 511%, which was by far the fastest growth rate for U.S. exports to any of its top 10 export markets. China was the second-largest U.S. agricultural export market in 2016 at $21.4 billion, two-thirds of which consisted of soybeans.

Figure 1. Top 5 U.S. Merchandise Export Markets in 2016

($ in billions)

Source: USITC Dataweb.

Table 2. Major U.S. Exports to China in 2016

($millions and percentage change)

NAIC Number NAIC Description (4-digit level) 2014 2015 2016 Percent Change 2015-2016 1111 OILSEEDS & GRAINS 16,285 13,034 15,533 19.2% 3364 AROSPACE PRODUCTS & PARTS 13,932 15,445 14,578 -5.6% 3361 MOTOR VEHICLES 1 1,248 9,224 8,942 -3.1% 3344 SEMICONDUCTORS & OTHER ELECTRONIC COMPONENTS 6,453 6,925 6,892 -0.5% 3345 NAVIGATIONAL, MEASURING, MEDICAL, AND CONTROL INSTRUMENTS 5,442 5,459 5,525 1.2% 9100 WASTE AND SCRAP 7,088 5,945 5,172 -13.0% 3251 BASIC CHEMICALS 4,486 4,548 4,592 1.0% 3252 RESIN, SYN RUBBER, ARTF & SYN FIBERS/FIL 4,298 3,738 3,564 -4.6% 3339 OTHER GENERAL PURPOSE MACHINERY 3,385 3,106 3,001 -3.4% 3254 PHARMACEUTICALS & MEDICINES 2,206 2,510 2,702 7.6% Total 123,621 116,072 115,775 -0.3% Source: NAIC Description (4-digit level)

Notes: NAIC is the North American Industrial Classification system.Table 3. Major U.S. Merchandise Export Markets: 2001-2016

($billions and percentage change)

Country 2001 2016 Percent Change 2016/2001 Canada 164 266 62.2% Mexico 102 231 126.5% China 19 116 510.5% Japan 58 64 10.3% United Kingdom 41 55 34.1% Germany 30 49 63.3% South Korea 22 42 90.9% Netherlands 20 40 100.0% Hong Kong 14 35 150.0% Belgium 14 32 128.6% Total 731 1,454 98.9% Source: USITC DataWeb and Global Trade Atlas.

Note: Ranked according to the top 10 U.S. merchandise export markets in 2016.Many trade analysts argue that China could prove to be a much more significant market for U.S. exports in the future. China is one of the world's fastest-growing economies, and healthy economic growth is projected to continue in the years ahead, provided that it implements new comprehensive economic reforms. China's goals of modernizing its infrastructure, rebalancing the economy, upgrading industries, boosting the services sector, and enhancing the social safety net could generate substantial new demand for foreign goods and services. Economic growth has substantially improved the purchasing power of Chinese citizens, especially those living in urban areas along the east coast of China. In addition, China's large foreign exchange reserves (at $3.0 trillion as of January 2017) and its huge population (at 1.38 billion) make it a potentially enormous market. To illustrate:

- Although Chinese private consumption as a percentage of GDP is much lower than that of most other major economies, the rate of growth of Chinese private consumption has been rising rapidly. From 2007 to 2016, China's private consumption grew at an average annual rate of 8.9%, compared to 1.6% growth in the United States. |5|

- In 2015, there were 2.6 million Chinese visitors to the United States (up 18.3% over the previous year), ranking China as the fifth-largest source of foreign visitors to the United States. |6| According to U.S. Department of Commerce projections, by 2020, this figure will rise to 5.0 million, making China the third-largest source of international travelers to the United States after Canada and Mexico. |7|

- China has the world's largest mobile phone network with 1.3 billion mobile phone subscribers as of June 2016. |8|

- E-Marketer, a research firm, estimated that China's e-commerce sales in 2015 totaled $672 billion (nearly double the U.S. level) and projected sales would surge to nearly $2 trillion by 2019. |9|

- Boeing Corporation delivered 145 planes to China in 2015. Boeing predicts that over the next 20 years (2015-2034), China will need 6,330 new airplanes valued at $950 billion, and will be Boeing's largest commercial airplane customer outside the United States. |10| During Chinese President Xi Jinping's visit to the United States in September 2015, China announced plans to buy 300 aircraft valued at $38 billion.

- China replaced the United States as the world's largest Internet user in 2008. As of June 2016, China had an estimated 721 million Internet users, double the U.S. population. Yet, the percentage of the Chinese population using the Internet is small relative to the United States: 52% versus 87%, respectively. |11|

- General Motors (GM) reported that it sold more cars and trucks in China than in the United States each year from 2010 to 2016. |12| GM's China sales in 2016 were 3.9 million vehicles, compared to 3.0 million vehicle sales in the United States. Equity income from GM's joint venture operations in China was $2.0 billion in 2016. GM vehicle unit sales to China accounted for 38.7% of its global total. |13| GM expects China's vehicle market to increase by 5 million units or more by 2020. |14| In addition, U.S. motor vehicle exports to China rose by 51.7% from 2012 to 2016. These totaled $8.7 billion in 2016, making China the second-largest U.S. motor vehicle export market after Canada. |15|

- According to estimates by Credit Suisse (a global financial services company), in 2015 China overtook the United States to become the country with the largest middle class at 109 million adults (with wealth between $50,000 and $500,000); the U.S. level was estimated at 92 million. |16|

- A January 2017 study prepared by Oxford Economics for the U.S.-China Business Council estimated that U.S. exports of goods and services to China, plus bilateral FDI flows, directly and indirectly supported 2.6 million U.S. jobs and contributed $216 billion to U.S GDP. The study further predicted that U.S. exports of goods and services to China would exceed $520 billion by 2030. |17|

Major U.S. Merchandise Imports from China

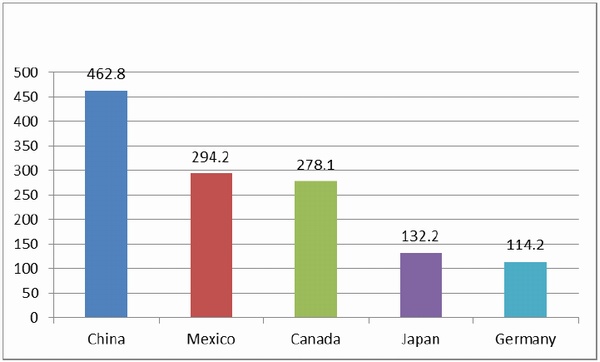

China was the largest source of U.S. merchandise imports in 2016, at $462.3 billion, down 4.2% from the previous year. |18| China's share of total U.S. merchandise imports rose from 8.2% in 2000 to 21.1% in 2016. The importance (ranking) of China as a source of U.S. imports has risen sharply, from eighth largest in 1990, to fourth in 2000, to second in 2004-2006, and to first in 2007-present (see Figure 2). The top five U.S. imports from China in 2016 were communications equipment; computer equipment; miscellaneous manufactured commodities (such as toys and games); apparel; and semiconductors and other electronic components (see Table 4). China was also the third-largest source of U.S. agricultural imports in 2016 at $6.2 billion.

Figure 2. Major Sources of U.S. Merchandise Imports: 2016

($ in billions)

Source: USITC DataWeb.

Table 4. Major U.S. Merchandise Imports From China in 2016

($millions and percentage change)

NAIC Number NAIC Description (4-digit level) 2014 2015 2016 Percent Change 2015-2016 3342 COMMUNICATIONS EQUIPMENT 64,236 67,349 65,676 -2.5% 3341 COMPUTER EQUIPMENT 67,201 63,433 57,377 -9.5% 3399 MISCELLANEOUS MANUFACTURED COMMODITIES 33,601 35,805 34,916 -2.5% 3152 APPAREL 27,146 27,512 25,145 -8.6% 3344 SEMICONDUCTORS & OTHER ELECTRONIC COMPONENTS 22,458 23,327 22,449 -3.8% 3371 HOUSEHOLD & INSTITUTIONAL FURNITURE & KITCHEN CABINETS 14,018 15,738 16,370 4.0% 3162 FOOTWEAR 16,842 17,067 14,624 -14.3% 3343 AUDIO & VIDEO EQUIPMENT 14,645 14,882 13,887 -6.7% 3363 MOTOR VEHICLE PARTS 12,213 13,575 13,417 -1.2% 3352 HOUSEHOLD APPLIANCES AND MISCELANEOUS MACHINES, NESOI 12,205 13,290 12,344 -7.1% Total 468,484 483,245 462,813 -4.2% Source: USITC Dataweb.

