| Information |  | |

Derechos | Equipo Nizkor

| ||

| Information | | |

Derechos | Equipo Nizkor

| ||

Dec13

World Ultra Wealth Report 2012/2013

CONTENTS

World Ultra Wealth Report Outlook 2012 - 2013

NORTH AMERICA

Still LeadingASIA

Slowing GrowthEUROPE

In A StallLATIN AMERICA

Plentiful OpportunitiesMIDDLE EAST AND AFRICA

Wealth Amongst VolatilityOCEANIA

Two Economies

World Ultra Wealth Report Outlook

Global recovery continues to display signs of weakness. Heightened Eurozone financial market and sovereign distress, stuttering recovery in the U.S. and softer than expected growth in major emerging market economies are the main drivers behind the IMF's recent adjustment of its forecast for global growth downwards to 3.5% for 2012 and 3.9% for 2013. The two main assumptions that the forecast is founded upon are policy action in the Eurozone that allows financial conditions to ease gradually and recent monetary policy changes in emerging market economies gaining traction.

The continual recurrence of financial market distress leading to sovereign distress and bailout packages that provide temporary relief in the Eurozone heightens the potential for uncontrolled default and Euro exits. Both these scenarios will have a severe impact on global economic growth prospects and wealth growth.

The following is an analysis of global developments and trends in wealth and ultra wealthy populations for 2012 to 2013 based on Wealth-X's proprietary research.

Major Wealth Indicators GDP* Currency Equity UNHW Population Combined Wealth North America ▲ UP N/A ▲ UP ▲ UP ▲ UP Asia ▲ UP ▼ DOWN ▼ DOWN ▼ DOWN ▼ DOWN Europe ▼ DOWN ▼ DOWN ▼ DOWN ▼ DOWN ▼ DOWN Latin America ▼ DOWN ▼ DOWN ▲ UP ▲ UP ▼ DOWN Middle East ▼ DOWN ▼ DOWN ▼ DOWN ▲ UP ▼ DOWN Africa ▲ UP ▼ DOWN ▲ UP ▲ UP ▼ DOWN Oceania ▲ UP ▼ DOWN ▲ UP ▲ UP ▲ UP WORLD ▼ DOWN ▼ DOWN ▼ DOWN ▲ UP ▼ DOWN Note: *All GDP growth rates are measured relative to the previous year's growth rate.

WEALTH TRENDS

Investment

UHNW investors are shifting their wealth into private companies, real estate and commodities.

Risk aversion is largely reflected in the shift away from speculative financial investments to hard assets.

Professionals and institutions engaging with UHNWIs should consider strategies and approaches that address the current concerns and focus of these clients.

Reduction in Tax Exposure

As governments around the world look to revive state finances through higher and stricter taxation regimes, UHNWIs look to reduce their tax exposure through a shift to territories with beneficial tax regimes. Professionals engaging with the ultra wealthy need to consider strategies that reduce tax exposure and address their clients' concerns.

WEALTH CURRENTS

2012 at present has been a year of shifting wealth currents, with the broad direction for wealth flows going eastwards. Eurozone UHNWIs, concerned over volatility and distress in sovereign and financial markets, have shifted wealth away from the periphery towards core economies with Germany and Switzerland as favoured destinations on the Continent. Other beneficiaries include the United Kingdom, the US, Hong Kong and Singapore.

The shift in wealth growth to emerging economies poses a challenge for wealth management firms based in the U.S. and Europe, who need to convince clients of their long term viability. In contrast, finding and keeping talent in developing markets is a key success factor as wealth management firms need to invest in human capital to capitalise on the opportunities presented by the shift.

STATE OF WORLD'S UHNW POPULATION

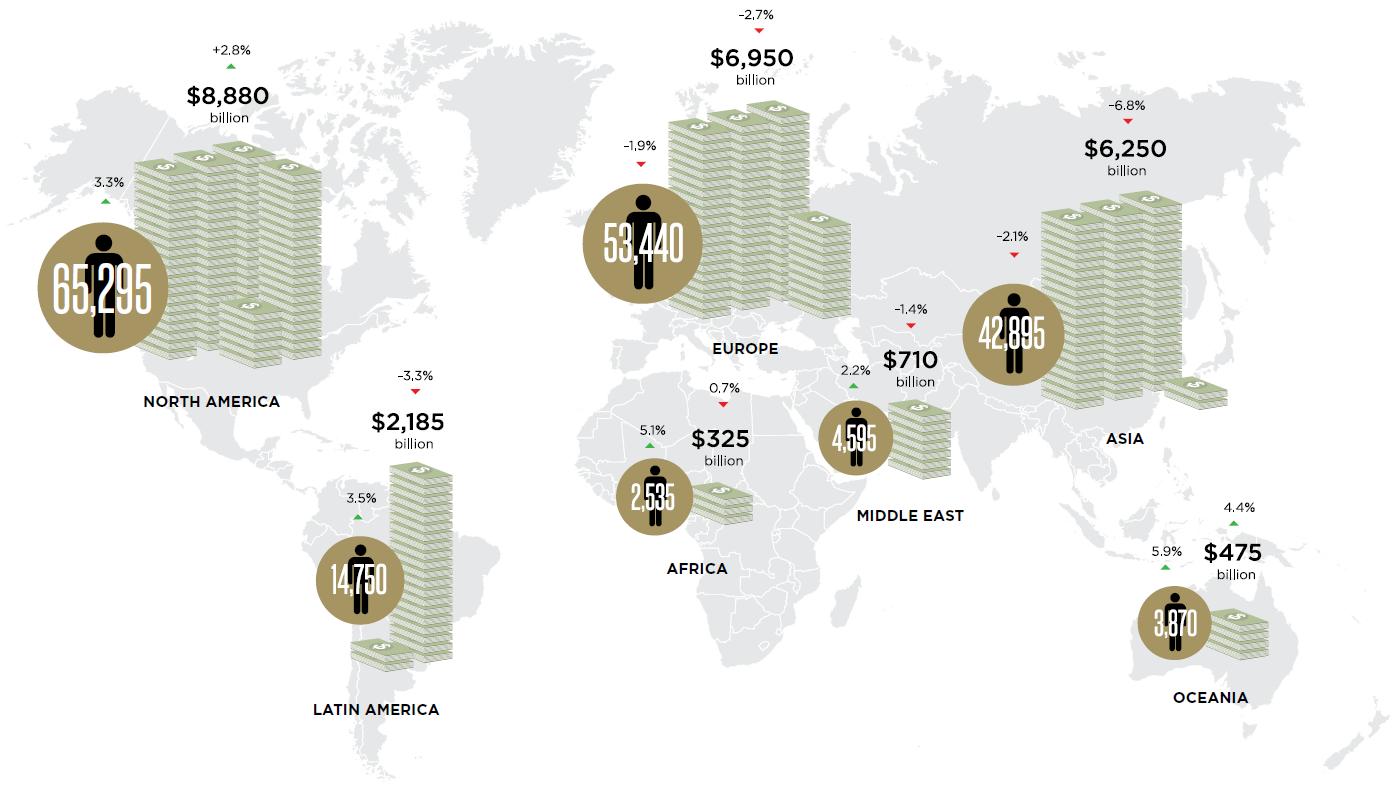

- The global UHNW population stands at 187,380 with a combined wealth of US$25.8 trillion. Combined wealth attributable to this segment shrank by 1.8% from a year ago. The decrease was largely driven by the Eurozone crisis and a slowdown in emerging economies.

- Oceania saw the greatest growth in UHNW population, with an increase of 5.9%, largely driven by the continued growth of Australia.

- Asia, in contrast, saw the largest percentage reduction in UHNW population amongst the regions. The 2.1% reduction in UHNW population is a result of poor equity performance, particularly in Japan, China and India.

- Combined wealth loss was highest in Asia as Hong Kong, China and Japan led wealth loss across the region.

- The U.S. leads in terms of real growth in UHNW population numbers, with 2,250 UHNWIs joining the ranks of the ultra wealthy. The combined total wealth of the U.S. UHNW population expanded by US$ 265 billion.

This Year's UHNW Population This Year's Wealth

US $ BillionLast Year's UHNW Population Last Year's Wealth US $ Billion Population Change % Total Wealth Change %

Click to enlargeGlobal Total 187,380 25,775 186,345 26,255 0.6% -1.8%

World UHNWI This Year's This Year's Last Year's Last Year's Net Worth UHNW Population Total Wealth

US$ billionUHNW

PopulationTotal Wealth

US$ billionPopulation

Change %Total Wealth

Change %$1 billion + 2,160 6,190 1,975 5,430 9.4% 14% $750 million to $999 million 990 855 1,090 845 -9.2% 1.2% $500 million to $749 million 2,475 1,560 2,415 1,440 2.5% 8.3% $250 million to $499 million 8,090 3,225 9,275 3,620 -12.8% -10.9% $200 million to $249 million 13,500 3,035 14,690 3,450 -8.1% -12% $100 million to $199 million 22,290 3,335 24,125 3,735 -7.6% -10.7% $50 million to $99 million 56,205 4,295 51,435 4,475 9.3% -4% $30 million to $49 million 81,670 3,280 81,340 3,260 0.4% 0.6% TOTAL 187,380 25,775 186,345 26,255 World Population Change % 0.6% World Wealth Change % -1.8% Wealth-X analysis shows the world's UHNW population grew by 0.6%. The growth rate of the global billionaire population outstripped that growth rate by expanding at 9.4%.

There are 2,160 billionaires globally. This group of billionaires, representing the top 1.2% of the world's UHNW population, control 24% of the total fortune attributable to the ultra wealthy. On average, these billionaires are worth US$2.9 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 43.6% of the total global UHNW population. They have a combined fortune of close to US$3.3 trillion or 12.7% of the total wealth of the world ultra affluent population.

