jul12

Memorandum of Understanding on Financial-Sector Policy Conditionally for Spain

- VS-NfD -

Draft 9.07.2012SPAIN

Memorandum of Understanding on Financial-Sector Policy Conditionally

xx July 2012

With regard to the EFSF Framework Agreement, and in particular Article 2 (1) thereof, this Memorandum of Understanding on financial-sector policy conditionality (MoU), details the policy conditions as embedded in Council Decision [...] of 20 July 2012 on specific measures to reinforce financial stability in Spain. Given the nature of the financial support provided to Spain, conditionality will be financial-sector specific and will include both bank-specific conditionality in line with State aid rules and horizontal conditionality. In parallel, Spain will have to comply fully with its commitments and obligations under the EDP and the recommendations to address macroeconomic imbalances within the framework of the European Semester. Progress in meeting these obligations under the relevant EU procedures will be closely monitored in parallel with the regular review of programme implementation.

For the duration of the EFSF financial assistance, the Spanish authorities will take all the necessary measures to ensure a successful implementation of the programme. They also commit to consult ex-ante with the European Commission, and the European Central Bank (ECB) on the adoption of financial-sector policies that are not included in this MoU but that could have a material impact on the achievement of programme objectives - the technical advice of the International Monetary Fund (IMF) will also be solicited. They will also provide the European Commission, the ECB and the IMF with all information required to monitor progress in programme implementation and to track the financial situation. Annex 1 provides a provisional list of data requirements.

I. Introduction 1. On 25 June 2012, the Spanish Government requested external financial assistance in the context of the ongoing restructuring and recapitalisation of the Spanish banking sector. The assistance is sought under the terms of the Financial Assistance for the Recapitalisation of Financial Institutions by the EFSF. Following this request, the European Commission in liaison with the ECB, the European Banking Authority (EBA) and the IMF conducted an independent assessment of the eligibility of Spain's request for such assistance. This assessment concluded that Spain fulfils the eligibility conditions. The Heads of State and Government at the Euro Area Summit of 29 June 2012 specified that the assistance will subsequently be taken over by the ESM, once this institution is fully operational, without gaining seniority status. The full implementation of this MoU will take into account all other relevant considerations contained in the Euro Area Summit statement of 29 June 2012.

II. Recent economic and financial developments and outlook 2. The global financial and economic crisis exposed weaknesses in the growth pattern of the Spanish economy. Spain recorded a long period of strong growth, which was, in part, based on a credit-driven domestic demand boom. Very low real interest rates triggered the accumulation of high domestic and external imbalances as well as a real estate bubble. The sharp correction of that boom in the context of the international financial crisis led to a recession and job destruction.

3. The unwinding of economic imbalances is weighing on the growth outlook. Private sector deleveraging implies subdued domestic demand in the medium term. Sizable external financing needs increase the vulnerability of the Spanish economy. A shift to durable current account surpluses will be required to reduce external debt to a sustainable level. Public debt is increasing rapidly due to persistently high general government deficits since the beginning of the crisis linked to the shift to a much less tax-rich growth pattern.

4. The challenges that face segments of the banking sector continue to negatively affect the economy as the credit flow remains constrained. In particular, sizeable exposure to the real estate and construction sectors have eroded investor and consumer confidence. As the linkages between the banking sector and the sovereign have increased, a negative feedback loop has emerged. Therefore, restructuring (including, where appropriate, orderly resolution) and recapitalisation of banks is key to mitigating these linkages, increasing confidence, and spurring economic growth.

5. With the exception of a few large and internationally diversified credit institutions, Spanish banks have lost access to wholesale funding markets on affordable terms. As a result, Spanish banks have become highly dependent on Eurosystem refinancing. Moreover, the borrowing capacity of Spanish banks has been severely limited by the impact of rating downgrades on collateral availability.

III. Key objectives 6. The Spanish banking sector has been adversely affected by the burst of the real estate and construction bubble and the economic recession that followed. As a result, several Spanish banks have accumulated large stocks of problematic assets. Concerns about viability of some of these banks are a source of market volatility.

7. The Spanish authorities have taken a number of important measures to address the problems in the banking sector. These measures include the clean-up of banks' balance sheets, increasing minimum capital requirements, restructuring of the savings bank sector, and significantly increasing the provisioning requirements for loans related to Real Estate Development (RED) and foreclosed assets. These measures, however, have not been sufficient to alleviate market pressure.

8. The main objective of the financial sector programme in Spain is to increase the long-term resilience of the banking sector as a whole, thus, restoring its market access.

- As part of the overall strategy, it is key to effectively deal with the legacy assets by requiring a clear segregation of impaired assets. This will remove any remaining doubts about the quality of the banks' balance sheets, allowing them to better carry out their financial intermediation function.