Notes: NAIC is the North American Industrial Classification system.Throughout the 1980s and 1990s, nearly all U.S. imports from China were low-value, labor-intensive products, such as toys and games, consumer electronic products, footwear, and textiles and apparel. However, over the past few years, an increasing proportion of U.S. imports from China have been comprised of more technologically advanced products (see text box below).

U.S.-China Trade in Advanced Technology Products According to the U.S. Census Bureau, U.S. imports of "advanced technology products" (ATP) from China in 2016 totaled $147.6 billion. Information and communications products were the largest U.S. ATP import from China. ATP products accounted for 331.9% of total U.S. merchandise imports from China. In addition, 34.4% of total U.S. ATP imports were from China (compared with 14.1% in 2003). U.S. ATP exports to China in 2016 were $33.4 billion; these accounted for 28.8% of total U.S. exports to China and 9.7% of U.S. global ATP exports. In comparison, U.S. ATP exports to China in 2003 were $8.3 billion, which accounted for 29.2% of U.S. exports to China and 4.6% of total U.S. ATP exports.

The United States ran a $ 1 14.2 billion deficit in its ATP trade with China in 2016, up from a $21.0 billion deficit in 2003. Some see the large and growing U.S. trade deficit in ATP with China as a source of concern, contending that it signifies the growing international competitiveness of China in high technology. Others dispute this, noting that a large share of the ATP imports from China are in fact relatively low-end technology products and parts, such as notebook computers, or are products that are assembled in China using imported high technology parts that are largely developed and/or made elsewhere.

Trade in Services

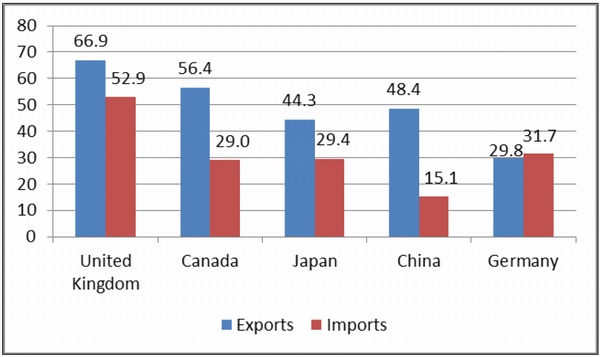

China is a major U.S. trading partner in services. In 2015, China was the 4th-largest services trading partner at $63.6 billion, the 3rd-largest services export market at $48.4 billion, and the 11th-largest source of services imports at $15.1 billion (see Figure 3). |19| The United States ran at $33.3 billion services trade surplus with China, which was the largest services surplus of any U.S. trading partner.

Figure 3. Major U.S. Services Trading Partners in 2015

($ in billions)

Source: BEA.

Notes: Ranked according to total trade in services in 2015.The U.S. Merchandise Trade Deficit with China

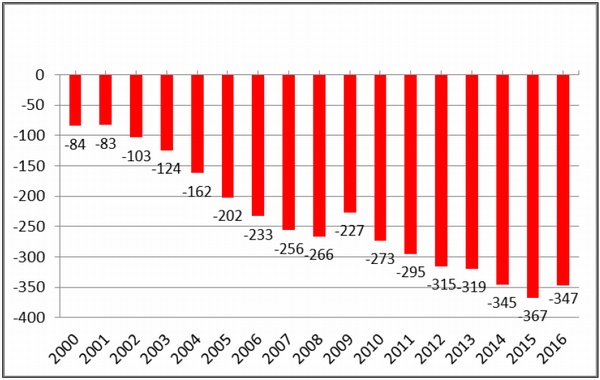

A major concern among some U.S. policymakers is the size of the U.S. merchandise trade deficit with China, which rose from $10 billion in 1990 to $367 billion in 2015 (see Figure 4). The deficit fell to $347 billion in 2016. For the past several years, the U.S. merchandise trade deficit with China has been significantly larger than that with any other U.S. trading partner (see Figure 5). Some analysts contend that the large U.S. merchandise trade deficits with China indicate that the trade relationship is somehow unbalanced, unfair, and damaging to the U.S. economy. Others argue the large U.S. trade deficit with China is more of a reflection of global shifts in production as well as the emergence of extensive and complex supply chains, where China is often the final point of assembly for export-oriented multinational firms that source goods from multiple countries.

Figure 4. U.S. Merchandise Trade Balance with China: 2000-2016

($ in billions)

Source: USITC DataWeb.

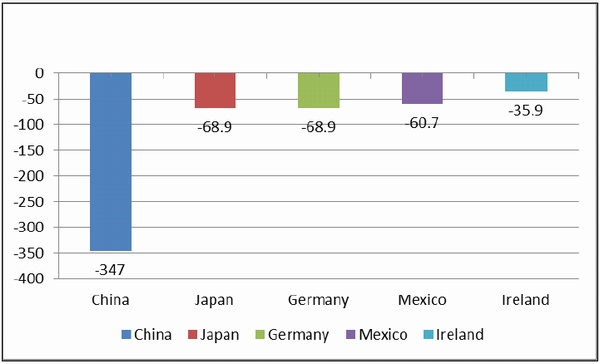

Figure 5. Five Largest U.S. Merchandise Trade Imbalances in 2016

($ in billions)

Source: USITC DataWeb.

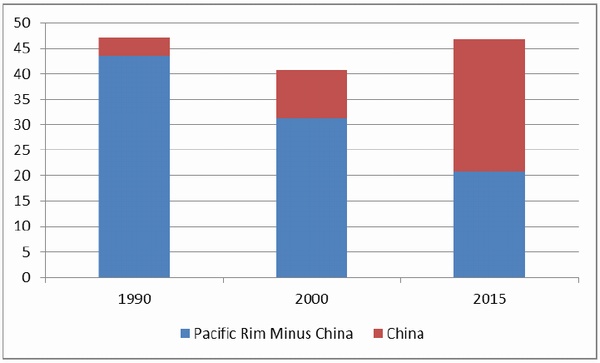

The Transfer of Pacific Rim Production to China by Multinational Firms

Many analysts contend that the sharp increase in U.S. imports from China (and hence the growing bilateral trade imbalance) is largely the result of movement in production facilities from other (primarily Asian) countries to China. That is, various products that used to be made in such places as Japan, Taiwan, Hong Kong, etc., and then exported to the United States, are now being made in China (in many cases, by foreign firms in China). To illustrate, in 1990, 47.1% of the value of U.S. manufactured imports came from Pacific Rim countries (including China); this figure remained relatively unchanged in 2015 at 46.8% in 2015. |20| Over this period, the share of total U.S. manufactured imports that came from China rose from 3.6% to 26.1%. In other words, while China was becoming an increasingly important source for U.S. manufactured imports, the relative importance of the rest of the Pacific Rim (excluding China) as a source of U.S. imports was declining, in part because many multinational firms were shifting their export-oriented manufacturing facilities to China (see Figure 6). In 1990, China accounted for 7.6% of U.S. manufactured imports from all Pacific Rim countries, but by 2015, this figure had risen to 55.8%.

Source: USITC DataWeb.