THE WEALTH-X FIVE YEAR FORECAST

In the next five years, Wealth-X forecasts that the world's UHNW population will grow by an annual average of 3.9% and the wealth attributable to the UHNW population is expected to grow by 5.5%.

Region Average Annual Population Change % Average Annual Wealth Change % North America 2.4% 3.4% Asia 5.4% 7.9% Europe 2.9% 3.5% Latin America 6.5% 12.1% Middle East 4.5% 7.4% Africa 6.9% 11.2% Oceania 2.9% 5.5% WORLD PROJECTIONS Global Average Annual

Population Growth %3.9% Global UHNW Wealth

Average Annual Growth %5.5% Of all the regions, Africa's UHNW population is expected to grow at the fastest rate, expanding by an average of 6.9% each year. The North American UHNW population, in contrast, is expected to grow at the slowest pace, expanding at 2.4%. The combined wealth attributable to the Latin American UHNW population is expected to grow by 12.1%, a rate that surpasses that of Africa. In terms of wealth growth, North America lags the other regions, seeing wealth growth at an average rate of 3.4%.

Based on the forecast growth projections, the Asian UHNW population will surpass the same measure for the U.S. by 2025, ahead of the 2032 prediction made in the 2011 - 2012 World Ultra Wealth Report. Total Asian UHNW wealth is forecast to surpass the U.S. combined wealth by 2020.

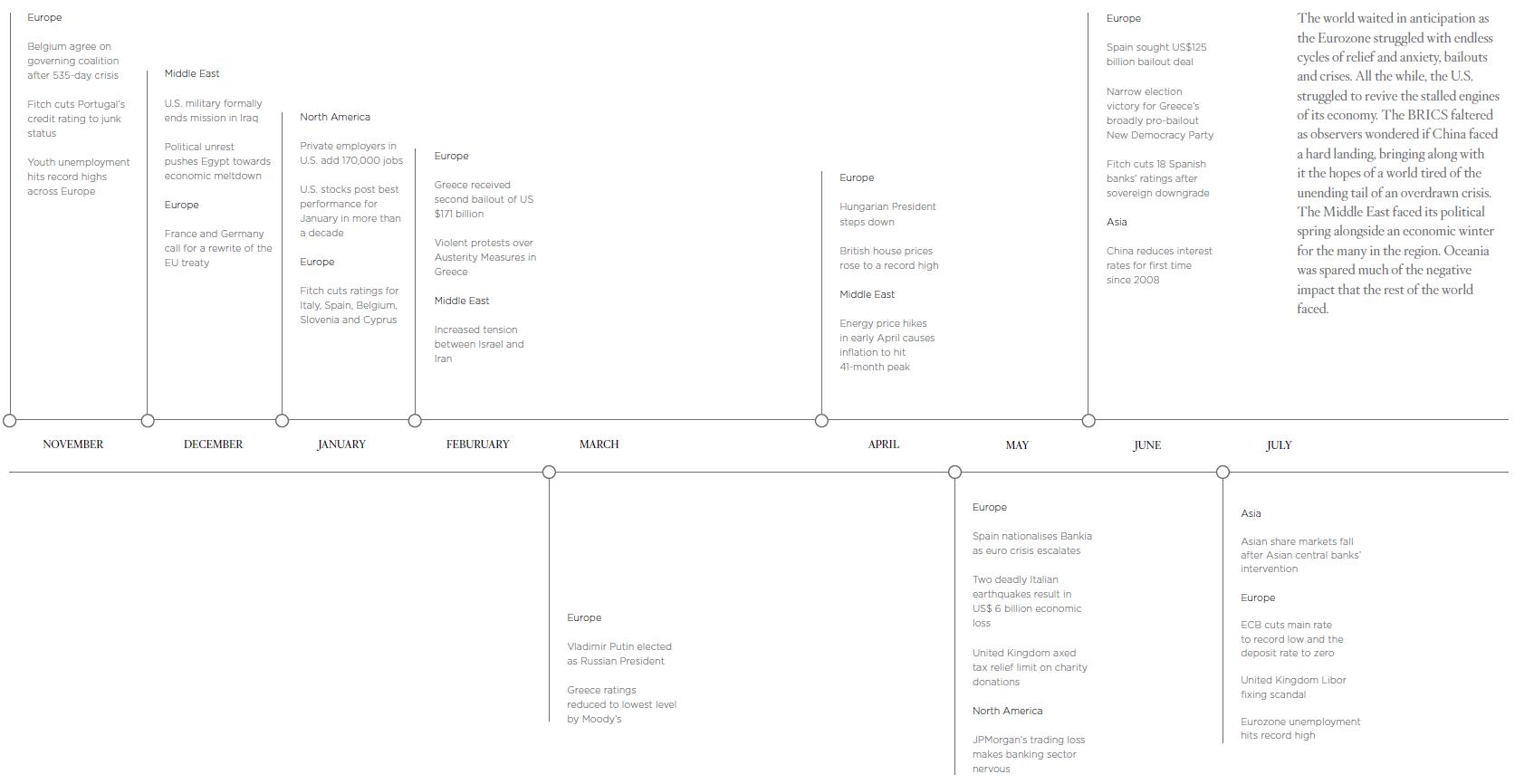

KEY WORLD EVENTS IN 2011 - 2012

Click to enlarge

Growth in the North American region is expected to be stable but modest. The International Monetary Fund (IMF) predicts the U.S. economy will expand by 2% in 2012, compared to the 1.7 % Gross Domestic Product (GDP) growth in 2011. Canada is expected to see moderate growth, going from 2.5% in 2011 to 2.1% this year.

Even as growth momentum in the world's biggest economy slowly recovers, downside risks remain. There is much debate as to whether the recovery in the U.S. will accelerate. The Federal Reserve has maintained interest rates near zero since 2008 and plans to maintain those rates through 2014 to revive the economy. To date, the U.S. Federal Reserve has carried out two rounds of quantitative easing. While the short term policy measures introduced after the financial crisis in 2008 have been sufficient, questions remain as to a sustainable fiscal plan for the longer term.

While the equity markets are positive, the S&P 500 index was up 7.2% during our measurement period, the housing market is stabilizing and consumer spending and confidence remain cautious. Corporate profits strengthened during the year, in part due to cost cutting measures. With the 2012 Presidential election in the balance and uncertain economic conditions in the Eurozone, there are fears of possible spillover effects on the American economy, which may in turn cause a drag on Canada's economy. The overall outlook for North America is cautious as potential threats lie ahead on the road to full recovery.

Hotspot

U.S.

- America's ultra affluent segment is growing at a rate that is faster than projected GDP for the country, boosted in part by the performance of equity markets. The wealth of the nation's richest expanded at a pace that outstripped the increase in UHNW population. This underlines the fact that the ultra wealthy generally recover faster during periods of recovery and expansion.

- With the U.S. authorities ramping up the fight against offshore tax havens, American UHNWIs are having to identify new avenues to protect their wealth and reduce tax exposure. The ultra wealthy are expected to continue to seek markets with less transparency and no tax treaties with the U.S.

- Despite the weakness in global markets and the tepid recovery within the U.S., the American UHNW market is one that captures attention. The number of billionaires in the country grew by 5.5% against a backdrop of resentment against the rich and those perceived to have exploited loopholes in the banking system, resulting in major protests and movements that spread round the world. America's billionaires, or the top 0.8% in the ultra affluent space, control 24.8% of the total wealth attributable to the UHNW segment.

This Year's This Year's Last Year's Last Year's U.S. UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billion$1 billion + 480 2,055 455 1,910 $750 million to $999 million 230 215 220 205 $500 million to $749 million 935 690 850 620 $250 million to $499 million 1,370 665 1,590 760 $200 million to $249 million 3,045 740 2,910 715 $100 million to $199 million 4,435 790 4,160 795 $50 million to $99 million 19,070 1,750 18,330 1,650 $30 million to $49 million 30,715 1,380 29,515 1,365 TOTAL UHNW 60,280 8,285 58,030 8,020 Our analysis shows there are 480 billionaires in the country. This group of billionaires, control almost a fifth of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth US$4.3 billion each. Wealth-X estimates that the UHNW population in the US expanded by 3.9% and total wealth of the ultra affluent grew by 3.3 %.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 51% of the total UHNW population in the U.S. They have a combined fortune of US$1.4 trillion or 16.7% of the total wealth of the American ultra affluent segment.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For America ▲ UP N/A ▲ UP ▲ UP ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