- By improving the transparency of banks' balance sheets in this manner, the programme aims to facilitate an orderly downsizing of bank exposures to the real estate sector, restore market-based funding, and reduce banks' reliance on central bank liquidity support.

- Additionally, it is essential to enhance the risk identification and crisis management mechanisms which reduce the probability of occurrence and severity of future financial crises.

IV. Restoring and strengthening the soundness of the Spanish banks:

Bank-specific conditionality9. The key component of the programme is an overhaul of the weak segments of the Spanish financial sector. It will be comprised of the following three elements:

- identification of individual bank capital needs through a comprehensive asset quality review of the banking sector and a bank-by-bank stress test, based on that asset quality review;

- recapitalization, restructuring and/or resolution of weak banks, based on plans to address any capital shortfalls identified in the stress test; and

- segregation of assets in those banks receiving public support in their recapitalization effort and their transfer of the impaired assets to an external Asset Management Company (AMC).

Roadmap

10. The recapitalisation and restructuring of banks will advance according to the following timeline.

- In July 2012, the programme will begin by providing a first tranche. In particular, until recapitalisation of banks has been fully effected, individual banks may find themselves at risk. Against the background of continued sovereign funding strains and extremely limited access by some banks to external funding, the financial situation of banks remains tight. Under these conditions, the ready availability of a credible backstop to be mobilised in case of emergency to cover for the costs of unexpected interventions contribute to restore confidence. The first tranche will have a volume of EUR 30 billion to be prefunded and kept in reserve by the EFSF. The possible use of this tranche ahead of the adoption of restructuring decisions by the European Commission will require a reasoned and quantified request from the Banco de Espana, to be approved by the European Commission and the Euro Working Group (EWG) and in liaison with the ECB.

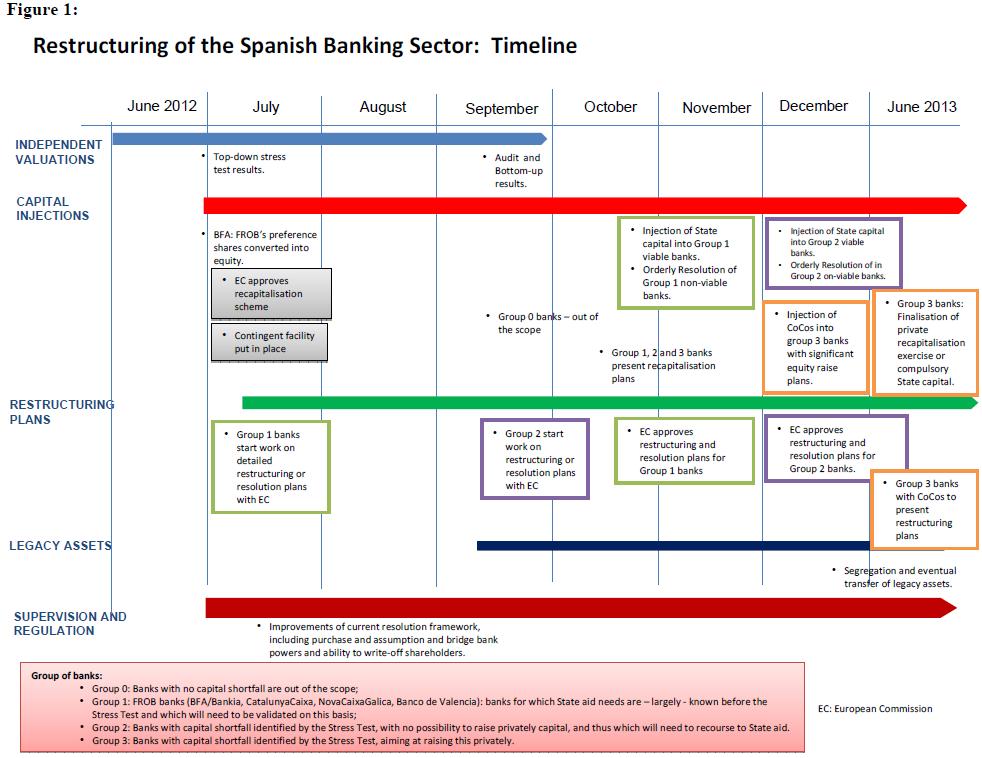

- A bank-by-bank stress test conducted by an external consultant with regard to 14 banking groups comprising 90% of the Spanish banking system will be completed by the second half of September 2012 (Stress Test). The Stress Test, following the results of the top-down exercise published on 21 June 2012, will estimate the capital shortfalls for individual banks and give rise to a recapitalisation and restructuring process for groups of banks as set out in Figure 1.