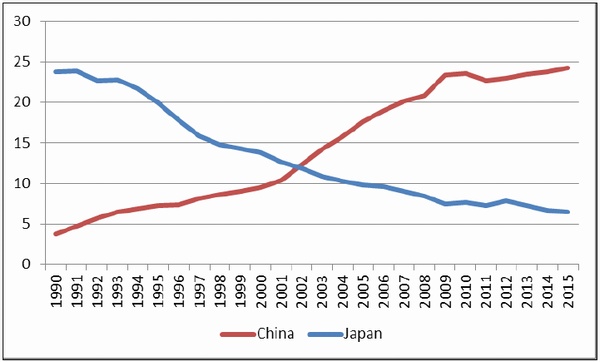

Notes: Standard International Trade Classification (SITC) definition of manufactured imports.A significant amount of the shift of production involved Japan. In 1990, Japan was the source of 23.8% of U.S. manufactured imports, but by 2015 this level had dropped to 6.5%. Conversely, China's share of U.S. manufactured imports rose from 3.8% to 24.3% (see Figure 7). Japan accounted for the single largest U.S. bilateral merchandise trade deficit for many years until it was overtaken by China in 2000.

Figure 7. U.S. Manufactured Imports from China and Japan as a percentage of U.S. Total: 1999-2015 (%)

Source: USITC DataWeb.

China as a Major Center for Global Supply Chains

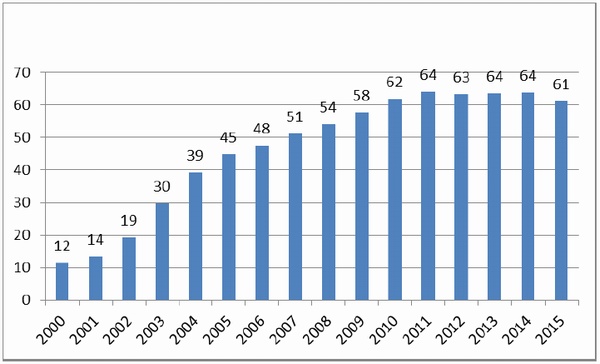

Another illustration of the shift in Asian production can be seen in the case of U.S. computer equipment imports, which constitute the largest category of U.S. imports from China (on an NAIC basis, 4-digit level). In 2000, Japan was the largest foreign supplier of U.S. computer equipment (with a 19.6% share of total U.S. imports), while China ranked fourth (with a 12.1% share). By 2015, Japan's ranking had fallen to fourth; the value of its shipments dropped by 75.4% over 2000 levels, and its share of U.S. computer imports declined to 3.2% (2015). China was by far the largest foreign supplier of computer equipment in 2015 with a 61.4% share of total U.S. computer equipment imports, compared to 12.0% in 2000 (see Figure 8). |21| While U.S. imports of computer equipment from China from 2000 to 2015 increased by 668.3%, the total value of U.S. computer imports worldwide rose by only 50.4%. |22| Taiwan, one of the world's leaders in sales of information and communications technology (ICT), produces over 93% of such products in China. Computer equipment, like many other globally traded products, often involves many stages of production, using parts and other inputs made by numerous multinational firms throughout the world, a significant share of which is currently assembled in China. The globalization of supply chains makes it increasingly difficult to interpret conventional U.S. trade statistics.

Figure 8. U.S. Computer Imports from China as a Percentage of Total U.S. Computer Imports: 2000-2015

(percentage)

Source: USITC DataWeb.

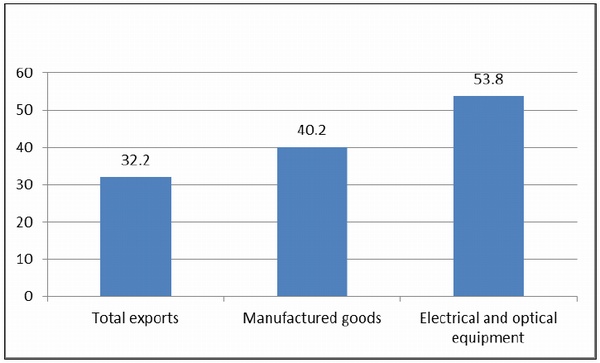

A joint study by the Organization for Economic Cooperation and Development (OECD) and the WTO has sought to estimate trade flows according to the value that was added in each country. For example, the OECD/WTO study estimated that in 2011, 32.2% of the overall value of China's gross exports was comprised of foreign imports. This level increases to 40.2% for China's total manufactured exports, and for electrical and optical equipment, it was 53.8% (see Figure 9). The study estimated that if bilateral trade imbalances were measured according to the value of trade that occurred domestically in each country, the U.S. trade deficit (in goods and services) with China in 2011 (the most recent year available) would decline by 35% (from $278.6 billion to $181.1 billion). This is largely because of the role of intermediates trade (parts and materials imported to make products). For example, the World Bank estimates that U.S. intermediate exports and imports to and from China in 2015 were $18.7 billion and $32.5 billion, respectively. |23| Thus, many Chinese products contain U.S.-made inputs and some U.S. products contain Chinese-made inputs.

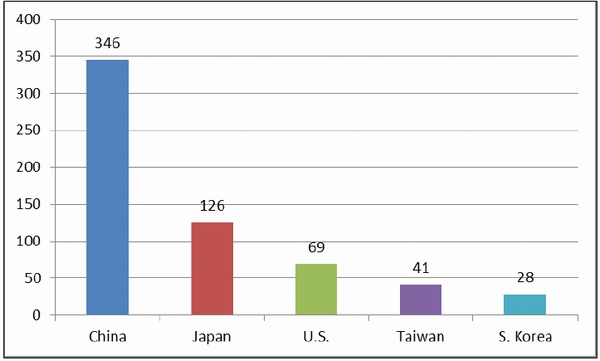

According to Apple Corporation, it utilized over 200 corporate suppliers with 766 facilities located around the world. The top five largest country sources of these facilities in 2015 were China (346), Japan (126), the United States (69), Taiwan (41), and South Korea (28) (see Figure 10). Some U.S. corporate suppliers to Apple have facilities located in many countries. For example, Intel Corporation has 10 facilities that supply products to Apple, of which, four are located in the United States, two each in China, and one each in Ireland, Israel, Malaysia, and Vietnam. |24| Apple iPhones are mainly assembled in China by Taiwanese companies (Foxconn and Pegatron), using a number of intermediate goods imported from abroad (or in many cases intermediates made by foreign firms in China). Many analysts have estimated that the value-added that occurs in China in the production of the iPhone is small relative to the total value of the product because it mainly involves assembling foreign-made or foreign-owned components. Apple Corporation, on the other hand, is thought to be the single largest beneficiary (in terms of gross profit) of the sale of the iPhone. However, conventional trade data do not accurately attribute the value-added that occurs in each stage of making the iPhone. Rather, when the United States imports iPhones from China, U.S. trade data attributes nearly the full value of the product as originating in China, which, some argue artificially inflates the size of the U.S. trade deficit with China.

One 2010 study estimated that in 2009, China exported 11.3 million iPhones to the United States, with a shipping price of $179 per unit and total export value at $2.0 billion. The study estimated that 96.4% of the value of iPhone was attributed to foreign suppliers and producers of components and parts, including the United States (at $122 million). Standard trade data would put China's trade surplus in iPhone trade with the United States at $1.9 billion, but that level would fall to $73.5 million if that trade was measured according to the value-added that occurred in each country. |25| Several analysts have concluded that Apple's innovation in developing and engineering its products and its ability to source most of its production in low-cost countries, such as China, has helped enable Apple to become a highly competitive and profitable firm (as well as a source for high-paying jobs in the United States). |26| Apple products illustrate that the rapidly changing nature of global supply chains has made it increasing difficult to interpret the implications of U.S. trade data because, while they may show where products are being imported from, they often fail to reflect who benefits from that trade.

Figure 9. Estimated Percentage Foreign Value-Added to China's Exports in 2011

Source: OECD/WTO Trade in Value-Added, October 2015.

Figure 10. Top Five Country Sources of Facilities that Supply Apple Corporation in 2015

Source: Apple Corporation 2015 supplier list.