State This Year's Number

of UHNW ResidentsLast Year's Number

of UHNW ResidentsPopulation Growth % 1 California 10,955 10,335 6% 2 New York 8,595 8,175 5.1% 3 Texas 5,890 5,520 6.7% 4 Florida 3,650 3,600 1.4% 5 Illinois 2,780 2,670 4.1% 6 Michigan 1,700 1,590 6.9% 7 Pennsylvania 1,620 1,590 1.9% 8 Connecticut 1,345 1,280 5.1% 9 Ohio 1,330 1,305 1.9% 10 Wisconsin 1,295 1,280 1.2% 11 New Jersey 1,275 1,255 1.6% 12 Virginia 1,200 1,175 2.1% 13 Washington 1,195 1,160 3% 14 Minnesota 1,125 1,105 1.8% 15 Georgia 1,110 1,085 2.3% 16 Maryland 1,060 1,035 2.4% 17 Massachusetts 995 940 5.9% 18 North Carolina 945 905 4.4% 19 Colorado 925 885 4.5% 20 Arizona 910 880 3.4% 21 Indiana 830 815 1.8% 22 Tennessee 815 790 3.2% 23 Oklahoma 800 785 1.9% 24 Missouri 760 750 1.3% 25 Arkansas 560 560 0% 26 Kansas 560 550 1.8% 27 Nevada 495 500 -1% 28 District of Columbia 475 440 8% 29 Alabama 380 395 -3.8% 30 Oregon 380 350 8.6% 31 Kentucky 375 375 0% 32 Louisiana 375 385 -2.6% 33 Montana 340 340 0% 34 Nebraska 300 305 -1.6% 35 South Carolina 295 295 0% 36 Wyoming 295 300 -1.7% 37 Mississippi 265 280 -5.4% 38 Rhode Island 260 255 2% 39 West Virginia 205 210 -2.4% 40 Hawaii 200 195 2.6% 41 Iowa 200 195 2.6% 42 Idaho 190 190 0% 43 Utah 190 180 5.6% 44 New Hampshire 180 175 2.9% 45 South Dakota 145 145 0% 46 Vermont 135 135 0% 47 New Mexico 130 130 0% 48 Maine 85 85 0% 49 Delaware 55 55 0% 50 North Dakota 55 50 10% 51 Alaska 50 45 11.1% TOTAL 60,280 58,030 3.9%

- California continues to be home to the largest population of UHNW individuals in the U.S., with 18.2% of the total UHNW population in the country. This comes as no surprise as wealth-generating clusters, such as Silicon Valley, power the state. Compared to the same period last year, the state added close to 6% more ultra affluent residents, thanks to a recovering equity market which benefited the U.S.'s largest home base of over 3,500 publicly traded companies. 2012 has seen many liquidity events involving social media, with Facebook grabbing headlines with its Nasdaq listing and propelling a number of its shareholders firmly into the UHNW segment.

- New York follows with 8,595 ultra wealthy dwellers. The state saw a 5.1% increase in UHNW residents compared to last year.

- The collective population of the top ten UHNW states accounted for 65% of the total U.S. UHNW population, slightly higher than the previous year. Within the top ten states, Connecticut overtook Ohio as the eighth largest state in part due to a rebounding New York City, which benefited the Tri-State area.

- The states that saw the largest percentage growth in UHNWI population were: Alaska at 11.1% and Oregon at 8.6%. Improvement in the unemployment rate in Oregon has seen it take the lead in UHNW population growth. Mississippi led all states with a decline in growth of -5.4%; Alabama at -3.8%; and Louisana at -2.6%. With high concentration in manufacturing, these Southern states have borne the brunt of the economic slowdown.

Top 10 U.S. City Ranking This Year's Population 1 New York 7,535 2 San Francisco 4,580 3 Los Angeles 4,525 4 Chicago 2,610 5 Washington 2,395 6 Houston 2,285 7 Dallas 2,015 8 Atlanta 970 9 Seattle 950 10 Boston 915 10 Philadelphia 915

- The NYC Metro area once again tops the UHNW U.S. City Rankings with 7,535 individuals worth at least $30 million. San Francisco overtook Los Angeles as home to the second largest population of UHNW individuals due to local firms who benefited from buoyant equity and venture capital markets. Chicago, Washington, Houston, Dallas and Atlanta all retained their places on the list.

- Seattle, with stronger corporate profits and job growth, overtook Boston in terms of the UHNW population.

- Philadelphia made its debut on the list, sharing tenth spot with Boston.

Asia emerged relatively unscathed from the financial contagion sparked by the 2008 credit crisis that has continued to affect the other parts of the world. Although Asia has been spared the fallout from the credit and sovereign debt crisis in the Eurozone, the crisis has dampened the pace of growth Asia has been accustomed to in recent years.

Asia, as a region, has seen GDP growth dip from 8.3% in 2010 to 5.9% in 2011, according to the IMF. With GDP growth rate expected to stabilise at 6% for 2012 and set to rise to 6.5% in 2013, Asia looks to be a rare spot of stability in a world where uncertainty and volatility is the new norm.

The majority of downside risks to Asia are external. The most apparent risk is that of the adverse impact on Asian exports from reduction in demand from western economies. This is particularly evident in export-oriented economies, including Thailand, China and India, where a reduction in demand from crisis-hit economies in the West has impacted growth. Other risks include those from volatile capital flows and those faced by importers and exporters due to the volatility of commodity prices. Asia has the flexibility and policy tools to manage these risks due to prudent macroeconomic policies pursued in the aftermath of the 1997 Asian financial crisis.

The need to support domestic demand in the region is crucial. Despite the adoption of tightening measures, loose monetary policy is expected to prevail, particularly in China and India. Fiscal policy remains supportive of growth in most countries, through an emphasis on social spending and infrastructure. However, credit growth, which has helped sustain domestic demand, has begun to decelerate across the region. The slowdown reflects a number of factors, including weak credit demand and tightening of credit policies within the banking system.

The impact of rising oil prices, particularly in the event of supply disruptions from tensions in the Middle East, could result in lower growth in energy dependent economies as well as higher inflation rates. Combined with the possibility of sluggish domestic demand, growth across Asia could disappoint. However, most observers agree that the Asian growth story largely continues unabated, anchored by China, with particular emphasis on the need to rebalance and promote domestic demand driven growth.

This Year's This Year's Last Year's Last Year's ASIA UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total Wealth

Change %Japan 12,830 2,075 13,040 2,270 -1.6% -8.6% China 11,245 1,580 11,510 1,695 -2.3% -6.8% India 7,730 925 8,215 980 -5.9% -5.7% Hong Kong 3,135 470 3,200 530 -2% -11.3% South Korea 1,385 265 1,400 290 -1.1% -8.6% Singapore 1,305 155 1,355 170 -3.7% -8.8% Taiwan 1,185 200 1,155 205 2.6% -2.4% Indonesia 785 120 750 85 4.7% 41.2% Malaysia 780 100 725 100 7.6% 0% Thailand 625 95 600 95 4.2% 0% Philippines 580 85 550 100 5.5% -15% Pakistan 310 40 285 40 8.8% 0% Vietnam 170 19 170 19 0% 0% Kazakhstan 140 20 155 25 -9.7% -20% Bangladesh 85 13 105 16 -19% -18.8% Uzbekistan 80 12 75 11 6.7% 9.1% Srilanka 60 9 75 11 -20% -18.2% Azerbaijan 60 9 60 9 0.0% 0% Mongolia 40 6 35 5 14.3% 20% Tajikistan 40 6 40 6 0% 0% Rest Of Central Asia 95 14 85 14 11.8% 0% Rest Of Asia Pacific 230 35 225 35 2.2% 0% Total 42,895 6,253 43,810 6,711 Asia Population Change % -2.1% Asia Wealth Change % -6.8% Wealth-X analysis has identified Asia as home to 42,895 UHNW individuals with a combined net worth close to US$ 6.3 trillion. There are 915 individuals who have left the ranks of the ultra wealthy since the release of the 2011 World Ultra Wealth Report. Asia saw a loss of 2.1% of its ultra wealthy population.

Wealth-X analysis shows Sri Lanka saw the largest percentage reduction in UHNW population, followed by Bangladesh and Kazahstan. In absolute terms, India suffered the largest reduction in UHNW population, losing 485 ultra wealthy individuals, followed by China who lost 265 UHNWIs and Japan who lost 210. In contrast, Mongolia's UHNW population increased by 14.3%, followed by the rest of Central Asia and Pakistan. Total wealth for the region declined by US$458 billion or close to 6.8%.

Significant Drivers:

- Declines in total wealth and population figures are largely driven by declines in three major countries, namely Japan, China and India, who collectively constitute close to 75% of the UHNWI population for the region. However, we are confident that these trends will reverse in the future based on the strength of financial systems and economies in the region.

- JAPAN: Japan's GDP saw modest growth, however, its equity market declined by 16% during the measuring period. Japan's property market also saw a slight decline while the Yen appreciated by 3.3%, due to the continuing effects of the 2011 earthquake and tsunami.

- CHINA: China's GDP estimates have been weaker than earlier forecasts. The Shanghai Stock Exchange Composite Index declined by 20% during the measuring period. The Chinese property market was stable with a downward bias while the Yuan appreciated 2% after central bank intervention slowed the pace of appreciation.

- INDIA: India's GDP continued to moderate. The Indian equity markets, which have significant impact on the local UHNW population, declined by 8% during the measuring period while the Indian Rupee declined by 25%.

NORTH ASIA

The leading engine of growth, North Asia has consistently seen higher GDP growth than other sub-regions of the Asian Continent. The ongoing financial crisis in the Eurozone has brought about deteriorating external demand and volatile financial markets in North Asia. GDP growth for the sub-region saw a dip to 8% for 2011 and is set to further decline to an estimated 7.1% for 2012, according to the Asian Development Bank. Leading indicators point towards continual moderation, particularly in industrial production, retail sales and exports.

Growth is expected to stabilise in 2013 at a forecast rate of 7.5%. Any visible economic slowdown in China would reverberate across global supply chains, creating a domino effect for commodity and resource rich economies. The spilling over of geopolitical tensions into the economic arena continues to be the single most disruptive factor in the sub-region.

UHNW population and wealth growth is dependant on leading economies in the sub-region avoiding further spillover from the Eurozone crisis.

This Year's This Year's Last Year's Last Year's North Asia UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %1 Japan 12,830 2,075 13,040 2,270 -1.6% -8.6% 2 China 11,245 1,580 11,510 1,695 -2.3% -6.8% 3 Hong Kong 3,135 470 3,200 530 -2% -11.3% 4 South Korea 1,385 265 1,400 290 -1.1% -8.6% 5 Taiwan 1,185 200 1,155 205 2.6% -2.4% TOTAL 29,780 4,590 30,305 4,990 -1.7% -8.0% The slowing of growth across North Asia has had a direct impact on UHNW populations across the sub-region with a majority of the countries registering a drop in UHNWIs and combined wealth.