- On the basis of the stress test results and recapitalisation plans, banks will be categorised accordingly. Group 0 will constitute those banks for which no capital shortfall is identified and no further action is required. Group 1 has been pre-defined as banks already owned by the Fund for Orderly Bank Restructuring (FROB) (BFA/Bankia, Catalunya Caixa, NCG Banco and Banco de Valencia). Group 2 will constitute banks with capital shortfalls identified by the Stress Test and unable to meet those capital shortfalls privately without having recourse to State aid. Finally, Group 3 will constitute banks with capital shortfall identified by the stress test with credible recapitalisation plans and able to meet those capital shortfalls privately without recourse to State aid. The distributions of banks between groups 0, 2 and 3 will be established in October, based on the results of the Stress Test and an assessment of recapitalisation plans.

- By early-October, banks in Groups 1, 2 and 3 will present recapitalisation plans identifying how they intend to fill the capital shortfalls identified. Capital can be raised, chiefly, from internal measures, asset disposals, liability management exercises, and by raising equity or from State aid.

- The Spanish authorities and the European commission will assess the viability of the banks on the basis of the results of the Stress Test and the restructuring plans. Banks that are deemed to be non-viable will be resolved in an orderly manner.

- For Group 1 banks, the Spanish authorities will start preparing restructuring or resolution plans with the European Commission from July 2012 onwards. These plans will be finalised in light of the Stress Test results and presented in time to allow the European Commission to approve them by November 2012. On this basis, State aid will be granted and plans can be implemented immediately. The process of moving impaired assets to an external AMC will be completed by year end. These banks are expected to have the largest capital needs.

- For Group 2 banks, the Spanish authorities will need to present a restructuring or resolution plan to the European Commission by October 2012 at the latest. Given the need to incorporate the findings from the Stress Test, the approval process is expected to run until end-December when these banks will be recapitalized or resolved in an orderly manner. All Group 2 banks must include in their restructuring or resolution plan the necessary steps to segregate their impaired assets into an external AMC.

- For banks in Groups 1 and 2, no aid will be provided until a final restructuring or resolution plan has been approved by the European Commission, unless use has to be made of the funds of the first tranche.

- Group 3 banks planning a significant equity raise corresponding to more than 2% of RWA will, as a precautionary measure, be required to issue contingent convertible securities (cocos) under the recapitalisation scheme to meet their capital needs by end December 2012 at the latest - COCOs will be subscribed for by the FROB using programme resources and can be redeemed until 30 June 2013 if they succeed in raising the necessary capital from private sources. Otherwise they will be recapitalised through the total or partial conversion of the COCOs into ordinary shares. They will have to present restructuring plans.

- Group 3 banks planning a more limited equity raise corresponding to less than 2% of RWA will be given until 30 June 2013 to do so. Should they not succeed, they will be recapitalized by means of State aid and present restructuring plans.

- Group 3 banks that still benefit from public support under this programme on 30 June 2013, will be required in their restructuring plans to transfer the impaired assets to the AMC, unless it can be shown for banks requiring less than 2% of RWA in State aid that other means to achieve full off-balance sheet segregation are less costly.

Diagnostics

11. The Spanish authorities will complete an accounting and economic value assessment of the credit portfolios and foreclosed assets of 14 banking groups. The assessment will be conducted by an external consultant, based on inputs from four independent auditors as follows.

- Based on a predefined sample of operations the accounting review will include: (i) data quality analysis, including the appropriate identification of restructured/refinanced loans; (ii) verification of the proper classification of operations; (iii) review of the calculation of impairment losses; and (iv) computation of the impact of the new provisioning requirements for both performing and non-performing loans in the real estate and construction sector.

- The extended mandate of the due diligence process of the auditors will also capture the data required for an economic value assessment of the assets. This will include a wider sample, necessary to assess the systems and appropriateness of loan origination, classification and arrears management to check and adjust the current classification and risk parameters. The information obtained from the auditors will be combined with additional bank specific data, as requested by the consultant, from official authorities and directly from banks through direct interaction as needed. In addition, a rigorous appraisal of the value of collateral and foreclosed assets value will be required to fully inform a comprehensive asset quality review carried out by the external consultant.

12. The asset quality review will form the basis for a bank-by-bank stress test to be performed by the external consultant. It will also form the basis for any future valuation of Spanish bank assets (see paragraph 21). This Stress Test will build on the scenarios developed for the top down exercise, and will benefit from the granular information and asset quality review that is being gathered by independent firms through data verification and validation and take into account its loss absorption capacity. All information required for the Stress Test, including the results of the asset quality review, will be provided to the consultants by mid-August at the latest. The results of the Stress Test will be published in the second half of September 2012. The Banco de Espana and the European Commission, in consultation with the EBA and in liaison with the ECB, will establish the specific capital needs of each participating bank (if any).