Note: Includes suppliers of materials, manufacturing, and assembly of products worldwide.Jobs and Trade

Measuring or assessing the benefits and costs of growing U.S.-China economic ties is often hotly debated among U.S. policymakers and economists, particularly in regard to its impact on various manufacturing sectors and workers (see Text Box).

China and U.S. Jobs The impact on U.S. employment (especially in various manufacturing sectors) resulting from imports from China (particularly after it joined the WTO in 2001) has been a major point of contention. Some critics of U.S. trade policy toward China attempt to link U.S. job losses to the growth and size of U.S. imports from China and/or the bilateral trade imbalance. For example, a study by the Economic Policy Institute (EPI) in December 2014 claims that growth in the U.S. goods trade deficit with China between 2001 and 2013 "eliminated or displaced" 3.2 million U.S. jobs (three-fourths of which were in manufacturing). |27| The authors stated that they used an input-output model that "estimated the amount of labor, or number of jobs, that is required to produce a given volume of exports and the labor displaced when a given volume of imports is substituted for domestic output." The difference between the two numbers is thus the estimated jobs displaced by the trade deficit. Critics of the EPI study argue that the methodology used is flawed. First, the study essentially takes the Department of Commerce's estimates of the number of jobs "supported" by each $1 billion exports (5,805 in 2013) |28| and makes the assumption that each $1 billion in imports must displace the same level of jobs, a notion that most economists would disagree with. For example, not all imports from China compete directly with U.S. producers. Many are products that used to be made in other countries, and thus an increase in imports from China alone did not necessarily displace U.S. domestic producers. In addition, some imports from China contain U.S.-made intermediate parts (such as semiconductors) made in the United States. Many imports from China are final assembled products (such as Apple iPhones) with a relatively small share of value-added from China, and the jobs generated or supported by innovating the products are not accounted for in the trade data. Finally, factors other than trade, such as technological innovation, may also affect job levels in some sectors.

Similarly, while China is the largest source of U.S. merchandise imports, the overall impact on the U.S. economy is relatively small. A Federal Reserve Bank of San Francisco study examined U.S. consumer spending and estimated that, in 2010, U.S. personal consumption expenditures (PCE) of domestically sourced goods and services goods was 88.5% of total U.S. PCE (total imports accounted for 11.5%). Imports from China accounted for 2.7% of U.S. PCE, but less than half of this amount was attributed to the actual cost (price) of Chinese imports--the rest went to U.S. businesses and workers transporting, selling, and marketing the Chinese-made products, which, the study estimated, would reduce China's share of U.S. PCE to l.9%. |29|

Economists generally argue that trade has an overall positive impact on the economy. Low-cost imports boost consumer welfare, increase consumer choices, and help lower inflation. However, some economists contend that the benefits of trade are not equally spread. Some sectors can be negatively impacted, affecting employment and wages, and such negative effects can be concentrated in certain regions or industries, and adjusting to such shocks can be challenging. A 2014 study by the National Bureau of Economic Research (NBER) concluded that increased import penetration from China from 1999 to 2011 directly and indirectly resulted in net U.S. job losses of 2.0 million to 2.4 million U.S. jobs, and accounted for 10% of the decline in U.S. manufacturing jobs during this period. |30| Another NBER study asserted that China's rise as an economic power has "induced an epochal shift in patterns of world trade" and has "challenged much of the received empirical wisdom about how labor markets adjust to trade shocks." The study said that for workers in import-competing firms, "adjustment in local labor markets is remarkably slow, with wages and labor-force participation rates remaining depressed and unemployment rates remaining elevated for at least a full decade after the China trade shock commences. Exposed workers experience greater job churning and reduced lifetime income," in part because workers that may lose their jobs due to imports often remain in highly exposed industries or regions, which are subject to further trade shocks. |31| The study claimed that there is little evidence for substantial off-setting employment gains in local industries not exposed to the trade shock. Critics of the two NBER studies contend that while trade may impact the composition of jobs in the U.S. economy, it has little long-term effect on the number of jobs, which they argue is largely a function of aggregate demand. They also point out that between 2010 and 2015, the number of U.S. manufacturing jobs rose by 6.8% even though U.S. imports from China increased by 32.4%. In addition, U.S. manufacturing output during this period rose by 15.3%. Some economists contend that U.S. productivity has been a major cause of job losses in manufacturing. A study by Ball State University attributed 88% of U.S. manufacturing job losses from 2000 to 2010 to productivity gains, noting that had the United States "kept 2000-levels of productivity and applied them to 2010-levels of production, we would have required 20.9 million manufacturing workers. Instead, we employed only l2.l million." |32|

U.S.-China Investment Ties: Overview

Investment plays a large and growing role in U.S.-China commercial ties. |33| China's investment in U.S. assets can be broken down into several categories, including holdings of U.S. securities, foreign direct investment (FDI), and other non-bond investments. The Department of the Treasury defines foreign holdings of U.S. securities as "U.S. securities owned by foreign residents (including banks and other institutions) except where the owner has a direct investment relationship with the U.S. issuer of the securities." |34| U.S. statutes define FDI as "the ownership or control, directly or indirectly, by one foreign resident of 10% or more of the voting securities of an incorporated U.S. business enterprise or the equivalent interest in an unincorporated U.S. business enterprise, including a branch." |35| The Bureau of Economic Analysis (BEA) is the main U.S. government agency that collects and reports data on FDI flows to and from the United States, which is done on a balance of payment basis. |36| China has also invested in a number of U.S. companies, projects, and various ventures which do not meet the U.S. definition of FDI, and thus, are not reflected in BEA's data.

Chinese overseas investment has largely been driven by its accumulation of foreign exchange reserves (FERs), which totaled $3.12 trillion as of October 2016, by far the world's largest. China's large FERs have mainly been a function of large annual trade surpluses and FDI inflows, as well as past intervention by the Chinese government to halt or slow the renminbi's appreciation (discussed later in the report) and restrictions on capital outflows by private Chinese citizens. Rather than holding foreign currencies, such as U.S. dollars, which earn no interest, the Chinese government has invested much of those reserves abroad. For many years, much of that investment has gone into U.S. Treasury securities, which have been viewed as a relatively safe investment (as they are backed by the full faith and credit of the U.S. government) and liquid (e.g., easily sold), albeit generating relatively small rates of returns. More recently, the Chinese government has diversified its investments in order to obtain higher returns, such as by encouraging its firms (especially state-owned enterprises) to invest overseas to become more globally competitive, as well as to help China gain access to raw materials (such as oil), food, and technology. As a result, Chinese annual FDI outflows have grown significantly in recent years, rising from $21 billion in 2006 to $128 billion in 2015, making China the third-largest source of annual global FDI outflows. |37|

U.S. investment in China has largely been in the form of FDI flows. Initially, most U.S. FDI in China after it began its market reforms in 1979 likely went toward export-oriented manufacturing to take advantage of China's relatively low wages. In more recent years, as China's economy has rapidly grown, a larger share of U.S. FDI in China has gone to tap into China's booming domestic demand for goods and services. However, many U.S firms raise concerns that Chinese investment restrictions and requirements often hamper their efforts.