SOUTH ASIA

South Asia counts some of the poorest countries in Asia amongst its members with many currently in nascent stages of economic development. Despite the dip in growth to 6.4% in 2011%, South Asia saw Foreign Direct Investment (FDI) grow by 23% in 2011. With the weak global environment leading to a reduction in exports and investment inflows, South Asia is set to see growth further moderate to 6.2% in 2012, according to the Asian Development Bank.

Widening trade deficits have led to the depreciation of most currencies in the sub-region and increased inflation levels, though stable inward remittances have helped offset some of the negative effects. Manufacturing growth has largely slowed and FDI has declined particularly in India and Pakistan. The poor performance of the Indian equity markets has had a negative impact on the Indian UHNWI population. Political unrest and instability across the sub-region continues to exert negative influence and act as deterrents for investors.

This Year's This Year's Last Year's Last Year's South Asia UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %1 India 7,730 925 8,215 980 -5.9% -5.7% 2 Pakistan 310 40 285 40 8.8% 0% 3 Bangladesh 85 13 105 16 -19.0% -18.8% 4 Sri Lanka 60 9 75 11 -20% -18,2% TOTAL 8,185 985 8,680 1,045 -5.7% -5.7% The South Asian sub-region recorded the steepest decline in UHNW populations and the second largest decline in combined wealth figures in Asia as a result of equity market valuation decreases.

SOUTH EAST ASIA

South East Asia has displayed financial resilience amidst the ongoing global crisis, that is a legacy of the 1997 Asian financial crisis. The sub-region's economies expanded 4.3% in Q1 2012, according to the Asian Development Bank. Growth largely came from the strong rebound in Thailand after the flood-related disruptions of 2011 and robust growth in the Philippines. Large-scale investments in infrastructure and burgeoning private consumption, driven by a growing middle class and social reforms, are key drivers of growth in the sub-region.

Strong domestic demand has helped offset weaker export figures as consumer confidence increased across the region, particularly in Thailand and Indonesia. Luxury consumption across the sub-region has remained stable despite the global uncertainty and natural disasters, a reflection of the strength of the economies that form the regional subset. South East Asian equity markets continue to see IPO activity, despite a slowdown in equity markets elsewhere, with Indonesia as a star performer.

While Singapore has emerged as a global wealth management hub, it is Indonesia that has topped the sub-region as the powerhouse of UHNW wealth and population growth.

This Year's This Year's Last Year's Last Year's South East Asia UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %1 Singapore 1,305 155 1,355 170 -3.7% -8.8% 2 Indonesia 785 120 750 85 4.7% 41.2% 3 Malaysia 780 100 725 100 7.6% 0% 4 Thailand 625 95 600 95 4.2% 0% 5 Philippines 580 85 550 100 5.5% -15% 6 Vietnam 170 19 170 19 0% 0% TOTAL 4,245 574 4,150 569 2.3% 0.9% With the exception of Singapore, the sub-region saw healthy growth in UHNW populations and combined wealth for some with Indonesia in the lead.

CENTRAL ASIA

Central Asia continued to deliver steady GDP growth. Despite a dip in GDP growth in 2011, Central Asia looks set to stabilise at a respectable 6.1% for 2012. As commodity exports boomed and overseas remittances grew, Central Asia saw steady economic performance in the last two years. In particular, the discovery of some of the world's largest unexploited mineral deposits in Mongolia led to an unprecedented boom in FDI into the region.

Strong public spending growth, development of a new oil field in Kazakhstan and a new gas pipeline network in Turkmenistan are expected to support growth in the sub-region. With commodity and fuel prices expected to stabilise, the outlook for Central Asia remains optimistic. The main downside risk comes in the form of political instability, which could destabilise the sub-region and act as a deterrent for investors.

UHNW population and wealth growth is very much dependent on the maintenance of stability in the sub-region and continued resource demand from external countries.

This Year's This Year's Last Year's Last Year's Central Asia UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %1 Kazakhstan 140 20 155 25 -9.7% -20% 2 Uzbekistan 80 12 75 11 6.7% 9.1% 3 Azerbaijan 60 9 60 9 0% 0% 4 Mongolia 40 6 35 5 14.3% 20% 5 Tajikistan 40 6 40 6 0% 0% Rest Of Central Asia 95 14 85 14 11.8% 0% TOTAL 455 65 450 70 1.1% -4.3% The star performer in the sub-region is Mongolia, which registered unprecedented growth in UHNW population and combined wealth.

Hotspot

INDIA

- Asia's third-largest economy saw growth decelerate to 6.9% in 2011 and is expected to grow at 6.6% in 2012, according to the World Bank.

- India's growth has slowed down due to global uncertainty, tightening measures adopted by the central bank in the form of higher interest rates as well as a deceleration in investment. The last is linked to structural impediments to investment, such as, problems with power supply, land acquisition and securing government approvals. The resolution of these impediments to private investment is critical to India's growth.

- A general lack of comprehensive infrastructural development and the prevalence of corruption are direct challenges for foreign investors and local business. The need to deal with infrastructure bottlenecks and ensure smoother public service delivery cannot be overstated. According to the IMF, India will accrue a demographic dividend in the next few decades and its ability to capitalize on it will depend on the development of its infrastructure.

- Recent tax-related policies announced by the government as part of its budget has caused unease among foreign and local firms. Prime Minister Manmohan Singh's assurance in early July that the government will not implement arbitrary taxation policies has sent a message of reassurance to the global investment community that "India is a safe and attractive investment destination".

- A combination of regulatory and political risks as well as hefty fiscal and current account deficits led to downgrades in India's credit rating outlook from both Fitch and Standard & Poor's earlier in the year.

- Choosing to see rising inflation as the greater of two evils, the Reserve Bank of India allowed interest rates to rise till October 2011, despite the resultant high cost of capital causing concerned amongst industry players and growing signs of stagnation in the manufacturing sector.

- With slowing growth as well as declining investment and business sentiment, there is speculation that the central bank may need to go beyond easing reserve requirements and directly cut interest rates to infuse liquidity into the economy.

- UHNW population and wealth growth depends on the economy redefining its direction and clarity of government policies.

This Year's This Year's Last Year's Last Year's India UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %$1 billion + 109 190 115 205 -5.2% -7.3% $750 million to $999 million 25 20 25 21 0% -4.8% $500 million to $749 million 125 80 135 90 -7.4% -11.1% $250 million to $499 million 200 75 215 75 -7% 0% $200 million to $249 million 655 160 665 155 -1.5% 3.2% $100 million to $199 million 845 135 895 140 -5.6% -3.6% $50 million to $99 million 2,240 140 2,380 160 -5.9% -12.5% $30 million to $49 million 3,535 125 3,785 135 -6.6% -7.4% TOTAL 7730 925 8,215 980 Population Change % -5.9% Wealth Change % -5.7% Wealth-X analysis shows there are 109 billionaires in the country. This group of billionaires, representing the top 1.4% of the UHNW population, control 20.5% of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth close to US$1.7 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 45.7% of the total UHNW population in India. They have a combined fortune of US$125 billion or 13.5% of the total wealth of the India's ultra affluent.

NON-RESIDENT INDIANS (NRIs)

NRIs This Year's UHNW

NRIs By RegionLast Year's UHNW

NRIs By RegionPopulation Change % North America 1990 1925 3.4% Europe 1050 1080 -2.8% Asia 915 955 -4.2% Middle East 760 750 1.3% Latin America 205 200 2.5% Africa 50 50 0% TOTAL 4970 4960 0.2% The global NRI UHNW population grew by 0.2% during the measuring period, largely driven by increases in the NRI UHNW population in North America. The positive performance of the technology sector in the U.S. has been a major factor behind the growth of the NRI population in the region.

The NRI population in Asia was adversely affected by the poor performance of equity markets and weakness in the financial services sector.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For India ▼ DOWN ▼ DOWN ▼ DOWN ▲ UP ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

Hotspot

CHINA

- As the world's second-largest economy and widely regarded as the most important driver of global growth, China has seen growth slow to 9.2% in 2011 and is expected to see even slower growth in 2012 at a forecast rate of 8.2%, according to the World Bank.

- General consensus among China observers is that the objectives of rebalancing should be achieved through raising the domestic absorptive capacity of China's economy by increasing the relative share of consumption and directing resources into more productive sectors of the economy, rather than a reduction in the net role of exports. The need for China to shift from investment-led to consumption-led growth was officially incorporated as a priority in the 12th Five Year Plan released in 2011.

- Despite widely held views that China's heavily export-oriented economy needs to address imbalances to stave off crisis in the long run, fixed asset investment, particularly infrastructure investment, remains a choice option to prevent any slowdown from turning into a slump in the short run. World Bank data shows gross fixed asset investment rose to over 45% of GDP back in 2010 and has continued to grow. The IMF believes that gross fixed asset investment accounting for 45% of GDP or more may be maintained for the next five years.

- Fixed asset investment as a proportion of GDP continued to rise this year, with fixed asset investment undertaken by State-Owned Enterprises (SOEs) expanding by 25% in June.

- Local government debt, the burden imposed by the financing needs of SOEs and the growing trend of non-performing loans continue to prompt concern among observers that liquidity problems might contribute to the difficulties plaguing the Chinese economy. For the first time since 2005, the volume of non-performing loans held by Chinese banks increased in two consecutive quarters in the first half of 2012.