13. In accordance with the appropriate governance structure established in the Terms of Reference for this exercise, a Strategic Coordination Committee ("SCC"), involving, together with the Spanish authorities, the European commission, the EcB, the EBA and the IMF and an Expert Coordination Committee ("ECC") will closely oversee the work carried out by the independent firms. The latter will provide full updates every two weeks to the SCC.

Recapitalisation, restructuring and/or resolution

14. The approach to bank restructuring and resolution is based on the principles of viability, burden sharing and limiting distortions of competition in a manner that promotes financial stability and contributes to the resilience of the banking sector. Recapitalisation plans involving the use of public funds will trigger a restructuring process. The restructuring plans of the banks requiring public funds will have to demonstrate that the long-term viability of the bank can be ensured without continuing State aid. The plans should focus on the bank's capacity to generate value for shareholders given its risk profile and business model, as well as the costs linked to the necessary restructuring. The degree of restructuring required will take due account of the relative size of the public support provided.

15. Restructuring plans will address the banks' ability to generate sustainable and profitable business going forward and their funding needs. The restructuring plans should be based on significant downsizing of unprofitable business with a focus on divestitures wherever feasible, de-risking through the separation of the most problematic assets, rebalancing of the funding structure, including a reduction of the reliance on central bank liquidity support, improved corporate governance and operational restructuring primarily through the rationalisation of branch networks and of staff levels. This should lead to a sustainable improvement in the cost-to-income ratios of the banks concerned. Non-listed entities should also present a credible timeline to eventually become publicly traded.

- The restructuring plans of viable banks requiring public support will detail the actions to minimise the cost on taxpayers. Banks receiving State aid will contribute to the cost of restructuring as much as possible with their own resources. Actions include the sale of participations and non-core assets, run off of non-core activities, bans on dividend payments, bans on the discretionary remuneration of hybrid capital instruments and bans on non-organic growth. Banks and their shareholders will take losses before State aid measures are granted and ensure loss absorption of equity and hybrid capital instruments to the full extent possible.

- For non-viable banks in need of public funds, the Spanish authorities have to submit an orderly resolution plan. Orderly resolution plans should be compatible with the goals of maintaining financial stability, in particular by protecting customer deposits, of minimising the burden of the resolution on the taxpayer and of allowing healthy banks to acquire assets and liabilities in the context of a competitive process. The orderly resolution process will involve the transfer of certain assets to the external AMC.

- The Spanish authorities commit to cap pay levels of executive and supervisory board members of all State-aided banks.

16. The Spanish authorities will take early and timely action on the restructuring and resolution plans. The authorities will immediately start liaising with the European Commission to ensure timely delivery of the restructuring plans. The restructuring plans will be submitted to the European Commission for assessment under State aid rules, and will be made available, once finalised, to the ECB, EBA and IMF. The Spanish authorities will provide all the necessary information on the restructuring or resolution plans as soon as the need for state aid is known. The process will commence immediately for Group 1 banks. For these banks, the Spanish authorities will work to put the European Commission in a position to approve the restructuring or resolution plans by November 2012. For those banks whose capital needs will become clear with the result of the bottom up stress test, the Spanish authorities will enter into the same process with the aim of ensuring that restructuring plans can be approved by the European Commission by December 2012. Recapitalisations will only take place after the adoption of a restructuring decision by the European Commission, requiring burden sharing and restructuring, unless funds of the first tranche are deployed.

Burden sharing

17. Steps will be taken to minimise the cost to taxpayers of bank restructuring. After allocating losses to equity holders, the Spanish authorities will require burden sharing measures from hybrid capital holders and subordinated debt holders in banks receiving public capital, including by implementing both voluntary and, where necessary, mandatory Subordinated Liability Exercises (SLEs). Banks not in need of State aid will be outside the scope of any mandatory burden sharing exercise. The Banco de Espana, in liaison with the European Commission and the EBA, will monitor any operations converting hybrid and subordinated instruments into senior debt or equity.

18. Legislation will be introduced by end-August 2012 to ensure the effectiveness of the SLEs. The Spanish authorities will adopt the necessary legislative amendments, to allow for mandatory SLEs if the required burden sharing is not achieved on a voluntary basis. These amendments should also include provisions allowing that holders of hybrid capital instruments and subordinated debt fully participate in the SLEs. By end-July 2012, the Spanish authorities will identify the legal steps that are needed to establish this framework, so that its adoption can be completed by end-August 2012. The Banco de Espana will immediately discourage any bank which may need to resort to State aid from conducting SLEs at a premium of more than 10% of par above market prices until December 2012.