China's Holdings of U.S. Public and Private Securities |38|

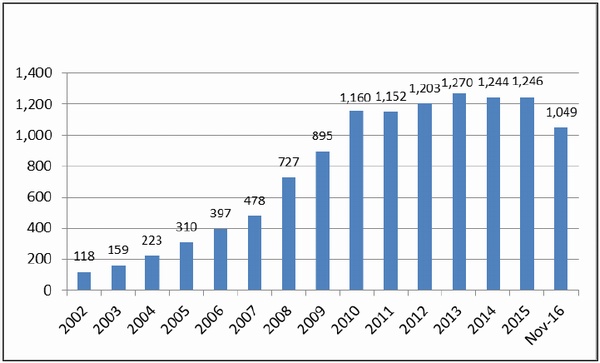

China's holdings of U.S. public and private securities are significant and by far constitute the largest category of Chinese investment in the United States. |39| These securities include U.S. Treasury securities, U.S. government agency (such as Freddie Mac and Fannie Mae) securities, corporate securities, and equities (such as stocks). China's investment in public and private U.S. securities totaled $1.84 trillion as of June 2015, making China the second-largest holder after Japan. |40| U.S. Treasury securities, which help the federal government finance its budget deficits, are the largest category of U.S. securities held by China. |41| As indicated in Table 5 and Figure 11, China's holdings of U.S. Treasury securities increased from $118 billion in 2002 to $1.24 trillion in 2014, but fell to $1.05 trillion as of November 2016, making it the second-largest foreign holder of U.S. Treasury securities after Japan. |42| China's holdings of U.S. Treasury securities as a share of total foreign holdings rose from 9.6% in 2002 to a historical high of 26.1% in 2010 (year-end), but this level has since fallen, dropping to 17.6% as of November 2016. |43|

Table 5. China's Holdings of U.S. Treasury Securities: 2002-November 2016

2002 2004 2006 2008 2010 2012 2014 Nov 2016 China's holdings ($ billions) 118 223 397 727 1,160 1,203 1,244 1,049 China's holdings as a percentage of total foreign holdings 9.6% 12.1% 18.9% 23.6% 26.1% 23.0% 21.7% 17.6% Source: U.S. Department of the Treasury.

Note: Annual data are year-end. Data excludes Hong Kong and Macau which are treated separately.Some analysts and Members of Congress have raised concerns that China's large holdings of U.S. debt securities could give China leverage over U.S. foreign policy, including trade policy. They argue, for example, that China might attempt to sell (or threaten to sell) a large share of its U.S. debt securities as punishment over a policy dispute, which could damage the U.S. economy. Others counter that China's holdings of U.S. debt give it very little practical leverage over the United States. They argue that, given China's economic dependency on a stable and growing U.S. economy, and its substantial holdings of U.S. securities, any attempt to try to sell a large share of those holdings would likely damage both the U.S. and Chinese economies. Such a move could also cause the U.S. dollar to sharply depreciate against global currencies, which could reduce the value of China's remaining holdings of U.S. dollar assets. Analysts further note that, while China is the largest foreign owner of U.S. Treasury securities, those holdings accounted for only 6.5% of total U.S. public debt securities as of March 2016. |44|

Figure 11. China's Holdings of U.S. Treasury Securities: 2002-November 2016

($ in billions)

Source: U.S. Department of the Treasury.

Notes: Annual data are year-end. Data excludes Hong Kong and Macau which are treated separately.In the 112th Congress, the conference report accompanying the National Defense Authorization Act of FY2012 (H.R. 1540, P.L. 112-81) included a provision requiring the Secretary of Defense to conduct a national security risk assessment of U.S. federal debt held by China. The Secretary of Defense issued a report in July 2012, stating that "attempting to use U.S. Treasury securities as a coercive tool would have limited effect and likely would do more harm to China than to the United States. As the threat is not credible and the effect would be limited even if carried out, it does not offer China deterrence options, whether in the diplomatic, military, or economic realms, and this would remain true both in peacetime and in scenarios of crisis or war." |45|

Bilateral Foreign Direct Investment Flows

The level of foreign direct investment (FDI) flows between China and the United States is relatively small given the large volume of trade between the two countries. Many analysts contend that an expansion of bilateral FDI flows could greatly expand commercial ties. |46| BEA data on U.S.-China FDI (see Table 6) indicate that in 2015:

- U.S. FDI flows to China were $7.3 billion (down 4.2% from 2014 flows), making China the 10th-largest destination of U.S. FDI outflows.

- The stock of U.S. FDI in China on a historical-cost basis (i.e., the book value) through 2015 was $74.6 billion (up 10.4% over the previous year), making China the 14th-largest overall destination of U.S. FDI through 2015.

- Chinese FDI flows to the United States were $5.1 billion (up 155.2% over 2014 levels), making China the 12th-largest source of U.S. FDI inflows in 2015.

- At the end of 2015, the stock of Chinese FDI in the United States on a historical-cost basis, was $14.8 billion (up 49.5% over the previous year), making China the 19th-largest overall source of U.S. FDI through 2015. |47|

Table 6. Summary of BEA Data on U.S.-China FDI Flows: 2015

FDI Data Quantity ($ billions) Ranking of FDI Flows U.S. FDI flows to China in 2015 7.3 10th China FDI flows to U.S. in 2015 5.1 12th Stock of U.S. FDI in China through 2015 74.6 14th Stock of Chinese FDI in U.S. through 2015 14.8 19th Source: Bureau of Economic Analysis.

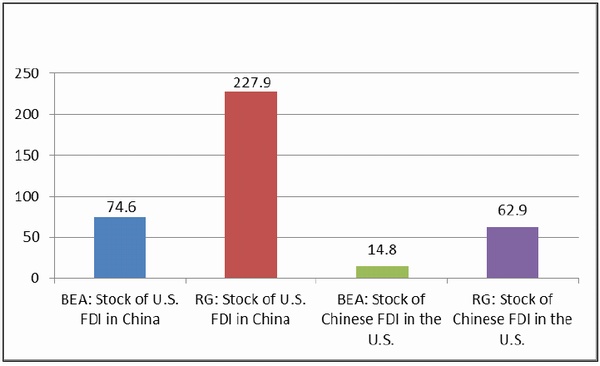

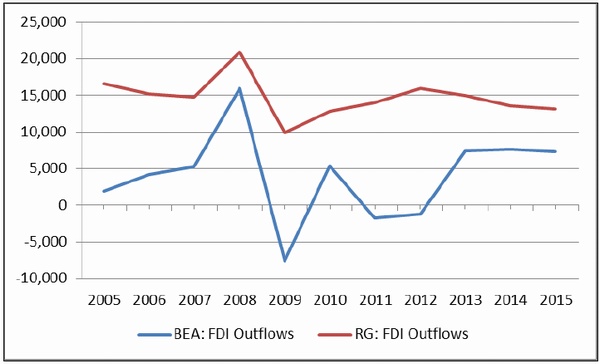

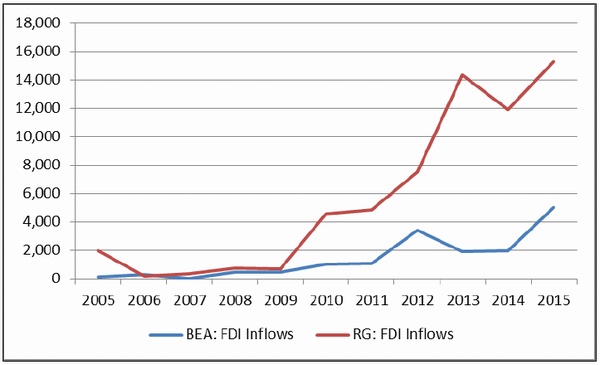

Notes: FDI stock data are on a historical-cost basis. Rankings were made using only countries and exclude broad groupings of territories or islands. Data for China exclude Hong Kong and Macau which are counted separately.The Rhodium Group, a private consulting firm, estimates Chinese FDI in the United States to be significantly higher than BEA estimates. The Rhodium Group notes that "Official data often exhibit a 1-2 year time lag and do not capture major trends, due to problems such as significant round tripping and trans-shipping of investments." |48| The Rhodium Group's approach is to calculate the full value of a Chinese acquisition in the year it was made and to attribute that acquisition to China if it was made by a Chinese entity, regardless of where the financing of the deal originated from (such as through Hong Kong and Caribbean offshore centers, which often occurs). |49| The Rhodium Group's data on U.S.-China FDI are much higher than BEA's data (see Figure 12, Figure 13, and Figure 14). |50| For example:

- The Rhodium Group's estimate of the stock of Chinese FDI in the United States through 2015, at $62.9 billion, is 325% higher than BEA's data (at $14.8 billion).