- The China Banking Regulatory Commission is expected to keep the maximum loan-to-deposit ratio at 75% and could adopt measures that constrain credit growth. In addition, limits were placed on bank lending to local governments to reduce liquidity risk, prevent an increase in bad assets held by banks and decrease the likelihood of default. All in an effort to balance the consequences of lower interest rates and reserve requirements that are the result of stimulative monetary policy.

- Efforts to deflate the housing bubble and discourage speculative activity in the housing market have accompanied the easing of credit market conditions for the rural sector. Taken with measures to boost consumer purchasing power, provide pension insurance for all rural residents and unemployed citizens as well as alleviate income inequality, there is clear focus on the harmony ideal espoused by the government.

- The central bank decision to increase the trading band for the Renminbi is expected to allow market forces to play a greater role in determining the level of the exchange rate. However, the slow appreciation in the effective exchange rate may do little to ease tensions that have arisen over accusations of currency manipulation.

- Weakening global demand, exacerbated by Eurozone instability and a weak U.S. recovery, has led to a notable slowdown in manufacturing activity in China. Trade surplus data for China provided further evidence of the softening of domestic demand and exporters' moves to reduce inventory due to concerns over weak growth in new orders.

- The impact could reverberate along the global supply chain as trade partners that have vertical supply chain links with China, particularly commodity suppliers, who may face a decline in demand for commodities alongside China's exports as the Eurozone crisis plays out.

- In a year of political power transition in China, major economic disruptions and the potential turmoil from the unwinding of imbalances is expected to be avoided. China observers largely agree that maintaining the status quo is the favoured option of the government and bureaucracy.

- UHNW population growth will accelerate should there be a smooth transition to consumption-led growth and the political direction continues to remain clear.

This Year's This Year's Last Year's Last Year's China UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %$1 billion + 147 380 150 540 -2% -29.6% $750 million to $999 million 70 60 75 60 -6.7% 0% $500 million to $749 million 245 145 250 145 -2% 0% $250 million to $499 million 785 265 800 255 -1.9% 3.9% $200 million to $249 million 1,175 250 1,205 225 -2.5% 11.1% $100 million to $199 million 1,470 165 1,505 155 -2.3% 6.5% $50 million to $99 million 2,745 145 2,810 145 -2.3% 0% $30 million to $49 million 4,610 170 4,715 170 -2.2% 0% TOTAL 11,245 1580 11,510 1,695 Population Change % -2.3% Wealth Change % -6.8% Wealth-X analysis shows there are 147 billionaires in the country. This group of billionaires, representing the top 1.3% of the UHNW population, control 24.1% of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth almost US$2.6 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 41% of the total UHNW population in China. They have a combined fortune of US$170 billion or 10.8% of the total wealth of China's ultra affluent.

TOP 10 CHINESE CITIES BY UNWH POPULATION

Chinese Cities UHNW Population By City 1 Beijing 2,295 2 Shanghai 1,435 3 Shenzhen 1,070 4 Guangzhou 970 5 Hangzhou 780 6 Chengdu 435 7 Xiamen 385 8 Changsha 325 9 Ningbo 285 10 Fuzhou 265 First line cities lead the charge when it comes to where UHNW individuals choose as their primary location in China. Beijing, Shanghai and Shenzhen top the table.

Guangzhou, Hangzhou and Chengdu continue to be popular among the newly rich. Cities in the East and South dominate the list.

8,245 UHNWIs or 73% of China's UHNW population are located in the top 10 cities.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For China ▼ DOWN ▲ UP ▼ DOWN ▼ DOWN ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

Hotspot

INDONESIA

- Southeast Asia's largest economy grew at its fastest pace in 20ii, 6.5% according to the World Bank. With growth projected to be 6% for 20i2, Indonesia's outlook is promising.

- Rating agencies, prompted by robust economic growth figures and evidence of fiscal prudence, raised Indonesia's sovereign credit ratings, returning the country to investment grade 14 years after the Asian financial crisis.

- Foreign investors have returned in droves, attracted by the country's abundant natural resources, booming private consumption and a favourable investment climate. However, the wave of protectionist regulations aimed at increasing revenue, encouraging investment and protecting local interests, particularly in relation to the mining sector have raised concerns amongst foreign investors. Contributing almost 11% to Indonesia's GDP, the mining sector has been a focal point for an estimated US$ 19 billion in FDI inflows in 2011.

- The sector is vulnerable to vertical supply chain stresses resulting from weakening demand from large trading partners, such as China. The vulnerability of the mining sector is expected to be partly offset by robust domestic demand.

- An appreciating currency and inflationary pressures have accompanied strong growth prospects and the boom in foreign investment, making attempts to reduce fuel subsidies controversial and unpopular. Total energy subsidies are expected to top US$ 32 billion in 2012. The failure to cut the subsidies is expected to push the country's budget deficit to 2.3% of GDP

- Indonesia's demographics are largely in its favour, with more than half its population under the age of 30 and a large portion of its population poised to enter the middle class. For foreign investors, Indonesia is an important consumer market as robust domestic private consumption shields it from global economic shocks. Indonesia's stock market has been on a positive trajectory with new historic highs reached in early April and saw success in the fixed income arena as well with a highly successful U.S. dollar bond issue placement.

- Pervasive corruption and bureaucratic inefficiencies are constant challenges Indonesia needs to address. Infrastructural inadequacies form another formidable hurdle for the government. While the government has promised increased investment in infrastructure development, investors need to see plans transform into action.

- The large disparity in income levels indicates there is scope for philanthropy to contribute towards the reduction of social inequality.

- UHNW population growth has been supported by the outstanding performance of the economy and looks set to continue to the foreseeable future.

Indonesia UHNWI This Year's This Year's Net Worth UHNWI Total Wealth

US$ billion$1 billion + 25 50 $750 million to $999 million 15 12 $500 million to $749 million 10 6 $250 million to $499 million 35 12 $200 million to $249 million 50 10 $100 million to $199 million 95 10 $50 million to $99 million 175 11 $30 million to $49 million 380 12 TOTAL 785 120 Wealth-X analysis shows there are 25 billionaires in the country. This group of billionaires, representing the top 3.2% of the UHNW population, control 40.7% of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth US$2 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 48.7% of the total UHNW population in Indonesia. They have a combined fortune of US$12 billion or 9.8% of the total wealth of Indonesia's ultra affluent.

AGE DEMOGRAPHIC

The average age of the Indonesian UHNWI is 60. Wealth protection, estate taxes and wealth transfer are likely to take priority for these UHNWIs in the next decade.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For Indonesia ▼ DOWN ▼ DOWN ▼ DOWN ▲ UP ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

Hotspot

MONGOLIA

- Mongolia saw unprecedented GDP growth in 2011 of 17.3%, close to triple the rate in 2010 of 6.4%, according to the World Bank. The strength of Mongolia's economic growth remained strong with GDP rising 16.7% in Q1 2012.

- Unemployment fell from 13% in 2010 to 9% in 2011. The development of the Oyu Tolgoi mine continued to have a strong spillover effect on the rest of the economy, including the positive impact on consumer and business sentiment.

- The sharp rise in government spending that reached a record 56% of GDP in 2011 and budgeted to rise by another 32% in 2012, fuelled by sharply rising resource revenues, has led to concern that the Central Asian economy is overheating. There are fears that pro-cyclical fiscal policies could result in a repetition of a "boom-bust" cycle for Mongolia, particularly as a global economic slowdown in growth could result in sharp declines in mineral prices and in turn, government revenues. To meet the requirements of the 2% structural deficit ceiling under the Fiscal Stability Law that comes into force in January 2013, Mongolia is expected to undergo severe fiscal tightening in 2013 to reduce structural deficit (last seen at 6.1% of GDP in April 20i2)to meet targets set out under the law.

- Liquidity risks are on the rise with bank lending having expanded by a staggering 73% year-on-year in 2011. Loan books are seeing increasing numbers of non-performing loans (NPLs). The ease of conversion between U.S. Dollar denominated and Mongolian Togrog currency accounts leaves the banking system vulnerable to capital flight. Further macroeconomic instability could expose liquidity and asset quality vulnerabilities in individual banks and the banking system.

- Strong growth was seen for exports, with coal shipments to China constituting a major component of total exports. Mongolia also saw record FDI inflows of US$ 5.3 billion, a hefty 62% of GDP.

- High domestic inflation and declining commodity prices near the end of 2011 led to an 11% depreciation in the Mongolian Togrog in 2011. Rising inflation reflected demand related pressures from higher government spending and rising food prices.

- While Mongolia has taken the right step with the establishment of the Fiscal Stability Fund, the amount of savings is insubstantial and leaves the country exposed to volatility in commodity prices.

- The World Bank has recommended that Mongolia adopts fiscal prudence, tightens fiscal and monetary policies to reduce inflation and takes action to reduce systemic risks in the banking sector.

- UHNWI population growth depends on stable economic growth, steady FDI inflows and continued demand for resources from emerging economies.

Mongolia 5 Year Forecast Population Growth % Total Wealth Growth % 2011 - 2012 14.3% 20% 2012 - 2013 11.4% 8.5% 2013 - 2014 11.7% 8.7% 2014 - 2015 8.1% 5.2% 2015 - 2016 12.6% 9.7% 2016 - 2017 8.4% 7% The wealth effect from the resource boom is expected to continue into the foreseeable future with potential volatility in commodity prices and markets reflected in the uneven trend of growth in wealth and UHNW populations.