19. Banks with capital shortfalls and needing State aid will conduct SLEs against the background of the revised legal framework and in accordance with State aid rules, by converting hybrid capital and subordinated debt into equity at the time of public capital injection or by buying it back at significant discounts. For Group 3 banks this rule will apply on 30 June 2013, if they still are in receipt of public funds. For non viable banks, SLEs will also need to be used to the full extent to minimise the cost for the tax payer. Any capital shortfall stemming from issues arising in the implementation of SLEs will not be covered by the EFSF assistance.

20. The bank resolution framework will be further upgraded. By end-August, the Spanish authorities, in consultation with the European Commission, the ECB and the IMF, will modify the bank resolution framework in order to incorporate relevant resolution powers to strengthen the FROB. This amendment will take into account the EU regulatory proposal on crisis management and bank resolution, including special tools to resolve banks, such as the sale of business tool and bridge banks; the legislation will also include a clarification of the financial responsibilities of the FGD (Deposit Guarantee Fund) and the FROB. The legislation will also include provisions on overriding shareholders rights in resolution processes.

Segregation of impaired assets: Asset Management Company

21. Problematic assets of aided banks should be quickly removed from the banks' balance sheets. This applies, in particular, for loans related to Real Estate Development (RED) and foreclosed assets. In principle, it will also apply to other assets if and when there are signs of strong deterioration in their quality. The principle underpinning the separation of impaired assets is that they will be transferred to an external AMC. Transfers will take place at the real (long-term) economic value (REV) of the assets. The REV will be established on the basis of a thorough asset quality review process, drawing on the individual valuations used in the Stress Test. The respective losses must be crystallized in the banks at the moment of the separation. The Spanish authorities, in consultation with the European Commission, the ECB and the IMF, will prepare a comprehensive blueprint and legislative framework for the establishment and functioning of this asset separation scheme by end-August 2012. The Spanish authorities will adopt the necessary legislation in the autumn with a view to assuring that the AMC will be fully operational by November 2012.

22. The AMC will manage the assets with the goal of realising their long-term value. The AMC will purchase the assets at REV and will have the possibility to hold them to maturity. The FROB will contribute cash and/or high quality securities to the AMC for an amount corresponding to a certain percentage (to be determined at the time of the establishment of the AMC) of the REV of the assets purchased. In exchange for the assets, the banks will receive a suitably small equity participation in the AMC, bonds issued by the AMC and guaranteed by the State, or cash and/or high quality securities. The bonds issued by the AMC will be structured in such a manner that they will meet the conditions set out in the ECB's "Guideline on monetary policy instruments and procedures of the Eurosystem".

V. Ensuring a sound framework for the banking sector:

Horizontal Conditionality23. A strengthening of the regulatory framework is critical to enhance the resilience of the Spanish banking sector. Spanish authorities will take additional measures in the following areas.

- Spanish credit institutions will be required, as of 31 December 2012, to meet until at least end-2014 a Common Equity Tier (CET) 1 ratio of at least 9%. The definition of capital used to calculate this solvency ratio will be based on that (eligible capital) established in the ongoing EBA recapitalisation exercise.

- From 1 January 2013, Spanish credit institutions will be required to apply the definition of capital established in the Capital Requirements Regulation (CRR), observing the gradual phase-in period foreseen in the future CRR, to calculate their minimum capital requirements established in the EU legislation. However, the additional capital needed to meet the 9% capital ratio will be calculated based on the capital definition established in the ongoing EBA recapitalisation exercise. In any case, Spanish credit institutions will not be allowed to reduce their capital base with respect to December 2012 figures, without previous approval from the Banco de Espana.

- The current framework for loan-loss provisioning will be re-assessed. On the back of the experiences of the financial crisis, the Spanish authorities will make proposals to revamp the permanent framework for loan loss provisioning, taking into account the temporary measures introduced during the past months, as well as the EU accounting framework. Furthermore, the authorities will explore the possibility to revise the calibration of dynamic provisions on the basis of the experience gathered during the current financial crisis. To this end, the authorities will submit by mid-December 2012, a policy document for consultation to the European Commission, ECB, EBA and IMF on the amendment of the provisioning framework if and once Royal Decree Laws 2/2012 and 18/2012 cease to apply.

- The regulatory framework on credit concentration and related party transactions will be reviewed. This review, to be carried out by the Spanish authorities by mid-January 2013, will in particular assess whether a strengthening of the regulatory framework is warranted.

- The liquidity situation of Spanish banks will continue being closely monitored. For the purpose of monitoring their liquidity position, credit institutions in receipt of State aid or for which capital shortfalls will be revealed in the Stress Test will, as of 1 December 2012, provide standardised quarterly balance sheet forecasts (funding plans) to the Banco de Espana and the ECB. The Banco de Espana will provide regular information on the liquidity situation of these banks to the European Commission, the ECB and the IMF, as specified in Annex 1.