- The Rhodium Group's estimate of the stock of U.S. FDI in China, at $227.9 billion, is 205.5% higher than BEA's estimate (at $74.6 billion).

- The Rhodium Group puts Chinese FDI flows to the United States in 2015 at $15.3 billion, which was 200% higher than BEA's data ($5.1 billion). The Rhodium Group estimates China's FDI flows doubled from 2012 to 2015, while BEA's data show a 47.7% increase.

- The Rhodium Group's estimate of U.S. FDI flows to China in 2015 at $13.1 billion, which was 78.8% higher than BEA's data.

Figure 12. BEA and Rhodium Group Estimates of the Stock of U.S.-China FDI through 2015

($ in billions)

Source: Bureau of Economic Affairs and the Rhodium Group.

Note: BEA and the Rhodium Group use different methodologies to measure China's FDI in the United States.Figure 13. BEA and Rhodium Group Data on Annual U.S. FDI Flows to China: 2005-2015

($ in millions)

Source: BEA and Rhodium Group.

Notes: BEA and Rhodium Group methodologies for measuring FDI differ significantly.Figure 14. BEA and Rhodium Group Data on Chinese FDI Flows to the United States: 2005-2015

($ in millions)

Source: BEA and Rhodium Group.

Note: BEA and Rhodium Group methodologies for measuring FDI differ significantly.Chinese Restrictions on U.S. FDI in China

U.S. trade officials have urged China to liberalize its FDI regime in order to boost U.S. business opportunities in, and expand U.S. exports to, China. Although China is one of the world's top recipients of FDI, the Chinese central government imposes numerous restrictions on the level and types of FDI allowed in China. According to the U.S.-China Business Council (USCBC), China imposes ownership barriers on nearly 100 industries. |51| The OECD's 2014 FDI Regulatory Restrictiveness Index, which measures statutory restrictions on foreign direct investment in 57 countries (including all OECD and G-20 countries, and covering 22 sectors), ranked China's FDI regime as the most restrictive, based on foreign equity limitations, screening or approval mechanisms, restrictions on the employment of foreigners as key personnel, and operational restrictions (such as restrictions on branching, capital repatriation, and land ownership). |52|

Some recent surveys by U.S. business groups suggest that foreign firms in China may be less optimistic about the Chinese market than in the past, due in part to perceived growing protectionism. To illustrate:

- A September 2015 survey by USCBC noted that "American executives' confidence in their prospects in China continues to moderate, however, reflecting uncertainty about the direction of Chinese policies, limited progress on economic reforms, increased competition, and slowing growth." A quarter of companies cited Chinese policies and regulations as the primary constraint on increased profitability in China and 97% said they felt Chinese state-owned enterprises (SOEs) received preferences." |53|

- A 2016 American Chamber of Commerce in China (AmCham China) business climate survey of 500 member companies found that while a majority of respondents felt optimistic about their investments in China, 77% said that foreign businesses in China were less welcome in China than before, compared to 41% who asserted that in 2013. Inconsistent regulatory interpretation and unclear laws were cited by respondents as their biggest business challenge in China. |54|

- A 2016 European Union Chamber of Commerce in China business confidence survey stated that the business environment in China was becoming "increasingly hostile" and "perpetually tilted in favor of domestic enterprises." For example, among respondents, 56% said doing business in China was becoming more difficult and 57% claimed foreign companies tend to receive unfavorable treatment in China compared to domestic Chinese firms. |55|

Negotiations for a Bilateral Investment Treaty (BIT) |56|

The United States and China initiated negotiations on reaching a bilateral investment treaty (BIT) in 2008 with the goal of expanding bilateral investment opportunities. U.S. negotiators hope such a treaty would improve the investment climate for U.S. firms in China by enhancing legal protections and dispute resolution procedures, and by obtaining a commitment from the Chinese government that it would treat U.S. investors no less favorably than Chinese investors.

In April 2012, the Obama Administration released a "Model Bilateral Investment Treaty" that was developed to enhance U.S. objectives in the negotiation of new BITs. |57| The new model BIT address six core principles or issues for investors, including national treatment and most-favored nation (MFN) treatment at all stages of investment, rules on expropriations and compensation if this occurs, ability to transfer funds in and out of the country, limits on performance requirements (such as domestic content targets or mandated technology transfer), neutral arbitration of disputes, and freedom by investors to appoint their own senior officials. |58|

During the July 10-11, 2013, session of the S&ED, China indicated its intention to negotiate a high-standard BIT with the United States that would include all stages of investment and all sectors, a commitment a U.S. official described as "a significant breakthrough, and the first time China has agreed to do so with another country." |59| A press release by the Chinese Ministry of Commerce stated that China was willing to negotiate a BIT on the basis of nondiscrimination and a negative list, meaning the agreement would identify only those sectors not open to foreign investment on a nondiscriminatory basis (as opposed to a BIT with a positive list which would only list sectors open to foreign investment).

During the July 9-10, 2014, S&ED session, the two sides agreed to a broad timetable for reaching agreement on core issues and major articles of the treaty text and committed to initiate the "negative list" negotiation early in 2015. |60| During BIT negotiations held in June 2015, each side submitted their first negative list proposals, and later agreed to submit a revised list in September 2015 right before President Xi's summit visit to the United States, which they did, but a breakthrough was not achieved. New negative lists were submitted in June 2016 and August 2016, |61| and the BIT was discussed at the September 2016, G-20 Summit held in Hangzhou, China, but no breakthrough was announced. The original goal was to complete an agreement by the end of President Obama's term.

Many analysts contend the negotiation of a U.S.-China BIT could have significant implications for bilateral commercial relations and the Chinese economy. According to USTR Michael Froman, such an agreement would "offers a major opportunity to engage on China's domestic economic reforms and to pursue greater market access, a more level playing field, and a substantially improved investment environment for U.S. firms in China." |62| For China, a high-standard BIT could help facilitate greater competition in China and result in more efficient use of resources, factors which economists contend could boost economic growth. Some observers contend that China's pursuit of a BIT with the United States represents a strategy that is being used by reformers in China to jumpstart widespread economic reforms (which appear to have been stalled in recent years). This strategy, it is argued, is similar to that used by Chinese reformers in their efforts to get China into the WTO in 2001. Such international agreements may give political cover to economic reformers because they can argue that the agreements build on China's efforts to become a leader in global affairs. This may make it harder for vested interests in China who benefit from the status quo to resist change. Some critics raise concerns that even if a high standard BIT is reached, ensuring China's full compliance may prove difficult, given China's extensive use of industrial policies. Others have raised questions as to the effect of such an agreement in boosting FDI flows and how that might impact U.S. jobs in affected industries. |63| A BIT would have to be approved in the U.S. Senate by a two-thirds majority.

The U.S.-China Economic and Security Review Commission's (USCC's) November 2015 annual report recommended that the Administration provide a comprehensive, publicly available assessment of Chinese FDI in the United States prior to completion of BIT negotiations that includes an identification of the nature of investments, whether investments received support of any kind from the Chinese government and at any level, and the sector in which the investment was made. |64| The USCC's 2016 annual report recommended that Congress should "amend the statute authorizing the Committee on Foreign Investment in the United States to bar Chinese state-owned enterprises from acquiring or otherwise gaining effective control of U.S. companies." |65|

Major U.S.-China Trade Issues

China's economic reforms and rapid economic growth, along with the effects of globalization, have caused the economies of the United States and China to become increasingly integrated. |66| Although growing U.S.-China economic ties are considered by most analysts to be mutually beneficial overall, tensions have risen over a number of Chinese economic and trade policies that many U.S. critics charge are protectionist, economically distortive, and damaging to U.S. economic interests. According to the USTR, most U.S. trade disputes with China stem from the consequences of its incomplete transition to a free market economy. Major areas of concern for U.S. stakeholders include China's

- extensive network of industrial policies (including widespread use of trade and investment barriers, financial support, and indigenous innovation policies) that seek to promote and protect domestic sectors and firms, especially SOEs, deemed by the government to be critical to the country's future economic growth;

- failure to provide adequate protection of U.S. intellectual property rights (IPR) and (alleged) widespread government-directed cyber theft of U.S. trade secrets security to help Chinese firms;

- mixed record on implementing its WTO obligations; and

- government-directed financial policies that promote high savings (but reduce private consumption), encourage high fixed investment levels (but may contribute to overcapacity in many industries), and a managed exchange rate policy that may distort trade flows.