Based on GDP projections and key economic indicators, wealth growth for Mongolia will decline significantly from 2012-2013. Growth rates at present are partly the result of expansionary fiscal expenditure, which is expected to be curbed significantly in 2013 with the Fiscal Responsibility Law coming into effect. The dip in UHNW population growth rates and wealth growth rates in 2014-2015 is expected to be a side effect of the Fiscal Stability Law that takes effect from January 2013.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For Mongolia NEUTRAL ▼ DOWN ▼ DOWN ▲ UP ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

In the eye of the storm, Europe continues to be held hostage by mounting social unrest, political instability and speculative investment flows. On the back of weakened confidence, escalating financial stress stemming from sovereign debt crises, effects of deleveraging on the real economy and fiscal consolidation across the euro area, GDP for the region is expected to dip from an expansion of 1.4% in 2011 to a contraction of 0.3% in 2012, according to the IMF.

As deleveraging plays out in the public, household, and banking sectors across Europe, it is proving to be a force that is deepening the recession in most European economies. Observers and economists are increasingly concerned over signs that the core countries of the Eurozone are affected by the deleveraging process. Undoubtedly, the slow recovery of demand from emerging markets contributes to the situation, however, domestic factors are the main drivers.

The primary challenge for Europe is to balance the much needed recapitalization and restructuring with measures that counter the side effects of tighter credit supply. Similar balance is required for fiscal adjustment, more commonly referred to as austerity measures. Apart from the political capital tied to such measures, fiscal adjustment that is overly rapid may strangle economic growth which is vital for the viability of any long term repayment and restructuring schemes.

The prospects for consumption are weak due to the decline in confidence, employment and income coupled with high debt in various economies on the Eurozone periphery. Of particular concern is the high level of youth employment in these countries. However, Germany and some of its northern neighbours may break the pattern, reinforcing the perception of a two-speed Europe.

UHNW population growth has been adversely affected by the Eurozone crisis and the implications of stricter tax regimes pursued by financially distressed governments.

Wealth-X analysis has identified Europe as the home of 53,441 UHNW individuals with a combined net worth of close to US$ 7 trillion. There are 1,054 individuals who have left the ranks of the ultra wealthy. Europe saw a 1.9% reduction in its ultra wealthy population.

Spain, France and Italy suffered the largest absolute drop in terms of UHNW population. In contrast, Luxembourg and Denmark showed strong growth in UHNW populations, underlining the strength of Scandinavian countries in the region. Total wealth for the region declined by US$190 billion or 2.7%.

This Year's This Year's Last Year's Last Year's Europe UNHW Population Total Wealth

US$ billionUNHW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %1 Germany 15,770 2,050 15,985 1,945 -1.3% 5.4% 2 UK 10,515 1,325 10,490 1,275 0.2% 3.9% 3 Switzerland 5,595 655 5,220 635 7.2% 3.1% 4 France 4,100 475 4,415 535 -7.1% -11.2% 5 Italy 1,940 220 2,245 270 -13.6% -18.5% 6 Spain 1,520 180 1,880 225 -19.1% -20% 7 Norway 1,370 155 1,345 160 1.9% -3.1% 8 Netherlands 1,205 135 1,225 145 -1.6% -6.9% 9 Russia 1,145 605 1,290 710 -11.3% -14.8% 10 Sweden 990 110 970 115 2.1% -4.3% 11 Turkey 830 95 800 95 3.8% 0% 12 Portugal 785 90 795 95 -1.3% -5.3% 13 Poland 775 90 875 105 -11.4% -14.3% 14 Belgium 750 85 775 95 -3.2% -10.3% 15 Denmark 685 75 630 75 8.7% 0% 16 Luxembourg 655 65 600 70 9.2% -7.1% 17 Ireland 570 65 550 65 3.6% 0% 18 Austria 530 60 610 75 -13.1% -19.5% 19 Ukraine 480 55 560 65 -9.4% -15.1% 20 Greece 455 50 445 50 2.2% 0% 21 Finland 405 45 405 50 0% -10% 22 Hungary 365 40 390 45 -6.4% -11.1% 23 Croatia 260 30 260 30 0% 0% 24 Czech Republic 260 30 250 30 4% 0% 25 Monaco 195 23 200 24 -2.5% -5.9% 26 Romania 124 14 125 15 0% -8.4% 27 Belarus 115 13 110 13 4.1% -3.3% 28 Georgia 105 12 105 13 -0.4% -6.5% 29 Serbia 90 11 120 15 -25.3% -25% 30 Bosnia and Herzegovina 85 9 65 8 30.2% 13.3% 31 Lithuania 80 9 80 10 -0.4% -8% 32 Liechtenstein 75 8 75 9 -0.4% -12.7% 33 Moldova 75 8 70 9 6.7% -6.5% 34 Slovenia 70 8 75 9 -7.0% -12.7% 35 Iceland 65 7 65 8 -0.4% -11.9% 36 Latvia 65 8 65 8 -0.4% 0.7% 37 Albania 55 7 55 7 -0.4% 4.1% 38 Slovakia 45 5 55 7 -18.5% -25.6% 39 Cyprus 45 5 50 6 -10.4% -18.2% 40 Bulgaria 45 5 45 6 -0.4% -9.1% 41 Estonia 40 4 40 5 -0.4% -18.2% 42 Macedonia 35 4 35 4 -0.4% -6.5% 43 Montenegro 21 2 20 2 4.6% -18.2% 44 Andora 19 2 20 2 -5.4% -18.2% 45 Malta 16 2 15 2 6.2% 9.1% Rest of Europe 20 2 20 2 -0.4% -18.2% TOTAL 53,440 6,950 54,495 7,140 Europe Population Change % -1.9% Europe Wealth Change % -2.7% The region as a whole saw a loss in total wealth driven largely by developments in the peripheral Eurzone countries and those bordering the Eurozone as increasing uncertainty drove wealth flows from the periphery towards core economies such as Germany as well as popular safe havens that include the United Kingdom and Switzerland. Growth in wealth in the United Kingdom, Switzerland and Germany has helped to ameliorate the situation for Europe as a whole. Future growth in UHNW populations and wealth is dependent on Eurozone member states reaching a satisfactory resolution of the sovereign finance and credit crisis that has played out across the region, particularly one that ensures long term stability. It is our opinion that should the ongoing crisis continue unabated, an eventual decline in both UHNW population and total wealth will be inevitable for Europe.

Significant Drivers:

- THE UNITED KINGDOM: GDP was stagnant with a downward bias along side a 2.4% decrease in the equity markets during the measuring period. The British Pound saw a devaluation of 4%.

- GERMANY: GDP stagnated accompanied by a 2.6% fall in equity markets and a 13% devaluation of the Euro.

- SWITZERLAND: The healthy 15% rise in equity markets outweighed the limited growth in GDP. However, the Swiss Franc saw a large devaluation of more than 24% during the measuring period.

Hotspot

GERMANY

- Europe's largest economy faces the difficult task of restoring some semblance of health to the monetary union while dealing with growing domestic dissatisfaction over perceptions that Germany has taken an overly large share of the bailout burden. Despite increasing pessimism surrounding its economic outlook due to the ongoing Eurozone crisis, Germany retained a stable outlook for its Standard & Poor's long-term debt sovereign rating.

- After a drop to 3.1% in 2011, Germany is expected to see GDP growth decline sharply to 0.6% in 2012 on the back of a spiralling sovereign crisis enveloping the Eurozone. While observers have noted that a two-speed Europe is developing with core economies like Germany decoupling from fragile periphery economies, they are of the opinion that Germany needs to recognise its fortunes are fundamentally tied to the Eurozone.

- An intensification of the Eurozone crisis will impact the German economy directly through the trade and financial links that bind it to the Eurozone as well as indirectly through impact on business and consumer confidence that is barely recovering. To secure financial stability in the Eurozone, Germany needs to help peripheral economies by allowing the labour markets in these economies to become more competitive without resorting to the reduction of nominal wages. This entails tolerance for more rapid wage growth within Germany.

- According to Mr Subir Lall, IMF Mission Chief to Germany, in a conference call on Germany on 3 July 2012, the German banking system as a whole (outside of the Sparkassen sector) is vulnerable to external developments due to large cross-border exposures. Other vulnerabilities include significant reliance on wholesale financing, high leverage ratios and the poor quality of bank capital. However, Germany has the capacity for appropriate easing measures and fiscal stimulus should external downside risks materialise.

- German demand for exports from peripheral Eurozone economies could be boosted through a combination of faster wage growth and higher inflation levels. This combination should set the stage for healthy consumption growth that boosts domestic demand as well as the labour and investment markets.

- �The German luxury market saw rapid growth in 2011 with sales across luxury sectors estimated to have risen by 16%. The potential of the German market, which currently accounts for only 0.3% of GDP, is in part enhanced by the development of an increasingly positive attitude among German consumers towards luxury products. Thanks to higher incomes and a robust labour market, German consumer confidence has been largely unaffected by the Eurozone's deepening fiscal crisis. On a related front, the rise of luxury tourism has had a positive impact on the German market with Chinese and Russian tourists increasing their spending by close to 50% on average in 2011.

- UHNW population growth was strengthened by the perception of Germany as the most stable of the Eurozone economies and further escalation of the crisis will accelerate this trend.

Germany UHNWI This Year's This Year's Net Worth UHNWI TOTAL WEALTH

US$ billion$1 billion + 137 550 $750 million to $999 million 180 140 $500 million to $749 million 640 325 $250 million to $499 million 810 260 $200 million to $249 million 700 145 $100 million to $199 million 1,210 130 $50 million to $99 million 4,775 260 $30 million to $49 million 7,320 240 TOTAL 15,770 2,050 Population Change % -1.3% Wealth Change % 5.4% Wealth-X analysis shows there are i37 billionaires in the country. This group of billionaires, representing the top 0.9% of the UHNW population, control 26.8% of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth US$4 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 46.4% of the total UHNW population in Germany. They have a combined fortune of US$240 billion or 11.7% of the total wealth of the German ultra affluent segment.