- The governance structure of former savings banks and of commercial banks controlled by them will be strengthened. The Spanish authorities will prepare by end-November 2012 legislation clarifying the role of savings banks in their capacity as shareholders of credit institutions with a view to eventually reducing their stakes to non-controlling levels. Furthermore, authorities will propose measures to strengthen fit and proper rules for the governing bodies of savings banks and to introduce incompatibility requirements regarding the governing bodies of the former savings banks and the commercial banks controlled by them. Moreover, authorities will provide by end-November 2012 a roadmap for the eventual listing of banks included in the Stress Test, which have benefited from State aid as part of the restructuring process.

- Enhanced transparency is a key pre-requisite for fostering confidence in the Spanish banking system. Several important measures have already been taken to increase the quality and quantity of information provided by credit institutions to the general public, notably concerning real estate and construction sector exposures. The authorities released for public consultation a regulatory proposal aimed at enhancing and harmonising disclosure requirements for all credit institutions on key areas of their portfolios such as restructured and refinanced loans, sectoral concentration. This regulatory proposal will be finalised in consultation with the European Commission, the ECB, the EBA and the IMF and become effective by end of September 2012.

24. The supervisory framework will be strengthened. The Spanish authorities will take measures in the following areas.

- A further strengthening of the operational independence of the Banco de Espana is warranted. The Spanish authorities will transfer by31 December 2012 the sanctioning and licensing powers of the Ministry of Economy to the Banco de Espana. Furthermore, the Spanish authorities will identify by end October 2012 possibilities to further empower the Banco de Espana to issue binding guidelines or interpretations.

- The supervisory procedures of Banco de Espana will be further enhanced based on a formal internal review. The Banco de Espana will conduct a full internal review of its supervisory and decision-making processes by end-October 2012 in order to identify shortcomings and make all the necessary improvements. In this internal review, the Banco de Espana will test recent improvements made to the supervisory procedures in order to ensure that the findings of on-site inspections translate effectively and without delays into remedial actions. Specifically, the authorities will analyse the need for any further improvements in the communication to the decision making bodies of vulnerabilities and risk in the banking system, in order to ensure the adoption of corrective actions. Furthermore, the authorities will ensure that macro-prudential supervision will properly feed into the micro supervision process and adequate policy responses.

- The Banco de Espana will by end-2012 require credit institutions to review, and if necessary, prepare and implement strategies for dealing with asset impairments. The Banco de Espana will determine the operational capability of credit institutions to manage arrears, identify operational deficiencies and will monitor the implementation of these plans. The assessment of the adequacy of loan work-out strategies will also be based on the findings of the external auditors and consultants during the asset quality review.

25. Consumer protection and securities legislation, and compliance monitoring by the authorities, should be strengthened, in order to limit the sale by banks of subordinate debt instruments to non-qualified retail clients and to substantially improve the process for the sale of any instruments not covered by the deposit guarantee fund to retail clients. This should include increased transparency on the characteristics of these instruments and the consequent risks in order to guarantee full awareness of the retail clients. The Spanish authorities will propose specific legislation in this respect by end-February 2013.

26. The public credit register will be enhanced. The Spanish authorities will take additional measures to improve the quantity and quality of information reported to the register. The envisaged enhancements will be submitted for consultation with stakeholders by end-October 2012. Furthermore, the necessary legislative amendments will be in place by

27. Non-bank financial intermediation should be strengthened. In light of the high dependence of the Spanish economy on bank intermediation, the Spanish authorities will prepare, by mid-November 2012, proposals for the strengthening of non-bank financial intermediation including capital market funding and venture capital.

28. Governance arrangements of the financial safety net agencies will be reviewed to avoid potential conflicts of interest. In particular, the authorities will ensure that, as of 1 January 2013 there will be no active bankers anymore in the governing bodies of the FROB. The governance arrangements of the FGD will also be reviewed, in particular with regard to potential conflicts of interest.

VI. Public finances, macroeconomic imbalances and financial sector reform 29. There is a close relationship between macroeconomic imbalances, public finances and financial sector soundness. Hence, progress made with respect to the implementation of the commitments under the Excessive Deficit Procedure, and with regard to structural reforms, with a view to correcting any macroeconomic imbalances as identified within the framework of the European semester, will be regularly and closely monitored in parallel with the formal review process as envisioned in this MoU.