Chinese "State Capitalism"

Currently, a significant share of China's economy is thought to be driven by market forces. A 2010 WTO report estimated that the private sector now accounted for more than 60% of China's gross domestic product (GDP). |67| A 2016 WTO study estimated that the private sector accounted for 41.8% of China's exports. |68|

However, the Chinese government continues to play a major role in economic decisionmaking. For example, at the macroeconomic level, the Chinese government maintains policies that induce households to save a high level of their income, much of which is deposited in state-controlled Chinese banks. This enables the government to provide low-cost financing to Chinese firms, especially state-owned enterprises (SOEs). At the microeconomic level, the Chinese government (at the central and local government level) seeks to promote the development of industries deemed critical to the country's future economic development by using various policies, such as subsidies, tax breaks, preferential loans, trade barriers, FDI restrictions, discriminatory regulations and standards, export restrictions on raw materials (including rare earths), technology transfer requirements imposed on foreign firms, public procurement rules that give preferences to domestic firms, and weak enforcement of IPR laws.

Many analysts argue that the Chinese government's intervention in various sectors through industrial policies has intensified in recent years. The December 2013 USTR report on China's WTO trade compliance stated:

During most of the past decade, the Chinese government emphasized the state's role in the economy, diverging from the path of economic reform that had driven China's accession to the WTO. With the state leading China's economic development, the Chinese government pursued new and more expansive industrial policies, often designed to limit market access for imported goods, foreign manufacturers and foreign service suppliers, while offering substantial government guidance, resources and regulatory support to Chinese industries, particularly ones dominated by state-owned enterprises. This heavy state role in the economy, reinforced by unchecked discretionary actions of Chinese government regulators, generated serious trade frictions with China's many trade partners, including the United States. |69|

The extent of SOE involvement in the Chinese economy is difficult to measure, due to the opaque nature of the corporate sector in China and the relative lack of transparency regarding the relationship between state actors (including those at the central and non-central government levels) and Chinese firms. According to one study by the U.S.-China Economic and Security Review Commission:

The state sector in China consists of three main components. First, there are enterprises fully owned by the state through the State-owned Assets and Supervision and Administration Commission (SASAC) of the State Council and by SASACs of provincial, municipal, and county governments. Second, there are SOEs that are majority owners of enterprises that are not officially considered SOEs but are effectively controlled by their SOE owners. Finally, there is a group of entities, owned and controlled indirectly through SOE subsidiaries based inside and outside of China. The actual size of this third group is unknown. Urban collective enterprises and Government-owned Township and village enterprises (TVEs) also belong to the state sector but are not considered SOEs. The state-owned and controlled portion of the Chinese economy is large. Based on reasonable assumptions, it appears that the visible state sector--SOEs and entities directly controlled by SOEs, accounted for more than 40 percent of China's nonagricultural GDP. If the contributions of indirectly controlled entities, urban collectives, and public TVEs are considered, the share of GDP owned and controlled by the state is approximately 50 percent. |70|

According to the Chinese government, at the end of 2011, there were 144,700 state-owned or state-controlled enterprises at the central and local government level, excluding financial institutions, with total assets worth $13.6 trillion. |71| Chinese SOEs have undergone significant restructuring over the years. More than 90% of SOEs have reportedly become corporations or shareholding companies. |72| The Chinese government has identified a number of industries where the state should have full control or where the state should dominate. These include autos, aviation, banking, coal, construction, environmental technology, information technology, insurance, media, metals (such as steel), oil and gas, power, railways, shipping, telecommunications, and tobacco. |73|

Many SOEs are owned or controlled by local governments. According to one analyst:

The typical large industrial Chinese company is ...wholly or majority-owned by a local government which appoints senior management and provides free or low-cost land and utilities, tax breaks, and where possible, guarantees that locally made products will be favored by local governments, consumers, and other businesses. In return, the enterprise provides the local state with a source of jobs for local workers, tax revenues, and dividends. |74|

China's banking system is largely dominated by state-owned or state-controlled banks. In 2011, the top five largest banks in China, all of which were shareholding companies with significant state ownership, accounted for 57.5% of Chinese banking assets. The Chinese government also has four banks that are 100% state-owned and holds shares in a number of joint stock commercial banks. |75| SOEs are believed to receive preferential credit treatment by government banks, while private firms must often pay higher interest rates or obtain credit elsewhere. According to one estimate, SOEs accounted for 85% ($1.4 trillion) of all bank loans in 2009. |76|

Not only are SOEs dominant players in China's economy, many are quite large by global standards. Fortune's 2016 list of the world's 500 largest companies includes 103 Chinese firms (compared to 29 listed firms in 2007), the top 20 of which are listed in Table 7. |77|

Table 7. Top 20 Chinese Companies on Fortune's Global 500 in 2016

Company Global 500 Rank State or Private Industry Revenue ($billions) Assets ($billions) Employees (000s) State Grid 2 State Utility 330 $479 927.8 China National Petroleum 3 State Energy 299 621 1,590 Sinopec Group 4 State Energy 294 317 810.5 Industrial & Commercial Bank of China 15 State Banking 167 3,420 466.3 China Construction Bank 22 State Banking 148 2,826 369.2 China State Construction Engineering 27 State Engineering & Construction 140 166 241.5 Agricultural Bank of China 29 State Banking 133 2,740 508.7 Bank of China 35 State Banking 122 2,590 310.0 Ping An Insurance 41 Non-State Insurance 110 734 275.0 China Mobile Communications 45 State Telecommunications 107 251 436.7 SAIC Motor 46 State Motor Vehicles & Parts 107 79 92.8 China Life Insurance 54 State Insurance 101 466 130.8 China Railway Engineering 57 State Engineering & Construction 99 110 281.4 China Railway Construction 62 State Engineering & Construction 96 109 284.1 Dongfeng Motor Group 81 State Motor Vehicles & Parts 83 57 192.0 China Resources National 91 State General Merchandisers 77 153 447.3 China Southern Power 95 State Utilities 75 99 303.3 Pacific Construction Group 99 Non-State Engineering & Construction 73 43 351.7 China South Industries Group 102 State Aerospace & Defense 70 60 238.3 China Post Group 105 State Mail, Package, and Freight Delivery 70 1,157 938.5 Source: Fortune 2016 Global 500.