TOP FIVE CITIES IN GERMANY BY UHNW POPULATION

German Cities UNHW Population By City Munich 1,595 Dusseldorf 1,380 Hamburg 1,345 Frankfurt 1,135 Stuttgart 1,120

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For Germany ▼ DOWN ▼ DOWN ▼ DOWN ▲ UP ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

Hotspot

SWITZERLAND

- Widely and traditionally recognised as a safe haven for wealth, Switzerland had expected to see GDP growth decline from 1.9% in 2011 to 0.8% in 2012, according to the IMF. However, the outlook for Switzerland has improved recently with its State Secretariat for Economics (SECO) forecasting GDP growth of 1.4% for 2012.

- These positive growth forecasts are significantly dependent upon the assumption that European economic policy is successful in preventing an uncontrolled proliferation of the crisis into a widespread banking and financial crisis, as the SECO noted.

- The first hint of insularity was displayed in the imposition of a cap on the franc by the Swiss National Bank in September 20ii has helped shield the economy from greater impact on trade and export margins due to the strength of the currency. On the export front, Germany, the largest consumer of Switzerland's exports, is expected to experience robust domestic demand growth. This is expected to help to offset the negative effects of the strong franc.

- The impetus towards insularity was further reinforced with the re-imposition of quotas on immigrants from eight other central and eastern European nations, in an effort to protect Swiss citizens' interest and keep unemployment levels at a target of 3%.

- Robust domestic demand has helped offset the effects of a strong franc on the export front. Strong local consumption led to national output expanding close to 2% in Q1 2012.

- The UBS Swiss Real Bubble Index, launched in May 2011 to study the risk of a property bubble in the Swiss residential housing market, declined for the first time in four years in Q2 2012 from a peak in Q1 2012. The imposition of minimum requirements for mortgage financing in July 2012 is expected to help curb demand for residential property and reduce price growth rates.

- The scrutiny of and crackdown on Swiss banking institutions on the back of suspicion surrounding their role in tax-evasion schemes has tarnished their reputation and contributed to the dismantling of the code of secrecy that has been a critical part of the Swiss banking sector for decades. Switzerland's Federal Department of Finance announced on 18 July 2012 that it intends to implement legislation which will allow Switzerland's tax authorities to share greater amounts of information on overseas residents who hold bank accounts in Switzerland. Such measures will better facilitate the sharing of data regarding suspected cases of tax evasion. As financially distressed governments seek to rejuvenate state finances, the pressure on Swiss banking institutions and authorities is set to increase.

- Observers have reported European investors resorting to stashing cash and gold bullion in Switzerland in a bid to protect their wealth from global economic uncertainty. The fallout from the Eurozone crisis and quantitative easing measures pursued by central banks have resulted in increasingly risk averse investors seeking safe havens and safe assets that retain value should inflation levels surge.

- Credit Suisse, one of Switzerland's biggest banks, adopted measures to boost its capital base after the Swiss National Bank's annual financial stability report pointed out that Swiss banks in general were inadequately prepared for deteriorating economic conditions in Europe or shocks from the domestic real estate market. The Swiss National Bank singled out UBS and Credit Suisse for criticism related to the need to reduce risk and strengthening capital reserves. Both banks hold close to US$250 billion of domestic mortgage debt, with half in property in regions, such as Zurich and Geneva, where the housing markets are overheating.

- UHNW population growth has benefitted from the flight to safety impetus across the Eurozone and looks set to continue.

Switzerland UHNWI This Year's This Year's Net Worth UHNWI Total Wealth

US$ billion$1 billion + 57 125 $750 million to $999 million 60 50 $500 million to $749 million 220 115 $250 million to $499 million 295 90 $200 million to $249 million 230 50 $100 million to $199 million 445 45 $50 million to $99 million 1,695 90 $30 million to $49 million 2,595 90 TOTAL 5,597 655 Population Change % 7.2% Wealth Change % 3.1% Wealth-X analysis shows there are 57 billionaires in the country. This group of billionaires, representing the top 1% of the UHNW population, control 19.1% of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth US$2.2 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 46.4% of the total UHNW population in Switzerland. They have a combined fortune of US$90 billion or 13.7% of the total wealth of the Swiss ultra affluent segment.

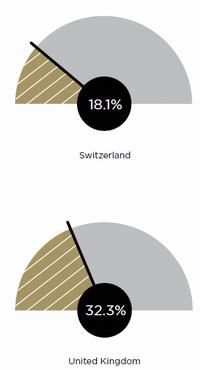

NON-DOMICILED UHNWIs

The data reflects the trends in the composition of the UHNW population in Switzerland, often viewed as a traditional favourite for global UHNWIs for taxation and privacy reasons.

Non-domiciled UHNWIs account for 18.1% of the Swiss UHNW population, which is in stark contrast to the 32.3% figure for the United Kingdom. A reason for the phenomenon may be the Swiss economy's reliance on certain industrial sectors, including machinery, chemicals and banking, as well as the smaller size of the Swiss labour market, which is only a sixth of the British labour market.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For Switzerland ▼ DOWN ▼ DOWN ▲ UP ▲ UP ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

Hotspot

UNITED KINGDOM

- Despite being widely seen as a favoured safe haven amid the economic, political and social crises on the European Continent, the United Kingdom is faced with the prospect of recession in 2012. Having seen GDP decline from 2.1% in 2010 to 0.7% in 2011, the United Kingdom is set to see a further decline in 2012 to 0.5% according to the OECD.

- The near-record levels of cash held by corporate entities are seen as an indication of caution on their part and a form of insurance against volatility and rapid shifts in the availability of capital. This heightens concern as private sector capital expenditure and investment are seen to be key to any recovery. Particularly as the United Kingdom is into its third year of fiscal austerity and government spending is not expected to contribute to the recovery.

- Consumption faces mixed fortunes as households are expected to face years of deleveraging and rising unemployment which may only be offset by declining inflation rates that could support real incomes.

- Despite current wealth inflows from risk adverse European UHNWs, recent research suggests a potential reverse in these capital flows will emerge on the back of massive devaluation across the Continent should countries exit the euro. A reversal in capital flows may have an adverse effect on the short term outlook for the financial services industry.

- The luxury property sector in the United Kingdom remains the envy of many as it has seen positive growth over recent years with foreign investors buying luxury homes in the United Kingdom, specifically London, to preserve wealth.

- Apart from residential property, UHNW investors are moving into the commercial real estate space. According to Jones Lang LaSalle, a global real estate services firm, 65% of the Central London office market was purchased by foreign investors in 2011 hailing from 30 countries. Jones Lang LaSalle estimated that in 2011, US$80.6 billion of overseas investor equity targeted real estate in the United Kingdom with London dominating interest. However, a potential Eurozone breakup will lead to massive devaluation across the Continent that will lead to a subsequent reverse in capital flows. The consequences for the luxury property sector could be devastating with a drop of up to 50% in London property prices.

- The decision to scrap plans to cap tax relief on charitable donations means the estimated US$2.1 billion of donations on which relief is claimed each year has been secured, much to the relief of the fundraising sector.

- UHNW population and wealth growth has benefited from the perception that the United Kingdom is a safe haven for wealth in uncertain economic conditions.

United Kingdom UHNWI This Year's This Year's Net Worth UHNWI Total Wealth

US$ billion$1 billion + 140 430 $750 million to $999 million 80 65 $500 million to $749 million 195 105 $250 million to $499 million 375 105 $200 million to $249 million 405 90 $100 million to $199 million 1,080 185 $50 million to $99 million 2,750 165 $30 million to $49 million 5,490 180 TOTAL 10,515 1,325 Population Change % 0.2% Wealth Change % 3.9% Wealth-X analysis shows there are 140 billionaires in the country. This group of billionaires, representing the top 1.3% of the UHNW population, control 32.5% of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth US$3.1 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 52.2% of the total UHNW population in the United Kingdom. They have a combined fortune of US$180 billion or 13.6% of the total wealth of the British ultra affluent segment.

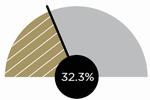

THE DIVERSE FACE OF WEALTH

Ethnic Group % of UHNW population Black 1.2% Caucasian 61.9% Chinese & North Asian 4.2% Hispanic 0.3% Middle Eastern 4.1% South Asian 28.3% NON-DOMICILED UHWNIs

The data reflects the trends in the composition of the UHNW population in the United Kingdom. That non-domiciled UHNWs account for 32.3% of the UHNW population of the United Kingdom points towards the emergence of UHNWIs who are global in their outlook and lifestyles.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For United Kingdom NEUTRAL ▼ DOWN ▼ DOWN ▲ UP ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

LATIN AMERICA

PLENTIFUL OPPORTUNITIESLatin America has seen steady growth over much of the last decade, fuelled by favourable commodity prices and the ready supply of international credit. Many Latin American governments used increased revenues in economically sound ways. Consequently, the region in general has seen deficits turn to surpluses and lower debt to GDP ratios. The investment in targeted social programs has resulted in a reduction in regional poverty levels.

GDP growth for the region declined sharply from 6.2% in 2010 to 4.5% in 2011 and is expected to slide further to 3.7% in 2012, according to the IMF. However, observers see the region continuing to converge towards its potential long term growth rate. Across the region, the pace of growth is expected to be uneven, with a split between countries that have strong links with the U.S. and those who are subject to Asian influences and whose economies are largely domestically driven. Venezuela and Argentina, in particular, are expected to see economic contraction due to the erratic nationalization policy trend in Argentina and political uncertainty in Venezuela that have caused unease amongst investors. Countries in the region generally have manageable fiscal deficit positions, allowing governments to play more dominant roles and adopt stimulus strategies should external shocks, such as impact from the Eurozone crisis, materialise.