30. According to the revised EDP recommendation, Spain is committed to correct the present excessive deficit situation by 2014. In particular, Spain should ensure the attainment of intermediate headline deficit targets of [x]% of GDP for 2012, [x]% of GDP for 2013 and [x]% of GDP for 2014. Spanish authorities should present by end-July a multi-annual budgetary plan for 2013-14, which fully specifies the structural measures that are necessary to achieve the correction of the excessive deficit. Provisions of the Budgetary Stability Law regarding transparency and control of budget execution should be fully implemented. Spain is also requested to establish an independent fiscal institution to provide analysis, advice and monitor fiscal policy.

31. Regarding structural reforms, the Spanish authorities are committed to implement the country-specific recommendations in the context of the European Semester. These reforms aim at correcting macroeconomic imbalances, as identified in the in-depth review under the Macroeconomic Imbalance Procedure (MIP). In particular, these recommendations invite Spain to: 1) introduce a taxation system consistent with the fiscal consolidation efforts and more supportive to growth, 2) ensure less tax-induced bias towards indebtedness and home-ownership, 3) implement the labour market reforms, 4) take additional measures to increase the effectiveness of active labour market policies, 5) take additional measures to open up professional services, reduce delays in obtaining business licences, and eliminate barriers to doing business, 6) complete the electricity and gas interconnections with neighbouring countries, and address the electricity tariff deficit in a comprehensive way.

VII. Programme Modalities 32. Spain would require an EFSF loan, covering estimated capital requirements with an additional safety margin, estimated as summing up to EUR 100 billion in total. The programme duration is 18 months. FROB, acting as agent of the Spanish government, will channel the funds to the financial institutions concerned. Modalities of the programme will be determined in the FFA. The funds will be disbursed in several tranches ahead of the planned recapitalisation dates, pursuant to the roadmap included in Section IV. These disbursements can be made either in cash or in the form of standard EFSF notes.

VIII. Programme monitoring 33. The European commission, in liaison with the EcB and EBA, will verify at regular intervals that the policy conditions attached to the financial assistance are fulfilled, through missions and regular reporting by the Spanish authorities, on a quarterly basis. Monitoring of the FROB activities in the context of the programme will take place regularly. The Spanish authorities will request technical assistance from the IMF to support the implementation and monitoring of the financial assistance with regular reporting.

34. The authorities will provide to the European commission, the EcB, EBA and the IMF, under strict conditions of confidentiality, the data needed for monitoring of the banking sector as a whole and of banks of specific interest due to their systemic nature or their condition. A provisional list of required reports and data is provided in Annex 1.

35. State-aided banks and the Spanish authorities will report to the European commission on the implementation of their restructuring plan via the appointed monitoring trustee.

36. The European commission in liaison with the EcB and EBA will be granted the right to conduct on-site inspections in any beneficiary financial institutions in order to monitor compliance with the conditions.

37. In parallel, the Council should review on a regular basis the economic policies implemented by Spain under the Macroeconomic Imbalances procedure as well as under the Excessive Deficit Procedure.

Annex 1: Data requirements Spanish authorities will regularly submit or update, at least on a weekly or monthly basis the following data:

1. Reports and data, on a weekly basis, on bank deposits.

2. Reports and data, on a weekly basis, on banks' liquidity position and forecast.

3. Quarterly bank prudential financial statements as sent to the supervisor, for the 14 banking groups, including additional details on:

- financial and regulatory information (consolidated data) on the 14 banking groups and the banking sector in total, especially regarding (P&L), balance sheets, asset quality, regulatory capital, balance sheet forecasts;

- non-performing loans, repossessed assets and related provisions; to include exposure across different asset classes (Land & Development, including commercial real estate), Residential Real Estate, SME lending, Corporate lending, Consumer lending;

- asset quality across different asset classes (good quality, watch, substandard, NPL, restructured, of which restructured and NPL); provision stock across different asset classes, new lending across different asset classes;

- sovereign debt holdings;

- outstanding stock of debt issued, with a break down by seniority (senior secured, senior unsecured, subordinated of which preference shares, government guaranteed), with the amounts placed with retail customers, and amortization schedule;

- regulatory capital and its components: including capital requirements (credit risk, market risk, operational risk).4. Until quarterly balance sheet forecasts are available, an agreed template for banks supported by FROB, regarding refinancing needs and collateral buffers, for a horizon of 1 month, 3 months and 6 months should be provided. Funding plans will eventually be required for an expanded sample of banks. Reporting will be expanded to also include capital plans.

5. Reports and data on un-pledged eligible collateral.

6. Reports and data on borrowing amounts in the repo market, either directly or through CCPs.

The Spanish authorities will, at the latest one week after the start of the programme, propose formats and templates for the submission of this information, which will be agreed with the European Commission, the ECB, EBA and the IMF.

Above list is provisional. Further requests may be added at a later stage. For this purpose, a procedure will be set-up for the relevant staff of the European Commission, the ECB, EBA and the IMF to submit additional ad hoc bank data requests as needed.