Of the 103 Chinese firms listed, Fortune identified 75 companies (73% of total) where the government owned 50% or more of the company. Together, these 75 firms in 2016 generated $7.2 trillion in revenues, had assets valued at $20.7 trillion, and employed 16.2 million workers. Of the 28 other Chinese firms on the Fortune 500 list, several appear to have financial links to the Chinese government. For example:

- Several of the listed firms are banks where the Chinese government owns a large or controlling share, including 26.5% of the Bank of Communications, 15.7% of China Minsheng Banking Corp., 21% of China Industrial Bank, 17.9% of China Merchant Bank, and 20% of Shanghai Pudong Development Bank. |78|

- Lenovo, a major global computer producer, was started by the Chinese National Academy of Social Sciences which started Legend Holdings in 1984. Lenovo was spun off from Legend in 2001, but Legend still owns 31% of Lenovo's shares. |79|

- Huawei (a major telecommunications company) describes itself as an employee-owned firm. However, many U.S. analysts contend that Huawei has strong links with the Chinese government, including the Chinese People's Liberation Army (PLA), and has not published a full breakdown of its ownership structure. In addition, in the past, the Chinese government reportedly ordered state banks to extend loans to the company early in its development so that it could compete against foreign firms in the domestic telecommunications market. |80|

- Ping An Insurance is the largest non-state company on the 2016 Global 500 list. In 2012, The New York Times published an article that reported that in 2004 a network of family and friends of then Chinese Premier Wen Jiabao owned 135 million shares of Ping An Insurance through a series of investment companies. |81| A March 2016 Times article described Ping An as a "labyrinthine shareholding structure made up of 37 interlocking holding companies." |82|

- Zhejiang Geely Holding Group (one of China's top 10 auto manufactures), while not state-owned, has received government subsidies. For example, The Wall Street Journal reported that Geely received $98 million in 2013 from central and local government entities, equal to 30% of its profits. |83|

China's Plan to Modernize the Economy and Promote Indigenous Innovation

Many of the industrial policies China has implemented or formulated since 2006 appear to stem largely from a comprehensive document issued by China's State Council (the highest executive organ of state power) in 2006 titled the National Medium-and Long-Term Program for Science and Technology Development (2006-2020), often referred to as the MLP. |84| The MLP appears to represent an ambitious plan to modernize the structure of China's economy by transforming it from a global center of low-tech manufacturing to a major center of innovation (by the year 2020) and a global innovation leader by 2050. |85| It also seeks to sharply reduce the country's dependence on foreign technology. The MLP includes the stated goals of "indigenous innovation, leapfrogging in priority fields, enabling development, and leading the future." |86| Some of the broad goals of the MLP state that by 2020:

- The progress of science and technology will contribute 60% or above to China's development.

- The country's reliance on foreign technology will decline to 30% or below (from an estimated current level of 50%).

- Gross expenditures for research and development (R&D) would rise to 2.5% of gross domestic product (from 1.3% in 2005). Priority areas for increased R&D include space programs, aerospace development and manufacturing, renewable energy, computer science, and life sciences. |87|

The document states that "China must place the strengthening of indigenous innovative capability at the core of economic restructuring, growth model change, and national competitiveness enhancement. Building an innovation-oriented country is therefore a major strategic choice for China's future development." This goal, according to the document, is to be achieved by formulating and implementing regulations in the country's government procurement law to "encourage and protect indigenous innovation," establishing a coordination mechanism for government procurement of indigenous innovative products, requiring a first-buy policy for major domestically made high-tech equipment and products that possess proprietary intellectual property rights, providing policy support to enterprises in procuring domestic high-tech equipment, and developing "relevant technology standards" through government procurement.

Reaction by U.S. Stakeholders

Beginning in 2009, several U.S. companies began to raise concerns over a number of Chinese government circulars that would establish an "Indigenous Innovation Product Accreditation" system. For example, in November 2009, the Chinese government released a "Circular on Launching the 2009 National Indigenous Innovation Product Accreditation Work," requiring companies to file applications by December 2009 for their products to be considered for accreditation as "indigenous innovation products." Similar proposed circulars were issued at the provincial and local government levels. U.S. business representatives expressed deep concern over the circulars, arguing that they were protectionist in nature because they extended preferential treatment for Chinese government procurement to domestic Chinese firms that developed and owned intellectual property (IP) and thus largely excluded foreign firms. |88| AmCham China described China's attempt to link IP ownership with market access as "unprecedented worldwide." |89| A letter written by the U.S. Chamber of Commerce and 33 business associations to the Chinese government on December 10, 2009, stated that the indigenous innovations circulars would "make it virtually impossible for any non-Chinese companies to participate in China's government procurement market--even those that have made substantial and long-term investments in China, employ Chinese citizens, and pay taxes to the Chinese government." Such groups contend that a large share of their technology is developed globally and thus it would be difficult to attribute the share of technology developed in China needed to obtain accreditation. |90|

A 2011 AmCham China survey found that 40% of respondents believed that China's indigenous innovation policies would hurt their businesses and 26% said their businesses were already being hurt by such policies. At a November 2011 WTO review of China's IPR policies, the U.S. WTO representative stated that China's policies of adopting indigenous innovation had "created a troubling trend toward increased discriminatory policies which were aimed at coercing technology transfer." He stated that "Chinese regulations, rules and other regulatory measures frequently called for technology transfer, and in certain cases, conditioned, or proposed to condition, the eligibility for government benefits or preferences on intellectual property being owned or developed in China, or being licensed, in some cases exclusively, to a Chinese party." |91|

China's Response to U.S. Concerns

The Chinese government responded to U.S. concerns over its indigenous innovation policies by arguing that they did not discriminate against foreign firms or violate global trade rules. |92| However, during the visit of (then) Chinese President Hu Jintao to the United States in January 2011, the Chinese government stated that it would not link its innovation policies to the provision of government procurement preferences. |93| During the May 2011 session of the U.S.-China Strategic and Economic Dialogue (S&ED), China pledged that it would eliminate all of its indigenous innovation products catalogs. |94| During the November 2011 talks held under the U.S.China Joint Commission on Commerce and Trade (JCCT), the Chinese government announced that the State Council had issued a measure requiring governments of provinces, municipalities, and autonomous regions to eliminate by December 1, 2011, any catalogues or other measures linking innovation policies to government procurement preferences. |95| This occurred after foreign business groups raised concerns that discriminatory indigenous innovation policies might continue to be implemented at the local level even after Hu Jintao's commitment. For example, the USCBC reported in February 2011 that it had identified 22 municipal and provincial governments that had issued at least 61 indigenous innovation catalogues. U.S. business representatives sought to ensure that Beijing's pledge on indigenous innovation would apply at all levels of government in China.

In May 2013, the USCBC reported that, although the central government had largely been successful in ensuring that sub-national governments complied with Hu Jintao's January 2011 commitments, 13 provinces had not yet issued any measures to comply. |96| In addition, an October 2012 USCBC survey found that 85% of respondents said they had seen little impact on their businesses resulting from China's commitments delinking indigenous innovation with government procurement. |97|

Remaining U.S. Concerns

While many U.S. business leaders have applauded China's pledge to delink indigenous innovation from government procurement, some remain wary that China will implement new policies that attempt to provide preferences to local Chinese firms over foreign firms. According to Adam Segal with the Council on Foreign Relations: "Even if China reverses certain policies under U.S. pressure, it will remain dedicated to those goals. U.S. policy is likely to become a game of Whac-a-Mole, beating down one Chinese initiative on indigenous innovation only to see another pop up." |98| U.S. business groups are also concerned with how the MLP blueprint will affect China's commitment to enforcing foreign IPR. They note, for example, that the MLP states: "Indigenous innovation refers to enhancing original innovation, integrated innovation, and re-innovation based on assimilation and absorption of imported technology, in order to improve our national innovation capability." To some, this seems to indicate that China intends to take existing technology, make some changes and improvements on it, and then claim it as its own without acknowledging or compensating the original IPR holders. A 2011 report by the U.S. Chamber of Commerce stated that China's indigenous innovation policies led many international technology companies to conclude that the MLP is a "blueprint for technology theft on a scale the world has never seen before." |99|

U.S. officials have attempted to convince Beijing that, while its desire to increase innovation in China is a commendable goal, its efforts to limit the participation of foreign firms in such efforts, or attempting to condition market access in China to the development of IPR by foreign firms in China will hinder, not promote, the advancement of innovation in China. The direction China takes on this issue could have a significant impact on U.S. economic interests as noted by a study by the USITC:

To the extent that China's policies succeed in accelerating technological progress, productivity, and innovation in the Chinese economy, they could provide spillover benefits for other countries. But if indigenous innovation policies act as a form of technological import substitution, systematically favoring Chinese domestic firms over foreign firms in relevant industries, they would be expected to have a negative effect on foreign firms and economies roughly analogous to what would occur if China simply imposed a protective tariff on imports of goods in the relevant sectors or levied a discriminatory excise tax on the sales of FIEs in the Chinese market. |100|

New Restrictions on Information and Communications Technology