The region is expected to see domestic demand outstrip GDP growth in 2012, stoked by buoyant consumer confidence and strong credit market performance. Regional performance is as much shaped by internal factors as high export prices that ensure trade deficits are manageable. Foreign investors tend to see potential primarily in the infrastructure and resource sectors and FDI flows into the region that target these sectors have been significant. On the other hand, the risks of overheating remain as high commodity prices and ebullient domestic demand heighten inflationary risks. Central banks in the region are expected to try to offset inflationary and currency pressures through the adoption of macroprudential policies.

Challenges that countries face run the gamut from labour market rigidities to the impetus towards trade protectionism and political uncertainty, reflecting both the diversity and complexity of the region.

UHNW population growth has accelerated off the back off strong economic performance across the region.

This Year's This Year's Last Year's Last Year's Latin America UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billionPopulation

Change %Total

Wealth Change %1 Brazil 4,640 865 4,725 925 -1.8% -6.5% 2 Mexico 3,240 430 2,900 420 11.7% 2.4% 3 Argentina 1,040 140 1,050 150 -1% -6.7% 4 Colombia 690 85 675 90 2.2% -5.6% 5 Peru 595 70 580 75 2.6% -6.7% 6 Chile 550 70 560 75 -1.8% -6.7% 7 Venezuela 420 55 375 50 12% 10% 8 Ecuador 250 30 230 30 8.7% 0% 9 Dominican Republic 240 30 225 30 6.7% 0% 10 Guatemala 235 28 230 30 2.2% -26.7% 11 Bolivia 220 30 200 28 10% 7.1% 12 Honduras 205 27 185 26 10.8% 3.8% 13 Nicaragua 190 26 180 25 5.6% 4% 14 Paraguay 165 22 150 22 10% 0% 15 El Salvador 145 20 140 20 3.6% 0% 16 Uruguay 115 16 105 16 9.5% 0% 17 Panama 105 15 110 14 5% 7.1% 18 Puerto Rico 100 14 100 14 0% 0% 19 Costa Rica 85 12 110 18 -22.7% -33.3% 20 Cuba 45 6 45 7 0% -14.3% Rest Of Latin America 1,475 195 1,380 195 6.9% 0% TOTAL 14,750 2,185 14,245 2,260 Latin America Population Change % 3.5% Latin America Wealth Change % -3.3% Wealth-X analysis has identified Latin America as the home of 14,750 UHNW individuals with a combined net worth of close to US$ 2.2 trillion. There are 505 individuals who have joined the ranks of the ultra wealthy. Latin America saw an increase of 3.5% in its ultra wealthy population.

Wealth-X analysis shows Brazil and Chile suffered two of the the largest percentage reductions in UHNW population. In contrast, Venezuela's UHNW population increased by at least 12%, followed by Mexico. Total wealth for the region declined by US$74 billion or 3.3%.

The region as a whole saw an increase in UHNW population driven by growth in Mexico and Venezuela. Across the region, growth is largely driven by resource exports. Diversification is necessary for sustained growth in the future.

Significant Drivers:

- BRAZIL: GDP saw modest growth, however that was offset by the 10% decline in equity markets and the 31% devaluation in the Brazilian Real.

- VENEZUELA: GDP growth was matched by an unprecedented 172% rise in equity markets. However, the Venezuelan currency was stagnant.

Hotspot

BRAZIL

- Since early 2011, buoyant commodity prices, robust private consumption and investment activity have seen Brazil's economy the focus of much speculation and attention. Signs have emerged that the B in BRICs may be fading into the background.

- On the back of a global slowdown and the effects of tightening policies, Brazil is expected to see growth ease further to 1.9 % in 2012, according to a survey commissioned by the Brazilian central bank. This comes on the back of a sharp dip in GDP growth from 7.5% in 2010 to 2.7% in 2011.

- Europe's sovereign debt crisis has eroded demand for exports from emerging economies and reduced demand for resources. Any heightening of the crisis could lead to a sharp spike in risk aversion, a drop in commodity prices and a knock-on effect in major trading partners, particularly the US and China. As the impact reverberates along the global supply chain, commodity prices are likely to be constrained, contributing to slowing economic growth in Brazil for 2012.

- The easy availability of credit particularly in 2003-2008 created a credit boom. With the fizzling of Brazil's decade-long credit binge, further drag on the real economy has been created. Consumer spending, which accounted for close to 60% of GDP, has declined, leading to speculation that this is the beginning of the end of a debt-fuelled consumer spending boom.

- Going forward, Brazil's central bank is expected to pursue monetary easing policies amid the current weak patch and a perceived need to lower interest rates to ease the effect of earlier tightening measures.

- Brazil's attraction as an investment destination is supported by its net global creditor status, stable external liquidity position as well as enviable international reserves, which are approaching the US$380 billion mark, approximately half the region's reserves. Though the negative impact of an appreciating currency is widely recognised, there is official support for policies that support a strong Brazilian Real. The Real is expected to appreciate in view of excess global liquidity and investor thirst for high yield investment options, particularly in terms of global fixed income investments.

- Further liberalisation of state-controlled sectors and companies, such as state-controlled banks and Petrobras, could boost Brazil's attraction for investors, who have felt locked out by state controlled monopolies. Brazil reportedly received close to US$60 billion FDI flows from June 2011-2012.

- The need to invest in energy and transport infrastructure, prerequisites for future growth, is urgent and should be at the forefront of government policy. Significant capital spending on the part of Petrobras to exploit vast ocean-based oil reserves is expected to be accompanied by the continued auction of assets to stimulate private sector investment in infrastructure. Such projects are expected to drive growth and productivity while improving public finances.

- Hurdles that Brazil potentially faces include, the inclination towards increased trade protectionism, perceived growth in corruption and the need to address challenges faced by the manufacturing sector in relation to the tax structure.

- UHNW population growth has suffered from the steep drop in GDP growth but may stabilize should appropriate policies be adopted.

This Year's This Year's Last Year's Last Year's Brazil UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth

US$ billion$1 billion + 49 300 50 320 $750 million to $999 million 30 25 30 27 $500 million to $749 million 135 85 140 90 $250 million to $499 million 295 100 300 115 $200 million to $249 million 420 95 430 100 $100 million to $199 million 620 95 630 100 $50 million to $99 million 1,200 90 1220 95 $30 million to $49 million 1,895 75 1925 80 TOTAL 4640 865 4725 925 Population Change % -1.8% Wealth Change % -6.5% Wealth-X analysis shows there are 49 billionaires in the country. This group of billionaires, representing the top 1.1% of the UHNW population, control 34.7% of the total fortune attributable to the ultra wealthy segment. On average, these billionaires are worth US$6.1 billion each.

The lowest tier of the UHNW group represented by those worth US$30 million to US$49 million is the largest group, making up 40.8% of the total UHNW population in Brazil. They have a combined fortune of US$75 billion or 8.7% of the total wealth of Brazil's ultra affluent.

MOBILE AND VERSATILE

The Brazilian UHNW population is mobile and versatile, with at least 10% of UHNWIs conducting business primarily outside of Brazil and at least 9% owning residences outside of Brazil.

Major Wealth Indicators GDP* Currency Equity Property Luxury Spending For Brazil ▲ UP ▼ DOWN ▼ DOWN NEUTRAL ▲ UP

Note: *All GDP growth rates are measured relative to the previous year's growth rate.

MIDDLE EAST AND AFRICA

WEALTH AMONGST VOLATILITYThe Middle East faces fiscal sustainability and structural issues. The region's growing population of youths will incease the demand for jobs in the future and the limited supply of oil point towards the increasingly important need to accelerate economic diversification. The petrodollar liquidity flush that the region is experiencing should be channeled into avenues that boost sustainable economic growth. This requires an expansion of financial markets in the region.Amidst the spike in oil prices, increasing tensions in the Middle East and Africa, both regions may see political uncertainty hampering growth potential. Economic activity within the North African region is tempered by geopolitical unrest within the region. Countries such as Egypt, that are slowly rebuilding after the Arab Spring of 2011, have yet to find a firm grip on the economic and political compass guiding their future. UHNW population growth was stable despite political uncertainty and looks set to grow as political stability returns to the region.Meanwhile, growth in sub Saharan Africa has not shown any signs of decline, but rather reflects the encouragement of positive commodity prices. Despite the promising picture, Africa, like other emerging economies, is susceptible to Europe's ongoing crisis. The gloom in Europe may prove to be the drag on economic expansion in Africa and the Middle East through the reduced demand for oil and an increase in risk aversion amongst investors. However, China's controversial series of investments in Africa reflects the continuing attraction of the resource-rich African continent. UHNW population growth has thrived off the back off demand for resources from emerging economies.

The Middle East and Africa are home to at least 7,130 UHNW individuals with a combined net worth of at least US$1 trillion. The steady pace of increase in the population of UHNW individuals reflects the tremendous potential of the two regions despite the political uncertainty that overshadows them.

There are 4,595 UHNW individuals in the Middle East, with a total net worth of US$710 billion. The Middle East saw an increase of 2.2 % in its ultra wealthy population. Overall combined wealth for the Middle East UHNW population saw a decrease of 1.3%.

This Year's This Year's Last Year's Last Year's Middle East UHNWI UHNW Population Total Wealth

US$ billionUHNW Population Total Wealth