Annex 2: Conditionality

Measure Date 1. Provide data needed for monitoring the entire banking sector and of banks of specific interest due to their systemic nature or condition (Annex 1). Regularly throughout the programme, starting end-July 2. Prepare restructuring or resolution plans with the EC for Group 1 banks, to be finalised in light of the Stress Tests results in time to allow their approval by the Commission in November. July 2012 - mid August 3. Finalise the proposal for enhancement and harmonisation of disclosure requirements for all credit institutions on key areas of the portfolios such as restructured and refinanced loans and sectoral concentration. End-July 2012 4. Provide information required for the Stress Test to the consultant, including the results of the asset quality review. Mid-August 2012 5. Introduce legislation to introduce the effectiveness of SLEs, including to allow for mandatory SLEs. End-August 2012 6. Upgrade of the bank resolution framework, i.e. strengthen the resolution powers of the FROB and DGF. End-August 2012 7. Prepare a comprehensive blueprint and legislative framework for the establishment and functioning of the AMC. End-August 2012 8. Complete bank-by-bank stress test (Stress Test). Second half of September 2012 9. Finalise a regulatory proposal on enhancing transparency of banks End September 2012 10. Banks with significant capital shortfalls will conduct SLEs. before capital injections in Oct./Dec. 2012 11. Banks to draw up recapitalisation plans to indicate how capital shortfalls will be filled. Early-October 2012 12. Present restructuring or resolution plans to the EC for Group 2 banks. October 2012 13. Identify possibilities to further enhance the areas in which the Banco de España can issue binding guidelines or interpretations without regulatory empowerment. End October 2012 14. Conduct an internal review of supervisory and decision-making processes. Propose changes in procedures in order to guarantee timely adoption of remedial actions for addressing problems detected at an early stage by on-site inspection teams. Ensure that macro-prudential supervision will properly feed into the micro supervision process and adequate policy responses.. End October 2012 15. Adopt legislation for the establishment and functioning of the AMC in order to make it fully operational by November 2012. Autumn 2012 16. Submit for consultation with stakeholders envisaged enhancements of the credit register. End-October 2012 17. Prepare proposals for the strengthening of non-bank financial intermediation including capital market funding and venture capital. Mid-November 2012 18. Propose measures to strengthen fit and proper rules for the governing bodies of savings banks and introduce incompatibility requirements regarding governing bodies of former savings banks and commercial banks controlled by them. End-November 2012 19. Provide a roadmap (including justified exceptions) for the eventual listing of banks included in the stress test which have benefited from state aid as part of the restructuring process. End-November 2012 20. Prepare legislation clarifying the role of savings banks in their capacity as shareholders of credit institutions with a view to eventually reducing their stakes to non-controlling levels. Propose measures to strengthen fit and proper rules for the governing bodies of savings banks and introduce incompatibility requirements regarding the governing bodies of the former savings banks and the commercial banks controlled by them. Provide a roadmap for the eventual listing of banks included in the Stress Test, which have benefited from State aid as part of the restructuring process.. End-November 2012 21. Banks to provide standardised quarterly balance sheet forecasts funding plans for credit institutions receiving state aid or for which capital shortfalls will be revealed in the bottom-up stress test. As of 1 December 2012 22. Submit a policy document on the amendment of the provisioning framework if and once Royal Decree Laws 2/2012 and 18/2012 cease to apply. Mid-December 2012 23. Issues CoCos under the recapitalisation scheme for Group 3 banks planning a significant (more than 2% of RWA) equity raise. End-December 2012 24. Transfer the sanctioning and licensing powers of the Ministry of Economy to the Banco de España. End-December 2012 25. Require credit institutions to review, and if necessary, prepare and implement strategies for dealing with asset impairments. End-December 2012 26. Require all Spanish credit institutions to meet a Common Equity Tier 1 ratio of at least 9% until at least end-2014. Require all Spanish credit institutions to apply the definition of capital established in the Capital Requirements Regulation (CRR), observing the gradual phase-in period foreseen in the future CRR, to calculate their minimum capital requirements established in the EU legislation. 1 January 2013 27. Review governance arrangements of the FROB and ensure that active bankers will not be members of the Governing Bodies of FROB. 1 January 2013 28. Review the issues of credit concentration and related party transactions. Mid-January 2013 29. Propose specific legislation to limit the sale by banks of subordinate debt instruments to non-qualified retail clients and to substantially improve the process for the sale of any instruments not covered by the deposit guarantee fund to retail clients. End-February 2013 30 Amend legislation for the enhancement of the credit register. End-March 2013 31. Raise the required capital for banks planning a more limited (less than 2% of RWA) increase in equity. End-June 2013 32 Group 3 banks with CoCos to present restructuring plans. End-June 2013